This post looks at why index earnings are derived by summing earnings of index constituents without first weighting the earnings by index weight (cap-weight or otherwise). While earnings are probably the most widely followed fundamental item, this explanation is applicable to a data point of one’s choice – operating earnings, cash flow, etc. An easy way to understand this kind of fundamental index data is to think of an index, such as the S&P 500, as a hypothetical portfolio.

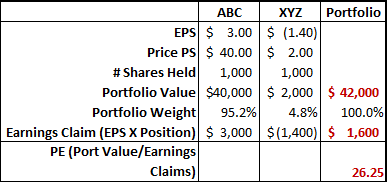

Consider a theoretical example in which we hold 1,000 shares in each of two stocks, ABC and XYZ. ABC is quite profitable, while XYZ is operating at a loss.

Despite the fact that 95% of the portfolio is invested in a stock with a PE of 13.3 ($40/$3), the portfolio as a whole has a claim to $1,600 in total earnings. We can’t ignore the losses generated by XYZ simply because we wish to – we hold 1,000 shares and each one is losing $1.40.

Dividing portfolio value by portfolio earnings claims gives a ratio of 26.25 – the price to earnings ratio (PE) of the portfolio. PE, calculated on this basis, has the useful property of indicating how long it takes to “earn” back our investment under current conditions – in this case, 26 ¼ years.

Conversely, if we were to weigh earnings claims by portfolio weights we would get the following:

![]()

It’s clear to see that one could easily be lead astray by the $2,790 earnings figure, which is the sum of weighted earnings claims. The most significant observation is that the portfolio does not, in fact, hold claim on $2,790 in earnings. This figure exaggerates our legitimate claim of $1,600 by $1,190! Obviously, if one were to calculate a PE ratio on this basis, it would be unrealistically low. Our two-stock example shows that a cumulative dollar, whether earned or lost, is equivalent in the aggregate of a portfolio whether it is derived from a large holding or a small one.

Similarly, index earnings represent the aggregate earnings of all companies in the index, and on this basis the index PE provides valuable information. A high index PE may imply a small, or nonexistent, margin of safety – the central investment concept articulated by Ben Graham, who described it as “the secret of sound investment…” and “always dependent on the price paid…”[1]

For more on the ins and outs of index earnings, see David Blitzer’s post from earlier in the year.

[1] Benjamin Graham, The Intelligent Investor, Revised Ed, pages 512, 517. (New York: HarperCollins, 2003)

The posts on this blog are opinions, not advice. Please read our Disclaimers.