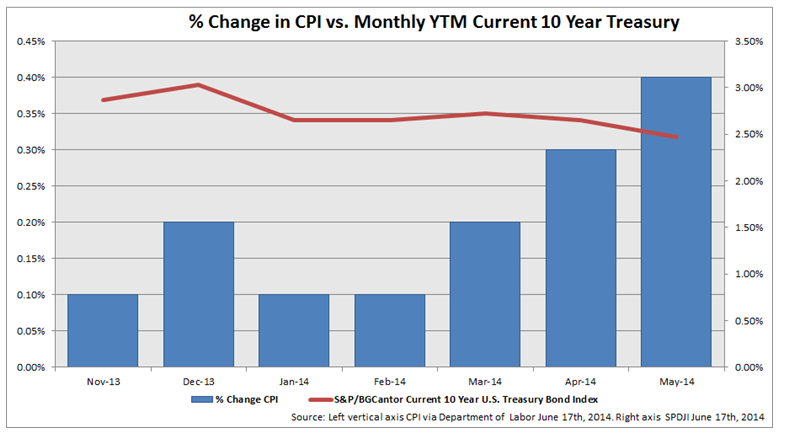

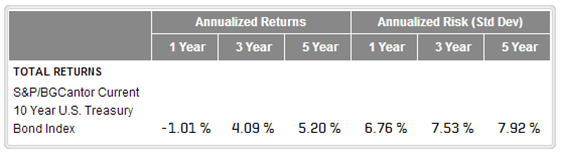

The market waits in anticipation this week as key economic indicators will be released to shed light on the health and direction of the financial world. The Department of Labor released Consumer Price Index (CPI) data for May showing consumer inflation ticking up 2.1% over the past twelve months. The Federal Reserve has stated an inflation objective of 2.0% prior to raising rates. The S&P/BGCantor Current 10 Year U.S. Treasury yields have remained relatively flat, 2.66 YTM with a YTD return of 4.94%. Bond prices and yields have an inverse relationship.

(Source: S&P Dow Jones Indices)

European Banks Back in Vogue

Conversely, across the pond, inflation has dropped to 0.6% in May, a 0.2% decrease from the EU’s April 0.8% inflation stat (Source: Eurostat). With the EU reaching some of its lowest inflation since 2009, the European Central Bank cut rates in early June in an attempt to fuel growth.

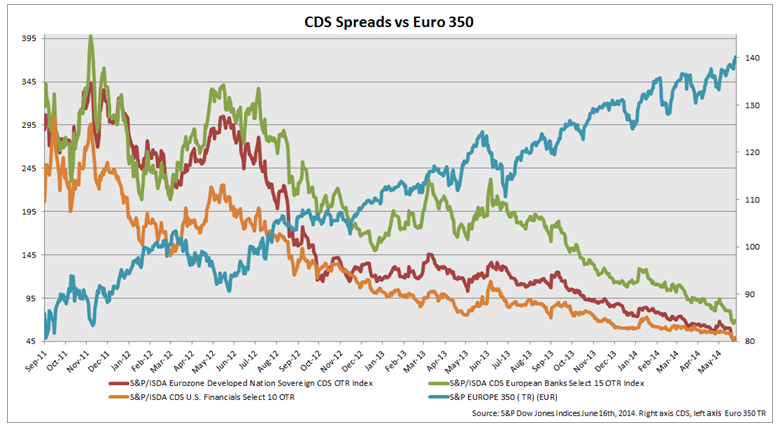

In a lower rate environment, credit default insurance for the European financial sector is becoming cheaper. Observed by the S&P/ISDA CDS European Banks Select 15, the notional amount has fallen 116 bps since this time last year to 73 bps. Essentially, where the market required $2,323 to insure an underlying credit of $100,000 in this sector in June 2013, now only requires $726 or 69% less. The reduction in cost of CDS insurance could be due to the three-year rally of the S&P Europe 350 which has a 1-year return of 18.49%. This trend could also be systemic of investors willing to take on more risk in search of yields in the low rate environment.

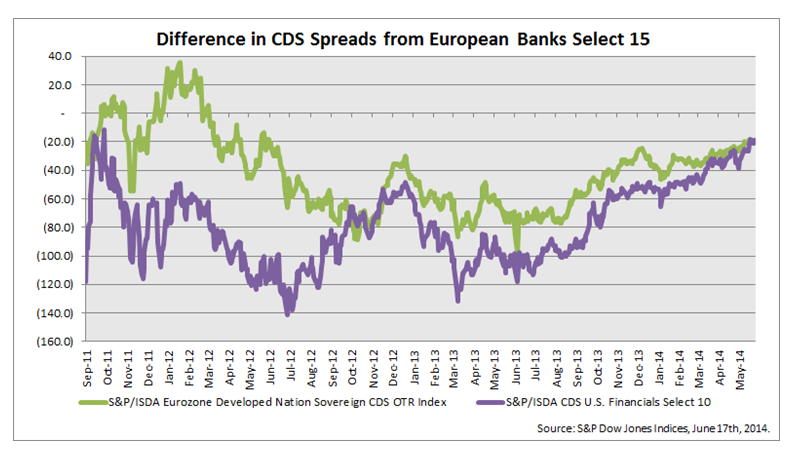

By examining the difference in spreads relative to the CDS European Banks to Eurozone sovereign bonds and financials in the U.S., we see that insurance across these sectors has not been this comparable in price for years. Default spreads between the S&P/ISDA CDS U.S. Financials Select 10 and European banks have not been this close since October 2011. Similarly, one would have to look back to June of 2012 to find European bank default insurance priced as comparably to S&P/ISDA Eurozone Developed Nation Sovereign CDS OTR Index. The difference today, however, is the dramatically lower cost against the notional debt of European bank credit default swaps.

While the U.S. is finally hitting inflation targets and the E.U. is missing their own by over half, little has changed. U.S. 10-year treasuries are still below 3% and the pricing of the default risk between the two indicates a similar outlook. With the Fed cutting QE, reducing growth projections, and holding off to significantly raising rates until 2015; the outlook is uncertain. For now, we will just have to wait and see how the tale of raising rates and inflation will play out.

The posts on this blog are opinions, not advice. Please read our Disclaimers.