Since the launch of the first defined outcome ETF in 2018, defined outcome strategies have moved from the margins to mainstream. In markets shaped by concentration risk, volatility and interest rate uncertainty, strategies that offer market participants upside participation with downside protection—via caps, buffers, floors and outcome periods—may help offset the risk of long-only equity exposure. With defined outcome ETF assets estimated at more than USD 78 billion,1 the need for benchmarks that reflect those strategies with greater precision is greater than ever, and S&P Dow Jones Indices has introduced the S&P 500® Defined Outcome Index Series to meet this need.2

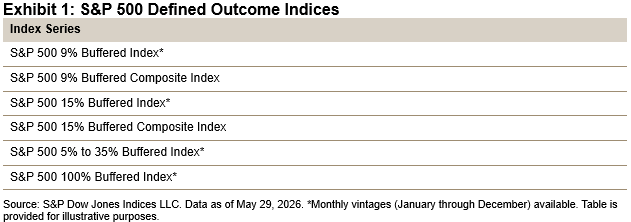

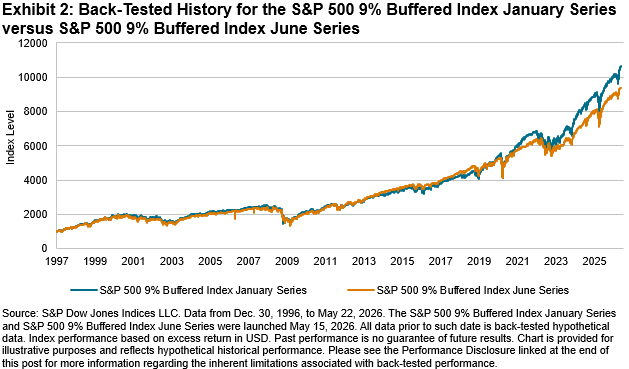

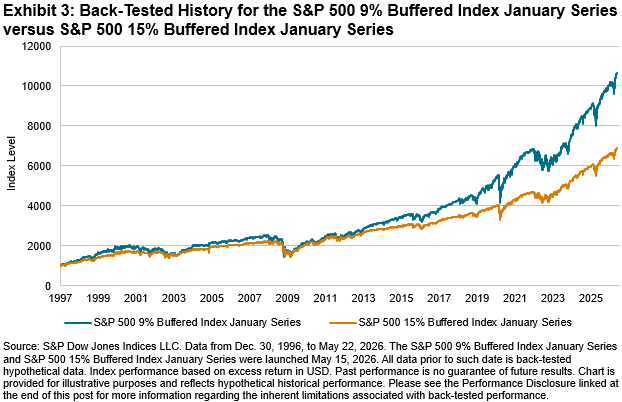

These indices were built to measure options-based outcome structures tied to the S&P 500 with a level of specificity that mirrors how investors use these strategies. Rather than treating defined outcome investing as a single category, the new benchmarks recognize that outcomes vary by downside buffer, upside participation framework and outcome period. The result is a broader index architecture spanning monthly vintages and several distinct exposure profiles, including 9% buffered, 15% buffered, 5% to 35% buffered and 100% buffered strategies, along with composite benchmarks designed to give a wider view across vintages. The indices have back-tested history back to 1996, which provides insight into hypothetical performance. With this data, we are able see how these strategies have performed across multiple market regimes and several key market stress events, including the dotcom bubble and crash, the 2007-2008 Global Financial Crisis and the COVID-19 pandemic.

Timing and structure are both critical elements of defined outcome strategies. A one-year buffered strategy that starts in January is different from one beginning in June. Similarly, a partial buffer and a deep buffer serve different purposes and suit different risk tolerances. Defined outcome strategies represent tradeoffs, as greater downside protection comes at the cost of greater upside potential.

Market participants may use these indices to help match outcome-oriented exposures with client objectives, whether that be mitigating drawdowns, reducing sequence risk or maintaining a more deliberate balance between protection and upside potential. A benchmark family that reflects those distinctions gives market participants a transparent way to compare exposures and better understand potential strategy behavior.

A benchmark should do more than provide a reference point; it should help provide transparency into the mechanics of performance. The dedicated S&P 500 Defined Outcome Index Series provides a more rigorous framework for measuring buffered equity strategies.

1 Morningstar as of year-end 2025.

2 For more information, please see the S&P 500 Defined Outcome Indices Methodology.

The posts on this blog are opinions, not advice. Please read our Disclaimers.