In November 2017, S&P Dow Jones Indices and MSCI announced revisions to the GICS® structure to be implemented in September 2018.[1] These changes are going to affect the consumer discretionary, information technology, and telecommunication services sectors. As a consequence, the Pan Asian internet giants BAT (Baidu, Alibaba, and Tencent) will be reclassified into the communication services and consumer discretionary sectors.

The key GICS structure changes are summarized as follows.

- The telecommunication services sector will be broadened and renamed to communication services. The renamed sector will include the existing telecommunications services companies with the addition of media and entertainment companies, which are currently classified under the consumer discretionary sector and information technology sector.

- The internet & direct marketing retail sub-industry under the consumer discretionary sector will include companies providing online marketplaces for consumer products and services. It will also include e-commerce companies.

- The internet software & services industry under the information technology sector will be discontinued and moved to a new sub-industry, internet services & infrastructure, under the IT services industry.

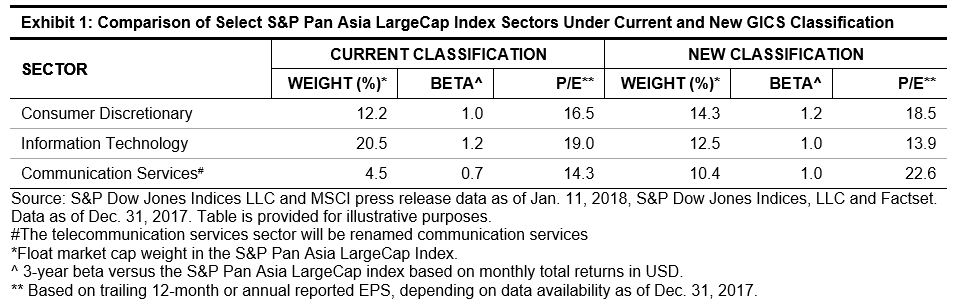

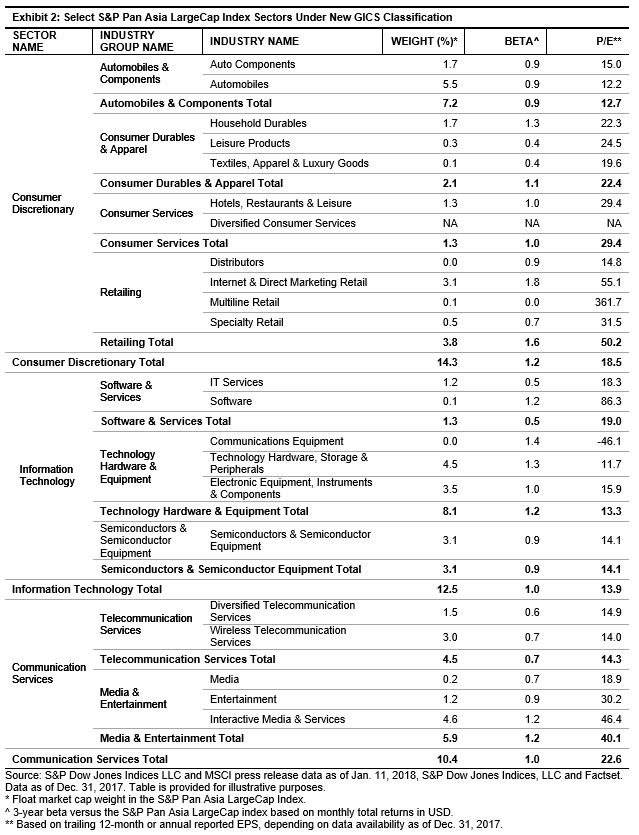

These changes could result in a significant impact on the composition, valuation, and performance characteristics of the sector indices. Based on the select list of large-cap companies with new GICS information released in January 2018,[2] we compiled the sector weights, return beta, and P/E of the three GICS sectors for the S&P Pan Asia LargeCap Index with the new GICS definitions (see Exhibits 1 and 2). The key observations include the following.

- The communication services sector will become less defensive and have more expensive P/E versus the current telecommunication services sector, mainly due to the addition of entertainment companies (such as Nintendo) and interactive media & services companies (such as Tencent). The regional sector weight increases from 4.5% to 10.4%.

- After the change in definition of the internet & direct marketing retail industry, the consumer discretionary sector will have higher beta and valuation, with the inclusion of Alibaba, which is currently classified as an internet software & services company. The regional weight of this sector changes from 12.2% to 14.3%.

- The information technology sector will have lower beta and P/E in comparison to the current GICS definition, primarily driven by the exclusion of the internet giants BAT, which represent 31.5% of the regional sector under the current classification.

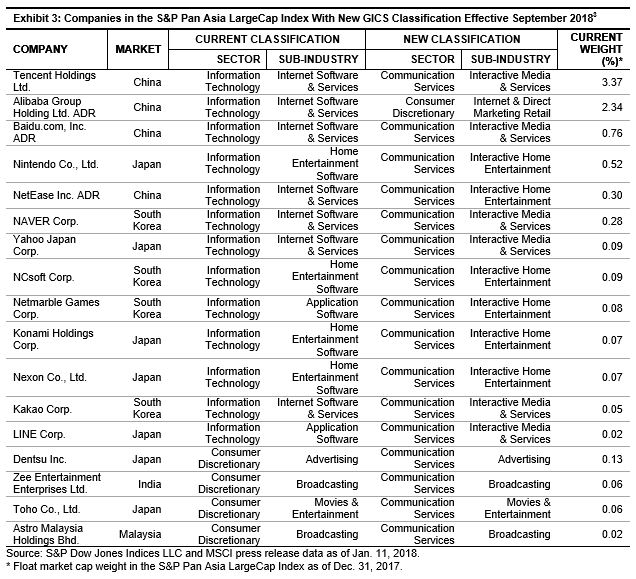

Overall, 17 companies from the S&P Pan Asia LargeCap Index will be affected by the revision to the GICS structure, according to the list announced by S&P Dow Jones Indices and MSCI in January (see Exhibit 3).

Apparently, the revisions to the GICS structure will result in significant change to the risk/return profile and fundamental characteristics of the consumer discretionary, information technology, and communication services sectors. Market participants should be mindful about these changes when evaluating these sectors in their asset allocation or investment analysis.

[1] For more details, please see https://spindices.com/documents/index-policies/20171115-gics-2018-revisions.pdf

[2] For more details, please see https://www.spice-indices.com/idpfiles/spice-assets/resources/public/documents/646149_gicspressreleasejan2018.pdf

[3] Note that the new company classifications are subject to change before implementation due to ongoing reviews, including for corporate events. For more details please see https://spindices.com/documents/index-policies/gics-changes-announcement-01-10-18.xlsx.

The posts on this blog are opinions, not advice. Please read our Disclaimers.