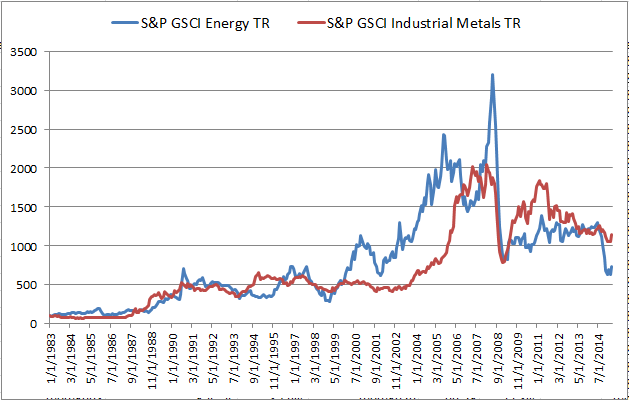

In April, the S&P GSCI gained 11.1%, posting its 19th best month in history with data back to January, 1970. The last time the index had performance this strong was in May, 2009 but what is most interesting is that all commodities in energy and industrial metals were positive.

When the economy slows, people still consume agriculture and livestock, and many use the precious metals as a safe haven. However, demand for energy and industrial metals are more sensitive to the growth of the economy but still may perform differently based on the type of growth – for example, automobile demand may increase energy consumption while construction may drive industrial metals.

Using historical monthly returns back to February 1983, energy and industrial metals only have a correlation of 0.20 and only move up together less than 1/3 of the time. Below is the chart of cumulative returns where you can see there is some relationship, though far from perfect.

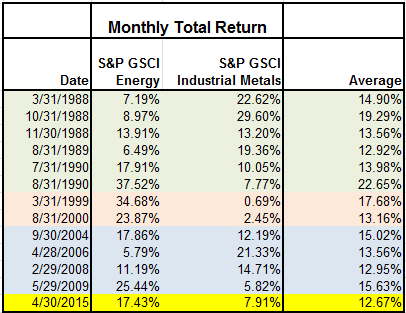

Given this less than perfect positive correlation but notion of economic sensitivity, when the two sectors spike together, it may be indicative. Since 1983, in only 12 months have energy and metals moved together on average in a month as much as in April 2015. The last time the sectors increased on average in a month as much as they did last month was in May 2009. The table below shows the months in history where the simple average of the two sectors was greater than in April 2015:

While the combined positive returns of at least today’s magnitude haven’t necessarily occurred in consecutive months, there are distinct general periods when the energy and industrial metals spiked, and with the exception of the 1999-2000 time that was clearly driven by energy, both sectors had relatively strong returns.

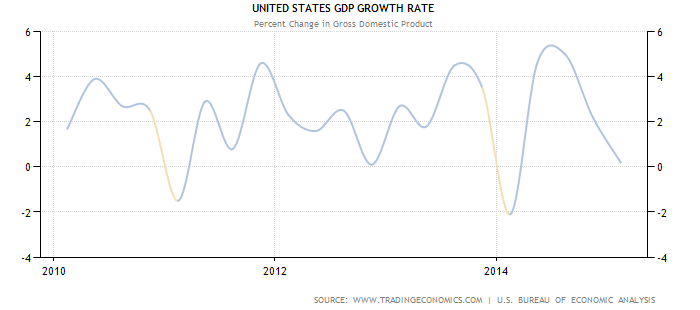

Given only four blocks of time where energy and industrial metals have moved this much, it seemed a comparison to real GDP growth might be interesting. Below is a chart of yoy% change of GDP data by per capita terms of the Americas. Notice the dips that follow each block of energy and industrial metal performance.

![Source:http://www.worldeconomics.com/papers/Global%20Growth%20Monitor_7c66ffca-ff86-4e4c-979d-7c5d7a22ef21.paper Real GDP data was taken from the World Economics Global GDP database Population data was obtained from the Maddison and the United Nations tables 2012/14 data was calculated from the year on year estimated % increase in real GDP from the IMF tables[1] (Gross domestic product, constant prices, % change)](https://www.indexologyblog.com/wp-content/uploads/2015/05/GDPyoyAmericas.png)

The posts on this blog are opinions, not advice. Please read our Disclaimers.