Direct Lending Has Become a Core Segment of Private Credit

Private credit has expanded in recent years, with the market reaching an estimated USD 2.28 trillion at year-end 2025 and projected to grow to approximately USD 4.5 trillion by 2030.1 Within this expansion, direct lending has emerged as the dominant strategy, reshaping how companies access capital and how investors generate yield. Direct lending refers to loans provided directly to companies by private and public investment funds, including business development companies, rather than traditional banks, the broadly syndicated loan (BSL) market or public debt markets. These privately negotiated loans—typically extended to middle-market and sponsor-backed businesses—offer floating-rate income and structural protections for lenders. What was once a niche allocation has evolved into a mainstream source of corporate financing and institutional yield generation.

These privately negotiated loans are typically extended to sponsor-backed companies and are characterized by:

- Floating-rate income profiles

- Senior-secured positioning

- Strong covenant and structural protections

- Bilateral structuring flexibility

As the market has scaled, so too has its importance in institutional portfolios.

A Collaboration between S&P DJI and Lincoln International Enables a Systematic View of Direct Lending3

As direct lending has become a core pillar of corporate credit, the need for consistent, transparent and rules-based measurement has grown increasingly urgent. Historically, investors have faced significant data constraints:

- Limited availability of standardized loan-level information

- Absence of investable or benchmark-quality indices

- Limited visibility into risk composition and structural characteristics

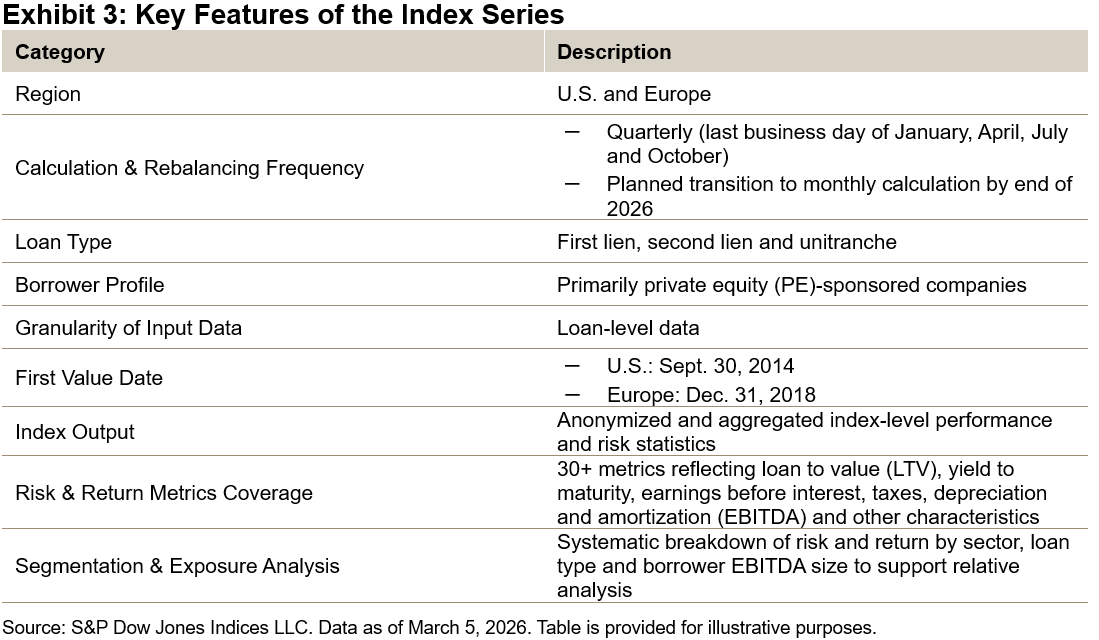

To address these challenges and enhance transparency, S&P Dow Jones Indices (S&P DJI) and Lincoln International formed a collaboration to launch the S&P Lincoln Senior Debt Index Series,3 comprising:

- S&P Lincoln U.S. Senior Debt Index

- S&P Lincoln Europe Senior Debt Index

By combining Lincoln International’s extensive private loan valuation database with S&P DJI’s expertise in index design, governance and calculation, the series delivers a systematic measure of the fair value performance of direct lending investments across the U.S. and Europe.

- Designed to Enhance Transparency and Institutional Confidence: The S&P Lincoln Senior Debt Index Series is structured to elevate transparency and analytical rigor within direct lending.

- Broad Market Coverage: Lincoln International’s valuation database represents approximately USD 220 billion of the direct lending loan market across the U.S. and Europe.

- Institutional-Grade Valuation Framework: Valuations are informed by Lincoln International and incorporate detailed portfolio company operating data provided by fund clients. All valuations conform to fair value standards under both U.S. GAAP and IFRS.

- Robust Governance: The index methodology is transparent, rules-based and administered independently by S&P DJI, with systematic rebalancing and oversight.

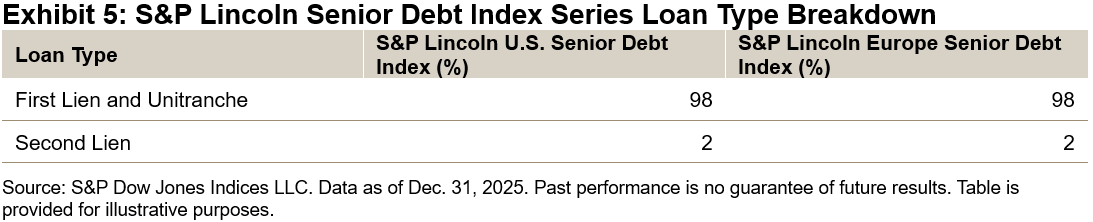

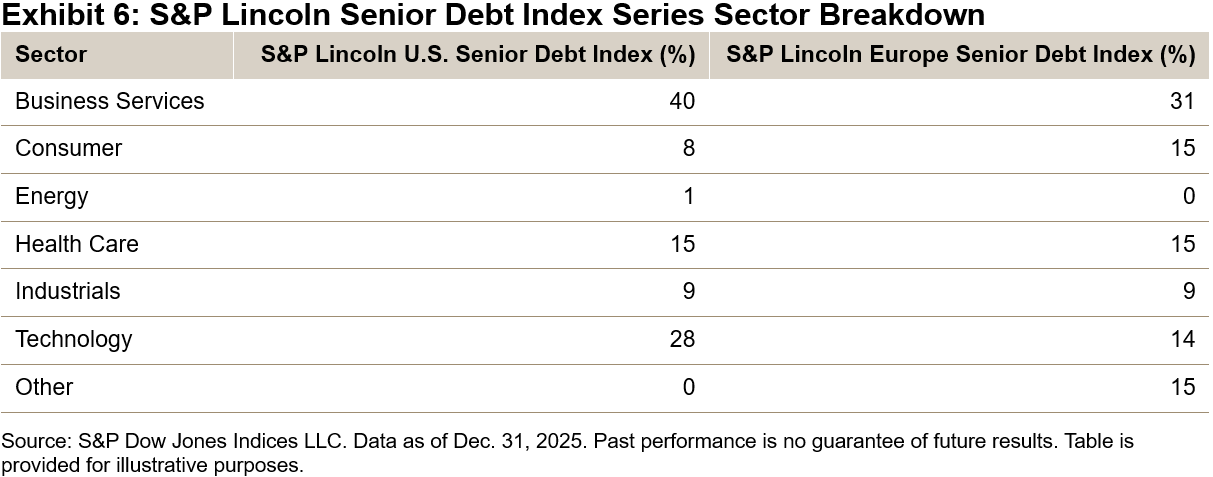

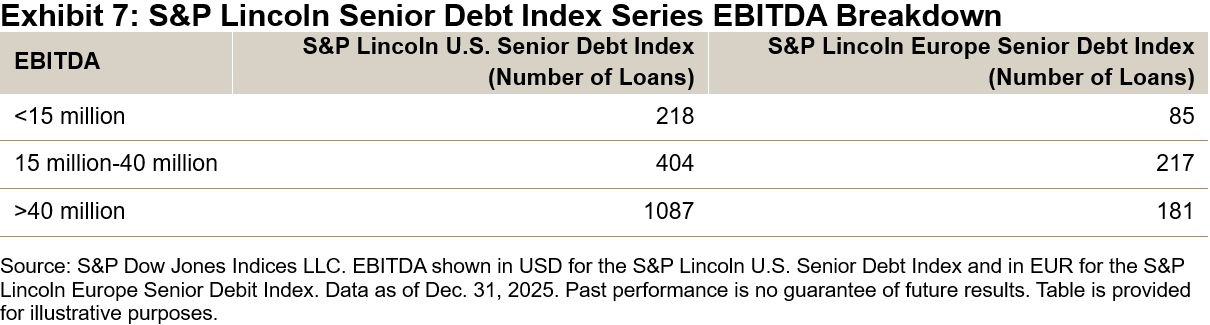

- Portfolio Characteristics and Composition: The indices reflect meaningful diversification across sectors, borrower size and loan structures.

- Average Principal Balance (As of Dec. 31, 2025)

- U.S.: USD 399 million

- Europe: EUR 142 million

- Average EBITDA Size (As of Dec. 31, 2025)

- U.S.: USD 101 million

- Europe: EUR 52 million

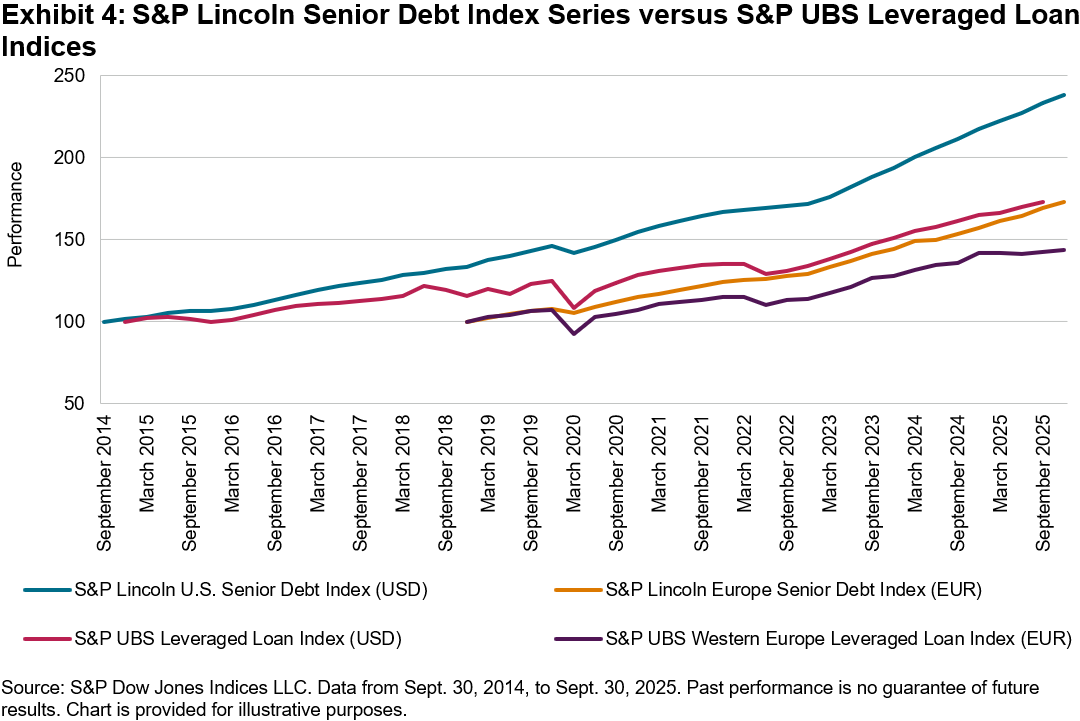

The S&P Lincoln Senior Debt Index Series outperformed leveraged loans over the last 10 years by 2.72% annually (U.S.) and over the last 7 years by 2.81% annually (Europe), as measured by the S&P Lincoln U.S. Senior Debt Index, S&P Lincoln Europe Senior Debt Index, S&P UBS Leveraged Loan Index and the S&P UBS Western Europe Leveraged Loan Index. This difference is driven by variations in company size, credit quality and liquidity.

The S&P Lincoln Senior Debt Index Series Complements BSL and BDC Benchmarks

As direct lending has grown in scale and institutional relevance, it increasingly sits alongside other leveraged lending segments, such as the BSL market, which represents approximately USD 1.4 trillion in the U.S.4

Both BSLs and direct lending provide senior-secured, floating-rate financing to leveraged borrowers and support similar corporate activities. However, their market structures differ. BSLs benefit from observable secondary market pricing, while direct lending loans are privately originated, negotiated bilaterally and typically held to maturity with limited trading activity. These structural distinctions mean that direct lending returns reflect not only credit fundamentals and seniority, but also an illiquidity premium and the value of structuring flexibility.

Conclusion

Private credit has evolved from a bespoke, opaque niche into a globally significant and institutionally scrutinized asset class. As the market expands in scale and systemic importance, the demand for transparency, governance and standardized measurement has intensified.

The S&P Lincoln Senior Debt Index Series represents an important milestone in the maturation of direct lending. By providing systematic, rules-based and independently administered measurement, the series enables:

- Improved performance benchmarking

- Enhanced risk transparency

- More informed asset allocation decision

- Strengthened reporting and governance frameworks

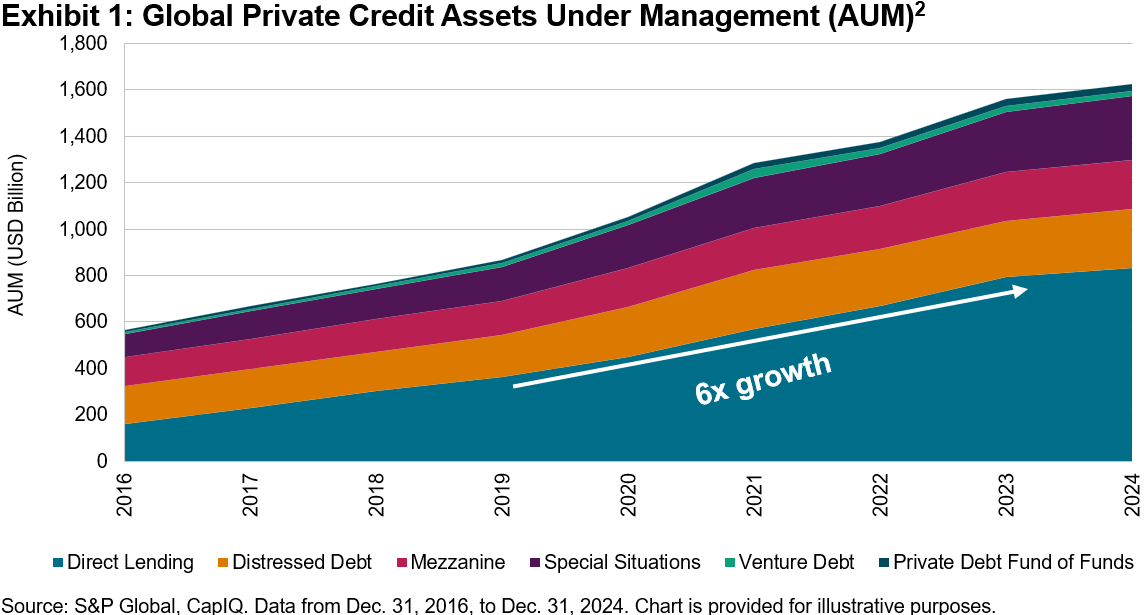

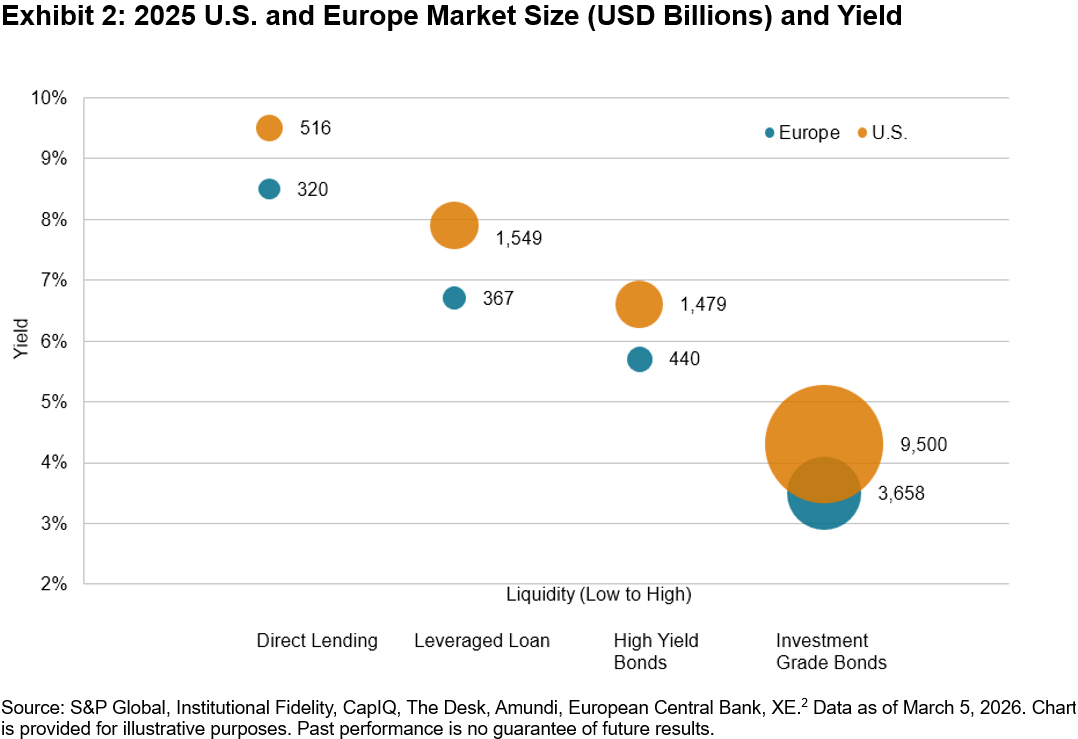

As demonstrated in Exhibits 1 and 2, private credit is now a major source of global capital formation. With this growth comes the responsibility to provide clarity and comparability. The S&P Lincoln Senior Debt Index Series helps establish the analytical infrastructure necessary for the next phase of the market’s evolution.

1 Guevarra, Joyce; Hiteshbhai Bharucha, Neel. “Private credit gains ground among top private equity managers.” S&P Global. Nov. 13, 2025.

2 U.S. leveraged loan and high yield bond yield and size: Presentation Title

U.S. & Europe Direct lending yield: S&P Lincoln Senior Debt Index Series.

U.S. & Europe Direct lending market size: CapIQ, S&P Global.

U.S. and Europe investment grade bonds market size: Barnes, Dan. IG issuance across US and Europe up 20% on five-year average. The Desk. Dec. 3,2025.

U.S. investment grade bonds yields: Leveraged Loan Market Review. Fidelity. Q4, 2025.

Europe leveraged loan and high yield bonds market size and yield: Valliere, Thierry, et al., 2025. Unlocking the potential of European Leveraged Loans. Amundi. March 20, 2025.

Europe investment grade bonds yield: Euro area yield curves. European Central Bank, Eurosystem.

Exchange rate data on Feb. 27, 2025, as sourced by XE.

3 S&P Dow Jones Indices and Lincoln International Unveil New Benchmarks for the Private Loan Market with Launch of S&P Lincoln Senior Debt Indices. S&P Dow Jones Indices. Feb. 23, 2026.

4 Wolfson, Kevin; Taylor, Joseph. Private Credit vs. Broadly Syndicated Loans: Not a Zero-Sum Game. PineBridge Investments. July 1, 2024.

The posts on this blog are opinions, not advice. Please read our Disclaimers.