In one of my previous blog posts, we demonstrated that high yield bonds exhibited a strong negative correlation with VIX and an even stronger one with VIX futures, which comes mostly from down markets. This prompted us to think that VIX futures may hold tail-risk hedging opportunities for high yield bond portfolios. In this blog, we explore allocating VIX futures to tail hedge a high yield bond portfolio, with back-tested results for the following two hedging strategies.

- Static allocation: Allocating a static weight of x% to VIX futures in a bond portfolio.

- Dynamic allocation: Allocating a fixed percentage (x%) of the portfolio to VIX futures according to the observed VIX spot level. At each month’s end, if the VIX spot is equal to or greater than 25, x% of the portfolio is allocated to VIX futures the next month. If the VIX spot at month’s end is less than 25, the allocation to VIX futures is 0.

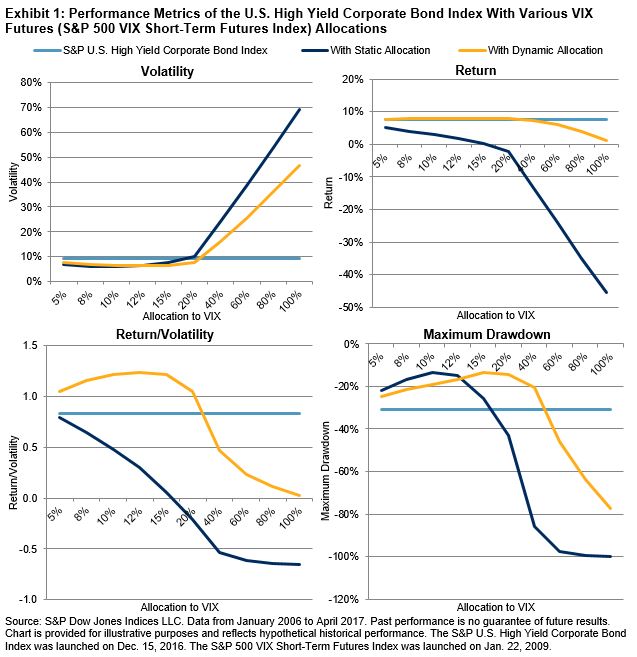

Exhibit 1 shows risk, return, and drawdown figures for a high yield bond portfolio with allocation to VIX futures ranging from 0 to 100%. On volatility alone, both static and dynamic allocation of VIX futures can help reduce portfolio volatility, as long as the VIX futures allocation is kept under 20%. Allocating more than 20% to VIX futures proved to overhedge the bond portfolio and introduce VIX as a new risk factor that can raise portfolio volatility as allocation increases.

On the return side, dynamic allocation to VIX futures can also improves portfolio returns when the allocation is kept under 20%. In comparison, static allocation to VIX futures can significantly drag down portfolio return, as rolling VIX futures tends to incur costs. Risk-adjusted return, as measured by the ratio of return over volatility, is optimized when VIX futures are dynamically allocated at 12%.

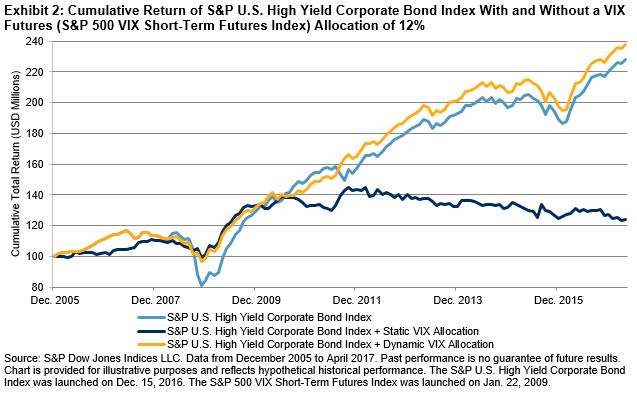

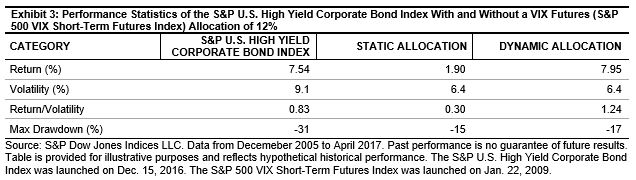

Exhibits 2 and 3 show the cumulative returns and performance statistics of a high yield bond portfolio with and without a VIX futures allocation of 12%. Dynamic allocation to VIX futures can provide downside protection and lessen portfolio drawdown—for example, during the market turmoil of 2008, 2009, and 2011—while adding extra return to the bond portfolio. Return per unit of risk improved from 0.83 to 1.24 for the dynamic allocation strategy.

Though static allocation of VIX futures can reduce portfolio volatility and offer downside protection compared with the broad-based, unhedged S&P U.S. High Yield Corporate Bond Index, it can drag down portfolio performance significantly, due to the high cost of rolling VIX futures.

Our back-tests have confirmed the potential benefit of a dynamic allocation to VIX futures in a high yield bond portfolio. Furthermore, we found that the risk-adjusted returns of the portfolio, as measured by the ratio of return over volatility, were optimized at the VIX futures allocation of 12% with our allocation algorithm.

The posts on this blog are opinions, not advice. Please read our Disclaimers.