The saying goes, “if the only tool you have is a hammer, everything looks like a nail.” That is the difficulty Fed chair Janet Yellen sees in monetary policy: if the only tool is raising or lowering interest rates, then everything – bubbles, inflation, unemployment, excessive risks, yield hunting or systemically important financial institutions – looks like nails. In a lecture at the IMF earlier this week (here), Mrs. Yellen answered questions about future bubbles and rate increases by explaining that the Fed has much more than the hammer of interest rates.

Macroprudential policy may not get through most spell checkers, but it is the chosen approach to frothy financial markets and incipient bubbles. Macroprudential policies are not new, but most were not aggressively used in the run-up to the financial crisis. Examples include regulatory limits on leverage, restrictions on short term funding and stronger underwriting standards for loans and mortgages. When the challenges in the financial markets are rapidly rising home prices or excessive and misunderstood risks, the response should be tighter credit standards for mortgages or restrictions on leverage. If the Fed were to raise interest rates to burst a housing bubble, the bubble might persist while higher interest rates boosted unemployment or lowered economic growth. Restrictions on loan-to-value and income-to-loan ratios would be a better choice. Interest rate policy should be reserved for controlling inflation and unemployment.

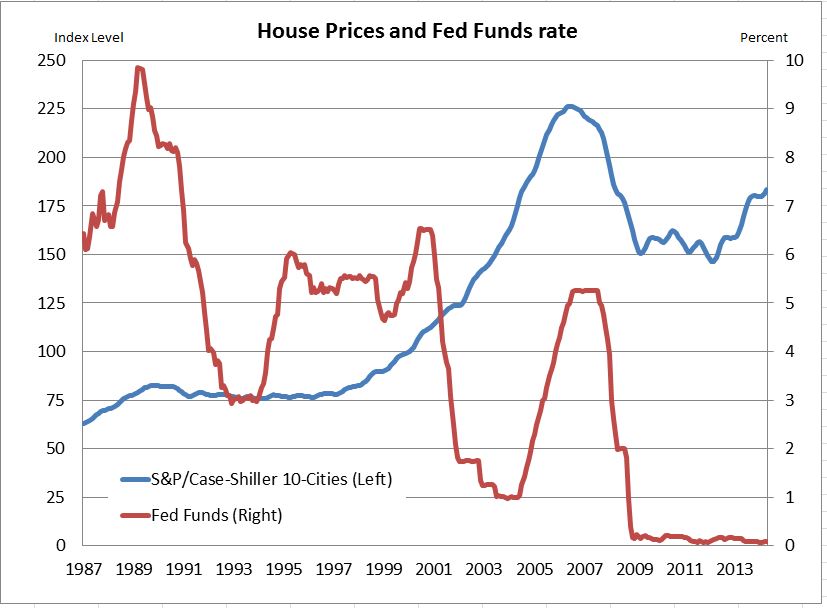

The chart shows the monthly pattern of home prices (as measured by the S&P/Case-Shiller 10 City Composite Index) and the fed funds rate since 1987. While whether the fed funds rate aggravated the housing bubble is debatable, there is a need for better ways to address bubbles,

The combined use of interest rate and macroprudential policies has some implications for investors: First, worries about a renewed housing bubble are not likely to push the Fed to raise interest rates. Those who want to argue that the rate increase will come sooner than the consensus target of the summer of 2015 need to argue about inflation and unemployment. Second, macroprudential policies are likely to reduce risks and profits in the financial sector. Less leverage should reduce the risk of another Lehman Brothers scale bank failure; it will also lower bank profits.

Some may wonder why macroprudential policy rules are needed – shouldn’t market discipline keep leverage in line and maintain credit standards? Hyman Minsky, a sometimes forgotten economist, noted that when good times persist people forget the risks and ignore the rules until the bubbles grow, leverage expands and banks and businesses fail. Macroprudential policy is partially an effort to control human nature.

The posts on this blog are opinions, not advice. Please read our Disclaimers.