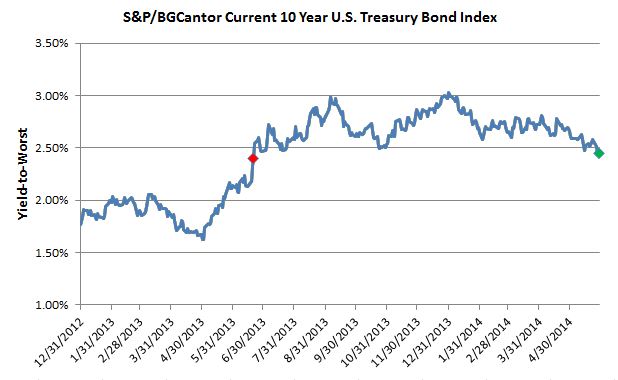

The last time the yield of the S&P/BGCantor Current 10 Year U.S. Treasury Bond Index was in the neighborhood of 2.4% was back in June 2013. The days of a 1% handle on rates are behind us, but the current lower rates harken back before this year. The beginning of 2014 saw yields as high as 3%. Back then, the market worried over issues such as the start and speed of Fed tapering, discussions of the timing of a rate increase, and an improving jobless claims number. Jobless claims were at 7% and the Fed was targeting 6.5%. Yields did come lower as a crisis in Ukraine erupted and a flight to safety trade resulted. Though it first appeared to pit the superpowers of Russia and the U.S. against each other, the Ukraine crisis has been downgraded to somewhat of a skirmish as varying counties has taken diplomatic approaches to dealing with the crisis.

Some focus has always been on the speed and timing of an economic recovery. Economic releases had been slow to indicate the speed of the recovery though recent numbers have shown a growing strength in their measures. The improving economic picture was knocked for a loop when a surprise rise in Germany’s unemployment to 24,000 from the expected 15,000 became cause for concern. Such a number before the June 5 European Central Bank interest rate announcement led investors to question economic strength and the possibility of an additional rate cut in Europe.

Since then, global sovereign bonds have moved down in yield. The S&P/BGCantor Current 10 Year U.S. Treasury Bond Index closed 7 basis points lower on the day of the Germany release (May 28). The change in pace of the expected global recovery has caused traders to cover shorts put on in expectation of higher rates, thus moving price higher and yields lower. Also, benchmark investors’ have been purchasing bonds to match their index’s duration extension for the May month-end rebalancing. Though reduced from prior levels, the Fed still purchases treasury bonds and mortgage bonds as part of the ongoing stimulus.

The posts on this blog are opinions, not advice. Please read our Disclaimers.