The fixed income market is quintessential for the growth of the economy. They serve as one of the mediums for the government to raise money. In India the fixed income market has been attaining the depth as well as maturity over the years and the government securities play a dominating role.

The on-the-run 10 year fixed interest rate bond issued by the Reserve Bank of India is treated as the benchmark and serves as a reference point for pricing of the other bonds along a yield curve. The S&P BSE India 10 Year Sovereign Bond Index seeks to measure the performance of the benchmark security and can be considered as the bellwether index.

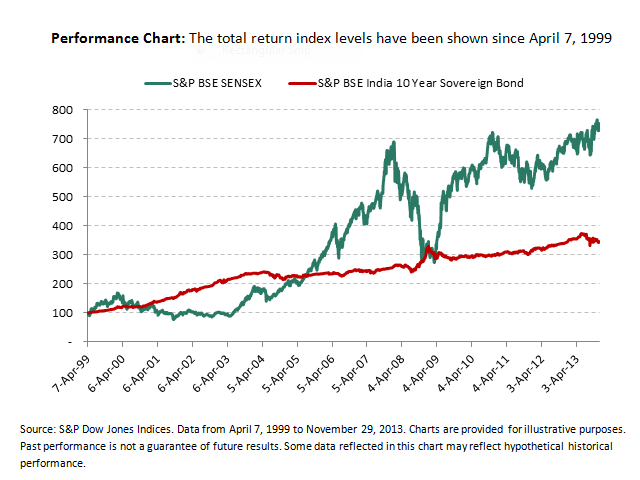

Fixed income market returns in general tend to be less volatile as compared to the equity market returns. This is very well depicted in the performance chart below. We can observe that S&P BSE India 10 Year Sovereign Bond index is less volatile as compared to S&P BSE SENSEX index.

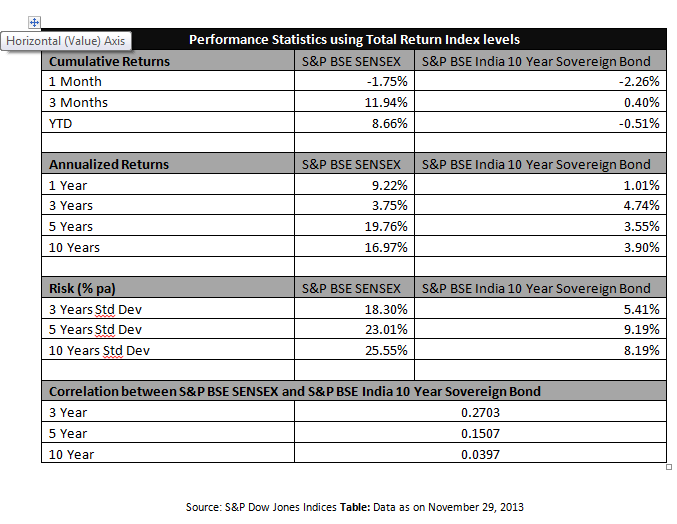

Average inflation in India was low during 2003 to 2007 and S&P BSE SENSEX index did well in these years. The S&P BSE India 10 Year Sovereign Bond Index remained mostly stable. In the year 2008, which was marked by recession, the S&P BSE SENSEX index nosedived, whilst the S&P BSE India 10 Year Sovereign Bond Index rose. Since 2009, the S&P BSE SENSEX index has improved significantly and the S&P BSE India 10 Year Sovereign Bond Index has also shown stable growth. The risk percentage and the annualized returns of the S&P BSE India 10 Year Sovereign Bond Index are low vis-à-vis S&P BSE SENSEX Index. The correlation of monthly returns in both the asset classes is very less and it decreases further as the time span increases. Table below summarizes the statistics.