As Brazil’s capital markets continue to mature, market participants now have access to a new tool for measuring and tracking volatility: the S&P/B3 VIX® Futures Index. Launched on May 25, 2026, this index represents a significant addition to the S&P/B3 Futures Indices and a meaningful step forward for the theme of volatility in Brazil.

What Is the S&P/B3 VIX Futures Index?

In December 2025, B3 launched VIX futures contracts on the S&P/B3 Ibovespa VIX—an implied volatility index that measures the market’s 30-day expectations for the volatility of the Ibovespa, Brazil’s headline equity benchmark. These contracts give market participants a direct and tradeable way to express a view on Brazilian equity volatility and to hedge equity market downturns.

The S&P/B3 VIX Futures Index is built based on these contracts and measures the performance of maintaining a constant 30-day long position in S&P/B3 Ibovespa VIX Futures. The index holds the next two near-term VIX futures contracts at any given time and rolls daily from the first- to second-month contracts in equal fractional amounts to maintain the constant one-month position.

Notably, the methodology is similar to the well-established S&P 500® VIX Short-Term Futures Index, which underlies some investable volatility products for U.S. markets.

Putting the Index to Work

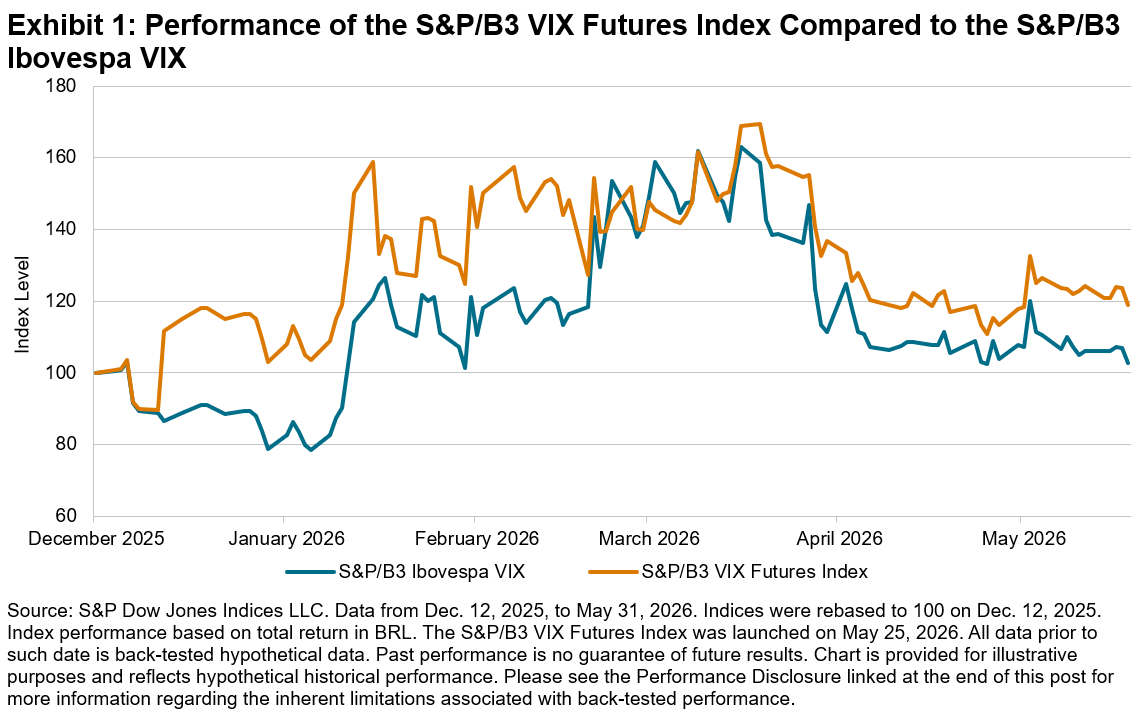

The S&P/B3 VIX Futures Index serves an important function in the equity volatility ecosystem. Because VIX itself is a statistical metric that is not replicable, a rolling futures index could be used to support volatility ETFs, structured products and other financial products. However, it is important to understand that while the S&P/B3 VIX Futures Index tends to be highly correlated to the spot S&P/B3 Ibovespa VIX (see Exhibit 1), the two indices are unlikely to experience similar percentage returns—particularly over longer periods of time. This is the result of a couple major factors.

First, the spot S&P/B3 Ibovespa VIX measures real-time market expectations of Ibovespa volatility, whereas the S&P/B3 VIX Futures Index reflects the forward price of volatility one month out; hence, the S&P/B3 VIX Futures Index will typically experience smaller changes in magnitude compared to the spot VIX.

Second, VIX futures markets are typically in contango—front-month contracts tend to trade cheaper than next-month contracts. As the S&P/B3 VIX Futures Index rolls from the cheaper to the pricier contract, it experiences a negative roll yield that erodes value over time. This is why volatility products built on the index are typically held for short-term periods.

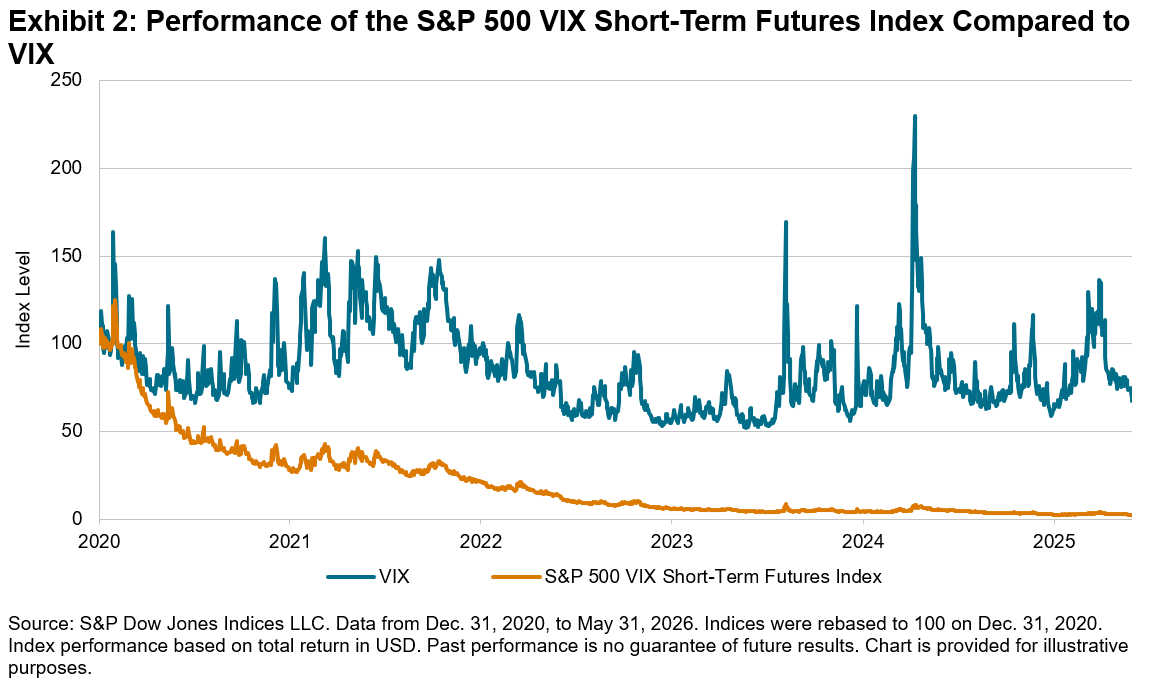

This dynamic is evident in the more established U.S. market (see Exhibit 2), where the S&P 500 VIX Short-Term Futures Index has steadily decayed toward zero since 2020, even as the spot VIX continues to oscillate within its historical range, highlighting how negative roll yield can erode the value over time.

A New Chapter for Brazilian Volatility Markets

The launch of the S&P/B3 VIX Futures Index marks an important milestone for Brazil’s derivatives market. The index follows the approach of the S&P 500 VIX Short-Term Futures Index, which underlies an ecosystem of tradable volatility products built on S&P 500 volatility. With Brazil entering an uncertain political phase ahead of upcoming elections and external headwinds such as U.S. tariffs, having reliable tools to measure and manage Brazilian market volatility could be essential. In a market defined by uncertainty, the S&P/B3 VIX Futures Index expands the risk management tools available to navigate volatile market cycles.

The posts on this blog are opinions, not advice. Please read our Disclaimers.