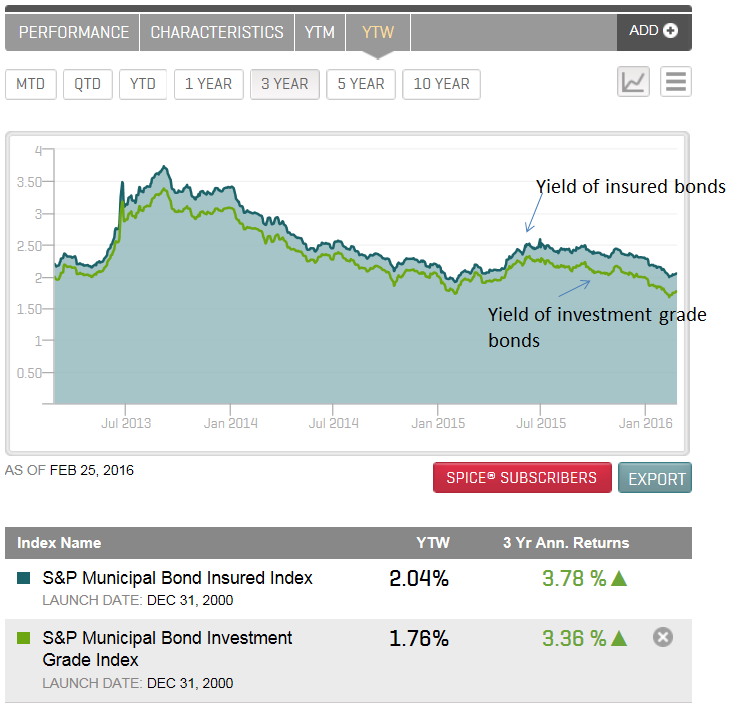

Okay, the mono-line insurance companies aren’t going to enjoy this note. After all, yields of insured bonds should be lower than bonds that are un-insured. Prior to the great recession approximately half of the municipal bonds outstanding were insured and during that time insured bonds were more in demand than un-insured bonds. Beginning with the great recession we have seen yields of insured bonds higher than un-insured bonds as questions about the viability of the insurers themselves were prominent worries in the market place. It is understood that not all mono-line insurers are the same credit quality, some are stronger than others. However, in aggregate the impact is impressive.

Using the weighted average yields of bonds in the S&P Municipal Bond Insured Index and the S&P Municipal Bond Investment Grade Index the difference can be highlighted. The result has been yield ‘pickup’ between insured and investment grade municipal bonds as of Feb. 25 2016 was 28bps. In general, it is cheaper to buy insured bonds than un-insured bonds and as a result returns have been higher.

Chart 1: Select municipal bond indices and their yields and returns over three year period

The risk of generalizing or over simplifying the complex municipal bond market is inherent in any broad analysis. Each issuer and each mono-line insurer has their own credit profile. The indices aggregate the bonds to provide the weighted average statistics used.

The posts on this blog are opinions, not advice. Please read our Disclaimers.