Since the negative interest rate policy was announced by the Bank of Japan, the yield of the S&P Japan Sovereign Bond Index has tightened 33 bps to -0.07%, as of Aug. 23, 2016. As the quantitative and qualitative easing program continues, some Japanese market participants seek investments that diversify their portfolios. U.S. treasury bonds have become appealing, as they offer better yields and high creditworthiness.

Fixed income investments can play an important role in a well-diversified portfolio, as they tend to reduce the overall portfolio volatility and generate income. Historically, U.S. bonds and U.S. equities have performed differently; they have negative correlations over the five-year period ending Aug. 23, 2016.[1]

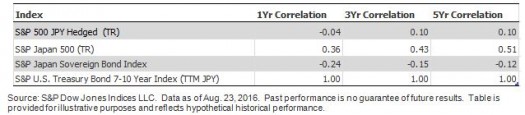

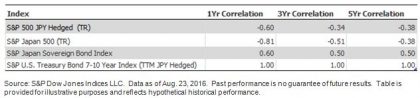

The benefit of diversification still holds when looking into Japanese yen assets. In the correlation analysis in Exhibits 1 and 2, the Japanese equities market is represented by the S&P Japan 500 (TR), the U.S. equities market is represented by the S&P 500 JPY Hedged (TR), and the Japanese sovereign bond market is represented by the S&P Japan Sovereign Bond Index. These assets are separately compared against the S&P U.S. Treasury Bond 7-10 Year Index (TTM JPY), which is calculated in Japanese yen, and the S&P U.S. Treasury Bond 7-10 Year Index (TTM JPY Hedged), which tracks the same bonds with returns represented in Japanese yen but is hedged in an effort to eliminate currency exposure through a one-month forward currency contract.

Regardless of market participants’ option to hedge the currency or not, historical data shows that U.S. Treasury bonds have had low to negative correlations with other major asset classes offered in Japan. Hence, there is a potential diversification benefit.

Exhibit 1: Correlation With the S&P U.S. Treasury Bond 7-10 Year Index (TTM JPY)

Exhibit 2: Correlation With the S&P U.S. Treasury Bond 7-10 Year Index (TTM JPY Hedged)

[1] Based on return performance of the S&P 500® (TR) and the S&P U.S. Treasury Bond 7-10 Year Index; data as of Aug. 23, 2016.

The posts on this blog are opinions, not advice. Please read our Disclaimers.