The measurement of active manager performance versus benchmarks is not new. The earliest study dates back to more than 90 years ago, when Alfred Cowles found that “statistical tests of the best individual records failed to demonstrate that they exhibited skill, and indicated that they more probably were results of chance.”1

Forty years later, by the 1970s, financial markets increasingly became dominated by professional investors rather than the retail investors of Cowles’ day. In “The Loser’s Game,” Charles Ellis found that “contrary to their oft articulated goal of outperforming the market averages, investment managers are not beating the market: The market is beating them.”2

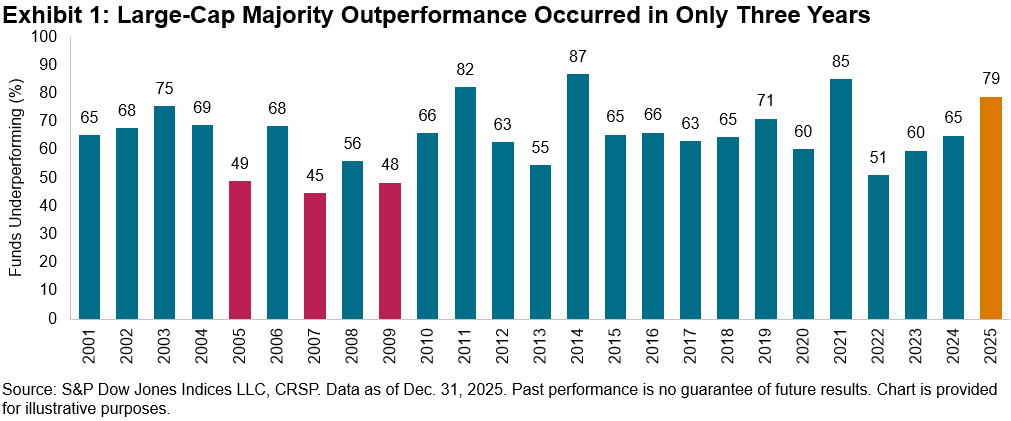

Less than 30 years later, the SPIVA® Scorecard launched in 2002, and it continues to serve as the de facto scorekeeper of the long-standing active versus passive debate. Beating the market is a tall order,3 with only three years of majority outperformance versus the S&P 500® over a 25-year history. For our largest and most closely watched category, 2025 was no exception, with 79% of all active large-cap U.S. equity funds underperforming the S&P 500.4

It is important to note that the underperformance rates shown in Exhibit 1 use the opportunity set available at the beginning of the period as the denominator to account for survivorship bias. We take a simple count of the funds that have survived and beat the index and then report the index outperformance percentage. Therefore, merged or liquidated funds are counted as underperformers.

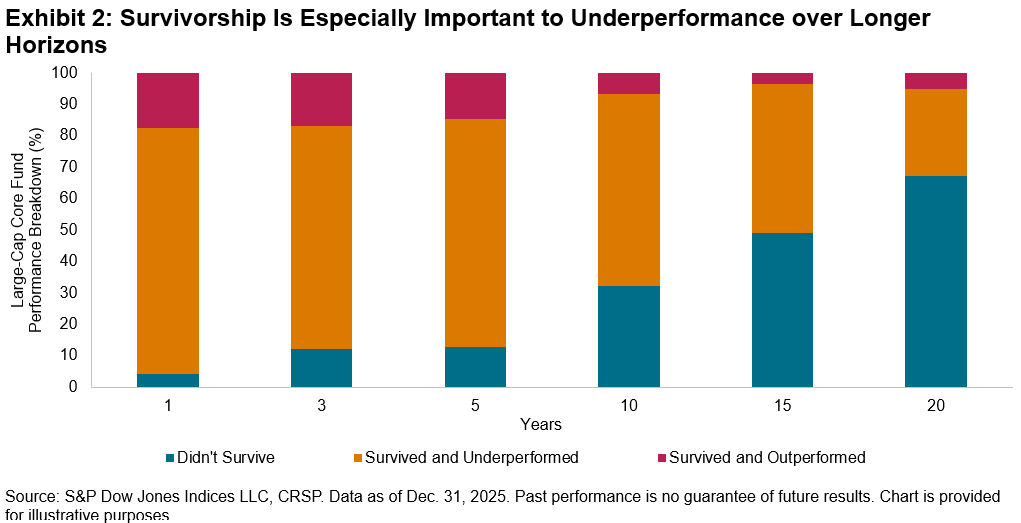

To better understand the impact of survivorship on underperformance, Exhibit 2 shows the breakdown of Large-Cap Core fund performance into three categories: funds that did not survive, funds that survived and underperformed and those that survived and outperformed. Over a one-year period, 82.5% of Large-Cap Care funds underperformed The 500®. Notably, most of this underperformance came from funds that survived but still underperformed, an indication of the challenges of benchmark outperformance regardless of the treatment of merged or liquidated funds.

Over a 20-year period, however, most of the category’s underperformance came from funds that did not survive, highlighting the importance that survivorship plays over longer time horizons. These trends are also indicative of the competitive nature of the business of active management, where winners tend to be rewarded with inflows by asset owners, but losers are generally punished with terminations and are less likely to survive over longer periods.5

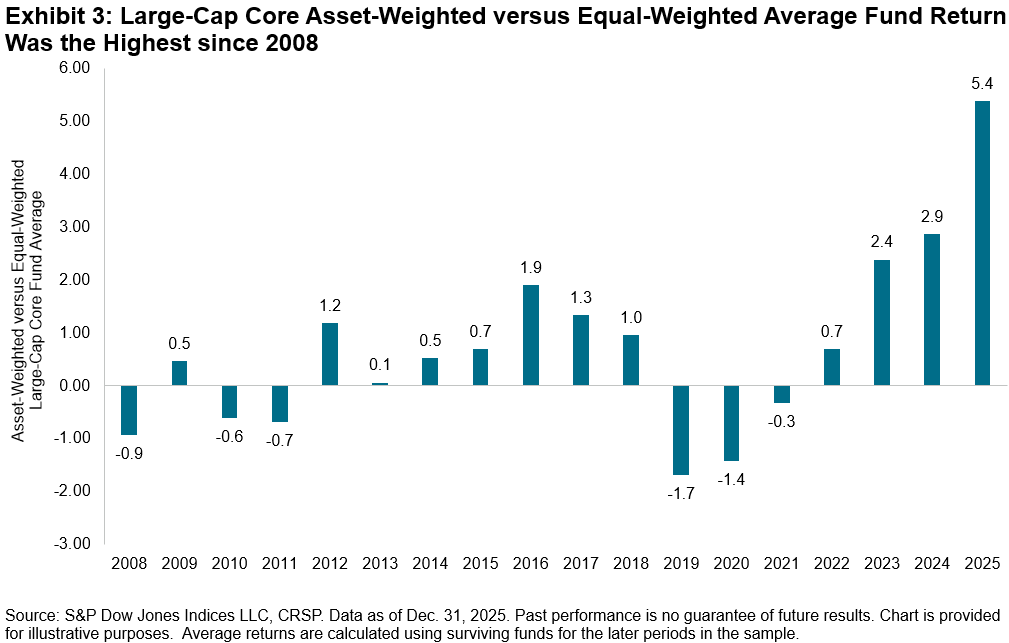

Another feature of our methodology of calculating fund underperformance is that funds of all sizes are treated equally. However, our scorecards show both equal- and asset-weighted average performance for comparison purposes. We observe in Exhibit 3 that the difference in 2025 of 5.4% between Large-Cap Core’s asset-weighted average return of 19.7% and the corresponding equal-weighted average return of 14.3% was the highest since 2008. The fact that larger funds have performed better in recent years, perhaps due to economies of scale or an information advantage, is typical, but unusually heightened compared to history.

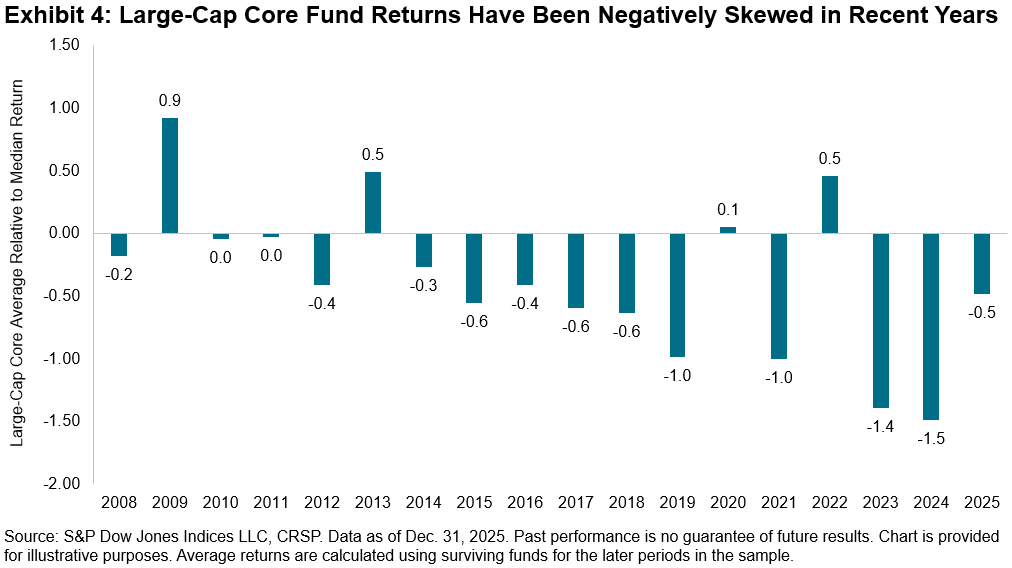

While larger funds have been among the winners in recent years, a negative skew has accompanied the cross section of fund returns. In other words, when a fund’s performance differed significantly from the median, it was more likely to be a significant underperformer. Exhibit 4 shows one measure of the historical skewness of fund excess returns for the Large-Cap Core category—specifically comparing the average return to the median return (reported as the second quartile breakpoint). While the skew was lower than in the prior two years, 2025 continued to witness an average return lower than the median.

Thanks to the rich data set backed by a robust methodology that SPIVA offers, including underperformance rates, survivorship statistics, equal and asset-weighted average returns, quartile breakpoints and more, readers across the globe can measure active manager performance versus the appropriate market benchmarks in a holistic manner. As the scorecard has evolved to expand to 11 regions with coverage across equities and fixed income, the message remains consistent regardless of geography or asset class: Most active managers underperform most of the time. Alfred Cowles would not be surprised.

1 Cowles 3rd, Alfred, “Can Stock Market Forecasters Forecast?” Econometrica, July 1933.

2 Ellis, Charles D., “The Loser’s Game,” Financial Analysts Journal, July/August 1975.

3 For more detail on why active underperformance happens, see Ganti, Anu R., and Craig J. Lazzara, “Shooting the Messenger,” S&P Dow Jones Indices LLC, Nov. 22, 2022.

4 Ganti, Anu R. et al., “SPIVA U.S. Year-End 2025 Scorecard,” S&P Dow Jones Indices LLC, March 3, 2026.

5 Over consecutive five-year periods, in almost every single reported equity and fixed income category, the worst-performing quartile saw the highest proportion of funds that were subsequently merged or liquidated. See Ganti, Anu R. et al., “U.S. Persistence Scorecard: Year-End 2025,” S&P Dow Jones Indices, May 7, 2026.

The posts on this blog are opinions, not advice. Please read our Disclaimers.