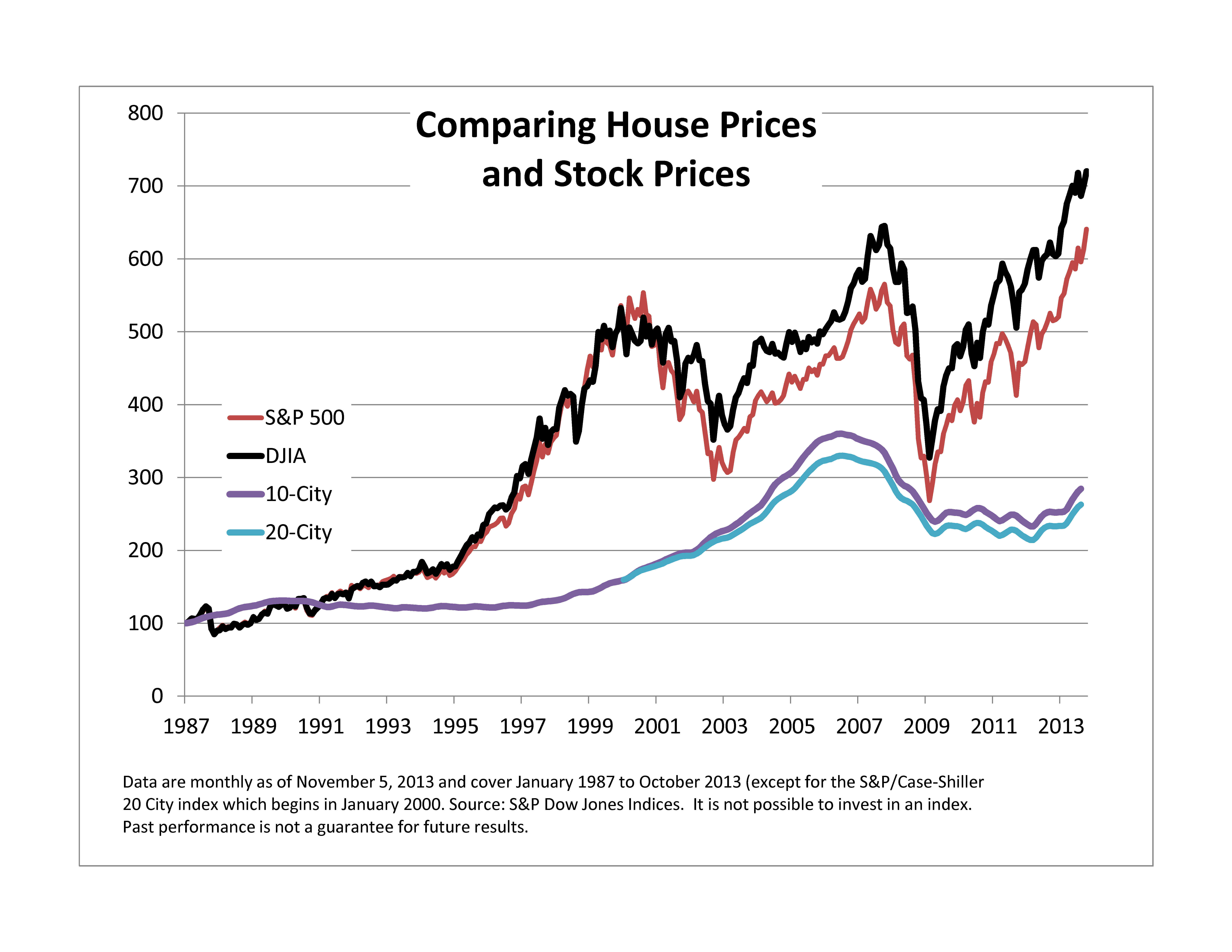

When tech stocks collapsed in 2000 and the market fell 50%, investors put their faith in houses: maybe too much faith. Then house prices collapsed from mid-2006 as mortgage excesses took down the economy. Stocks fell 50% again. The subsequent recovery in the economy, houses and stocks disappointed at least two of the three: the economy is lackluster and housing is coming back but remains about 20% below the peaks set seven years ago. Stocks have done better, reaching new highs as the S&P 500 recovered some 140% from the bottom. But even stocks are a scant 12% to 13% above their 2007 highs in six years or an annual return of two percent. Are houses a better bet because they suffered only one collapse since the turn of the century or are stocks preferred because the rebound is more dramatic? And what happened to diversification by spreading one’s wealth across houses and stocks?

The chart gives a quick comparison, but some numbers might help. All the data on the chart are monthly which means that some of the peaks and troughs of the market may be obscured compared to daily data. The housing series are monthly. As the picture suggests, stocks are more volatile. Both the S&P 500 and the Dow have standard deviations of monthly returns of about 15% annualized. The figures for the house price series (the S&P/Case-Shiller 10-City and 20-City Composites) are 3.3% and 4.0%. Stock investors would probably worry more often since stock prices will move farther and faster than house prices. Another aspect of the risk comparison is the depth of the collapse or draw down. Stocks dropped about 50% in both the tech bust and the housing bust; houses fell a comparatively modest 35%. The surprise in the numbers may be diversification and correlation. While the financial crisis sent everything but treasury bills into a free fall, the correlation between the S&P 500 and the S&P/Case-Shiller 10-City Composite is about 3.5%. Indeed another look at the chart shows that peaks and troughs of houses and stocks do not line up. The numbers don’t, and can’t, answer the question of which is the better choice between houses and stocks; it depends on the investor, his or her situation and taste for houses, stocks or risk.