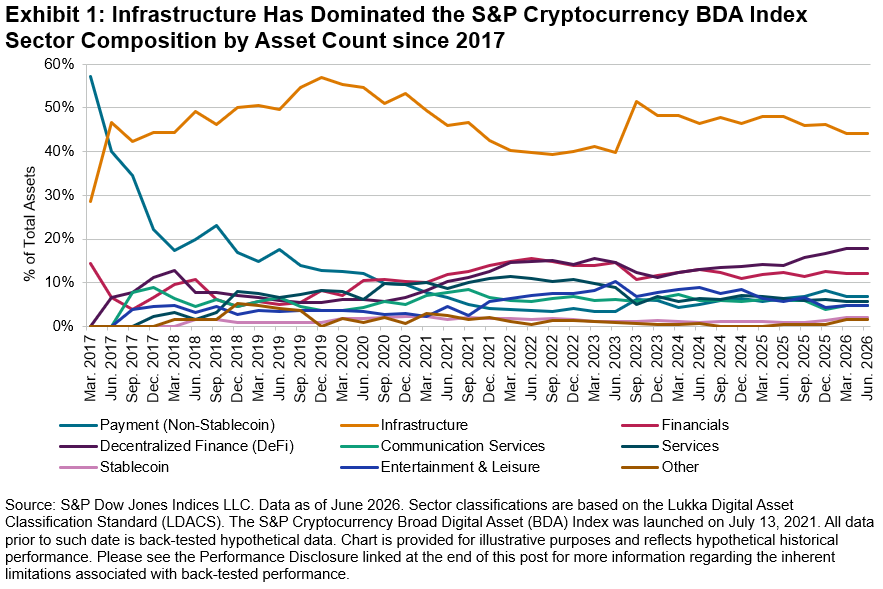

A common assumption about the digital asset market is that it remains a monolithic asset class dominated by a small number of names. However, examining the sector composition of the S&P Cryptocurrency Broad Digital Asset (BDA) Index reveals a more nuanced picture, one where diversity by asset count does not necessarily translate into diversity by market capitalization weight, and where sector-level diversification may coexist with network-level concentration.

The Lukka Digital Asset Classification Standard (LDACS)1 assigns each index constituent to a macro sector based on its most prevalent intended use and structure. By asset count, the Infrastructure sector—which includes Layer 1 and Layer 2 blockchains, oracle networks and decentralized storage protocols—has represented the largest share of the index since 2017, reaching approximately 44% of constituents by mid-year 2026. Decentralized Finance (DeFi) has emerged as a notable category, rising from near zero to approximately 18% over the same period. Financials, Communication Services and other sectors contribute additional breadth.

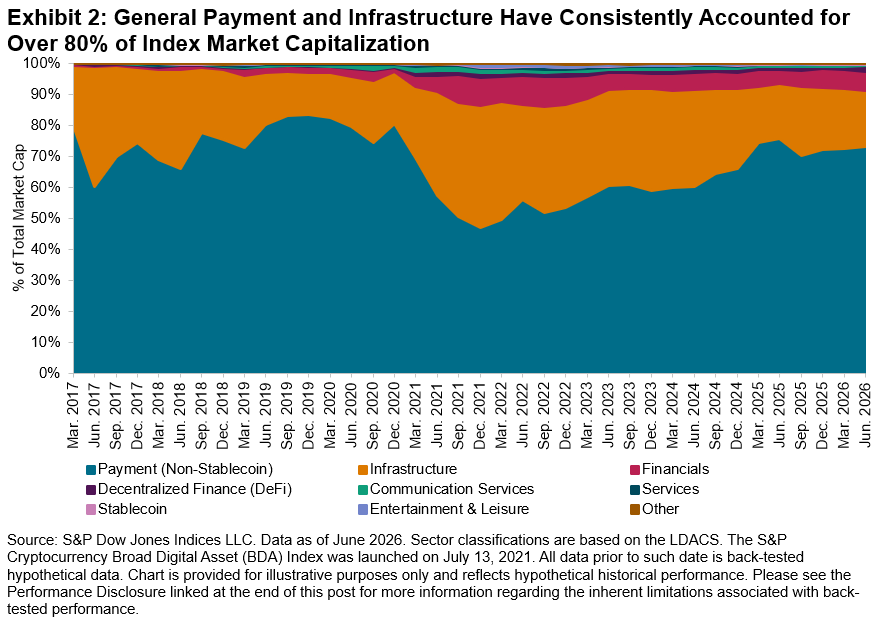

While diversity by asset count has increased over time, market capitalization remains concentrated. The Payment (Non-Stablecoin) sector—which includes Bitcoin—has consistently represented between 50% and 80% of total index market capitalization. Infrastructure constitutes the second-largest share at 15%-40%. Together, these two sectors have accounted for over 80% of index weight throughout most of the observed period. Sectors such as DeFi and Financials, despite growing representation by count, remain minor contributors by weight and represent a widely referenced segment of the digital asset ecosystem. This divergence between market cap and market interest highlights the distinction between base-layer networks and application-layer protocols. While Infrastructure and Payment tokens cover the bulk of current market capitalization, DeFi and Financials represent the functional use cases built on top of those networks, driving demand for targeted benchmarks to track these specific innovations.

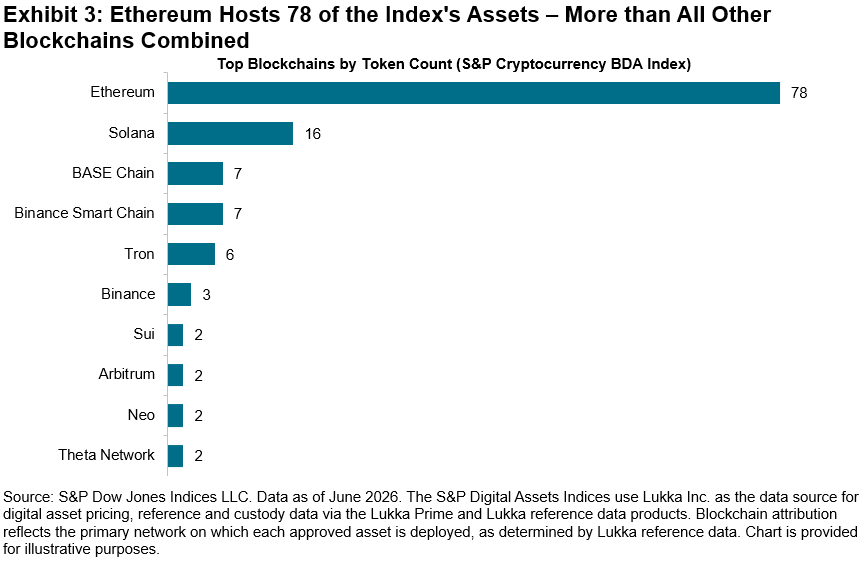

The index’s sector-level diversification coexists with a structural concentration at the network layer. Of the index’s constituents, 78 reside on the Ethereum blockchain, compared to 16 on Solana and single digits across BASE Chain, Binance Smart Chain, Tron and others. While the index reflects distinct functional use cases across multiple sectors, the majority of the constituents share a common settlement and execution layer. Sector diversification, in this context, may not fully equate to infrastructure diversification.

The S&P Cryptocurrency BDA Index reflects meaningful sector diversification by asset count. However, two forms of concentration are observable: market capitalization remains dominated by Payment and Infrastructure, and most constituent tokens are hosted on a single blockchain network. These patterns are not unique to digital assets—traditional equity indices also exhibit broad constituent coverage alongside narrow weight concentration—but they highlight the value of distinguishing between thematic diversity and structural independence when evaluating index composition.

1 The Lukka Digital Asset Classification Standard (LDACS) is a five-tier hierarchical taxonomy designed to classify digital assets based on their most prevalent intended use and structure. LDACS is governed by the Lukka Reference Data Oversight Board and reviewed quarterly.

The posts on this blog are opinions, not advice. Please read our Disclaimers.