Japanese dividend payouts are meaningfully higher in cash terms than they were a decade ago, bringing Japan more in line with other developed markets. Importantly, dividend growth is now increasingly anchored in formal dividend policy. This shift matters for market participants seeking both yield and exposure to Japanese equity markets by setting expectations around dividend sustainability.

Much of this evolution has been due to improved corporate governance and stewardship standards in the 2010s as well as the normalization of payout ratios, and capital efficiency reforms introduced by the Tokyo Stock Exchange in 2023.1 These reforms have sharpened management’s focus on the cost of capital and share price performance. As a result, dividend increases, progressive dividend policies and share buybacks have become more common. Many companies now explicitly commit to maintaining or increasing dividends, contributing to greater stability in Japan’s dividend market.

On Dec. 15, 2025, the Dow Jones Japan Select Dividend Index was launched to track companies with higher dividend yields and more sustainable dividend profiles in Japan.

Index Construction and Methodology

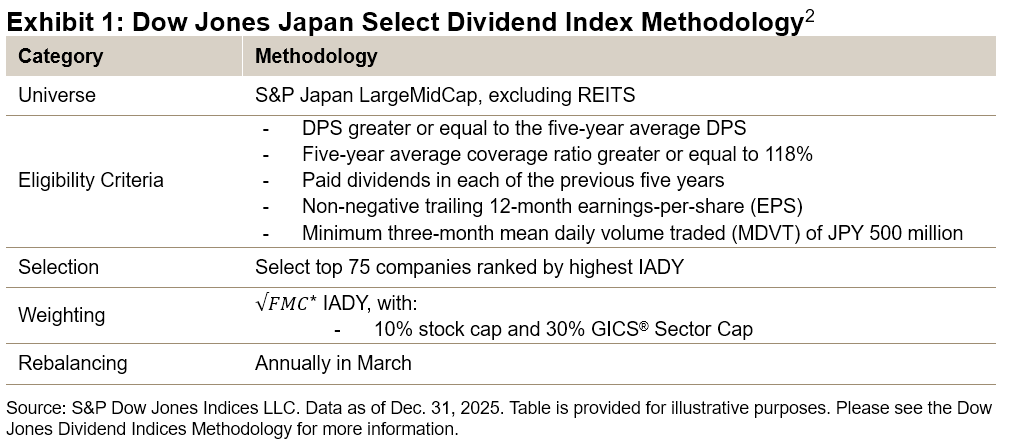

The Dow Jones Japan Select Dividend Index methodology (see Exhibit 1) follows the established approach of the Dow Jones Select Dividend Index Series. The starting universe is the S&P Japan LargeMidCap, excluding REITs. From this broad universe, a series of eligibility screens is applied to identify consistent dividend payments, adequate dividend coverage and higher yields.

Stocks passing these screens are then ranked by indicated annual dividend yield (IADY) with the top 75 selected subject to a buffer to reduce turnover. Constituents are weighted using the square root of free-float market capitalization (FMC) multiplied by IADY.

Dividend Yield Characteristics

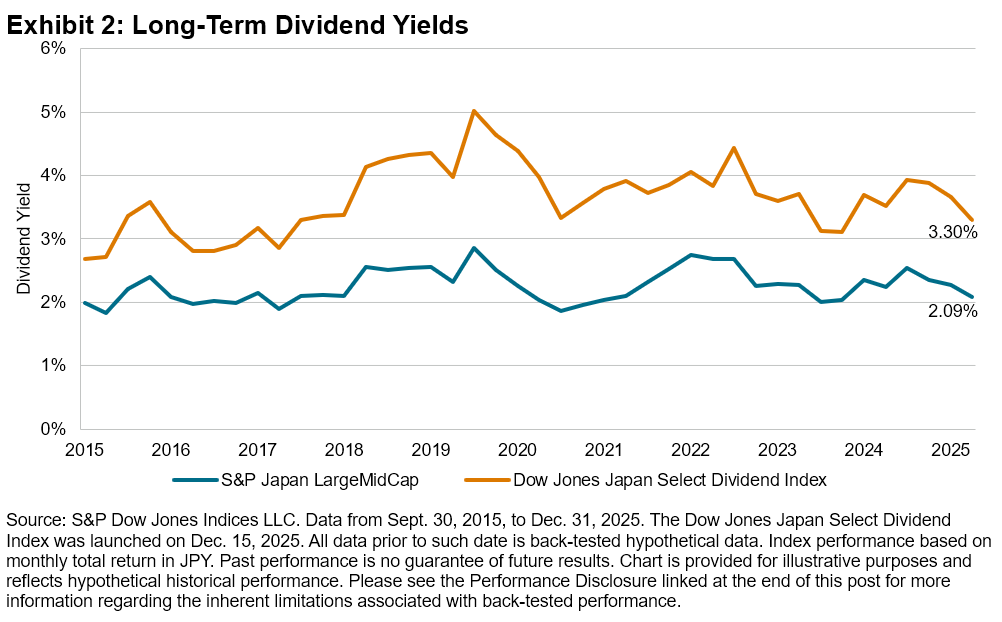

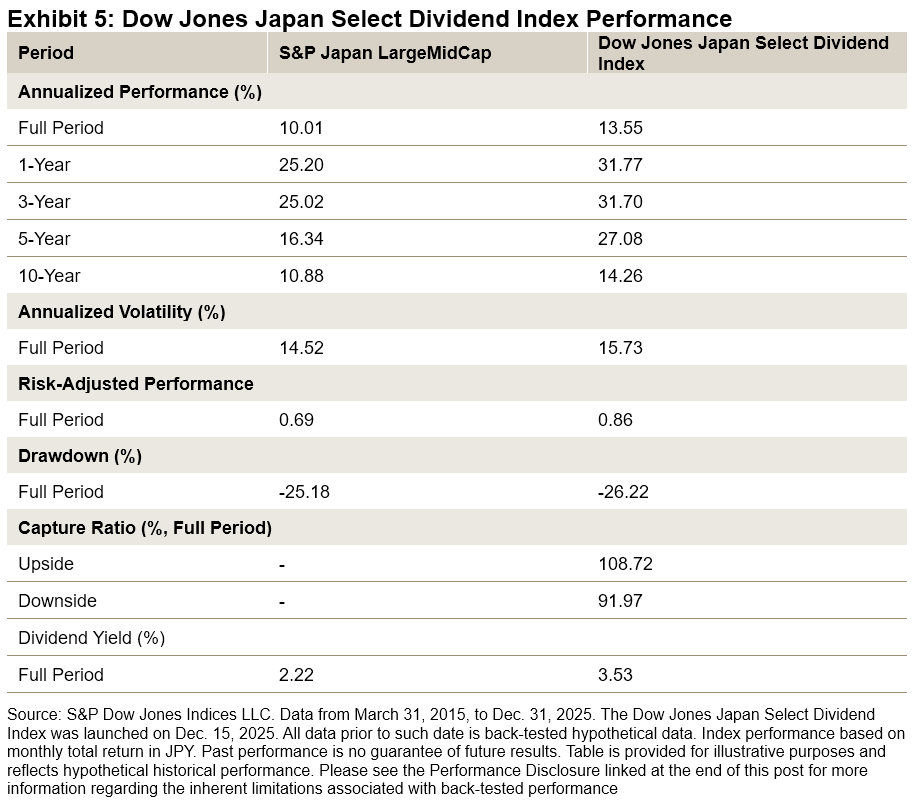

As shown in Exhibit 2, the long-term average dividend yield of the index since 2015 is 3.53%, approximately 130 bps higher than the benchmark universe.

As of year-end 2025, the index had a dividend yield of 3.30%, around 120 b above the benchmark, although slightly below its long-term average differential.

A Decade of Dividend Growth in Japan

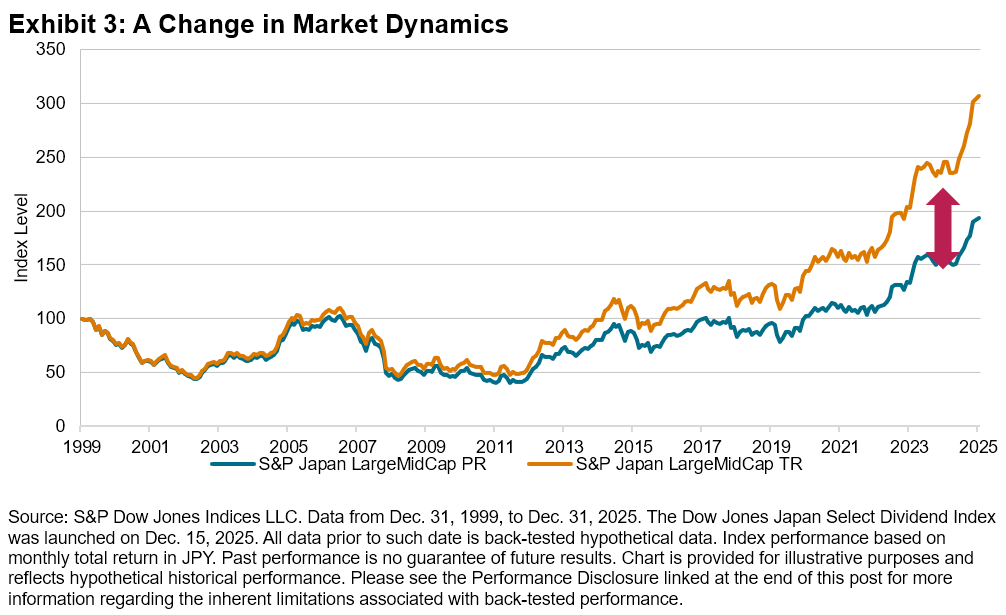

The Japanese market has witnessed significant dividend growth over the past decade. As illustrated in Exhibit 3, dividends gained prominence following the reforms of the 2010s, leading to larger and more consistent dividend payments, resulting in a widening between the total return (incorporating dividends) and price return versions of the benchmark, based on back-tested analysis.

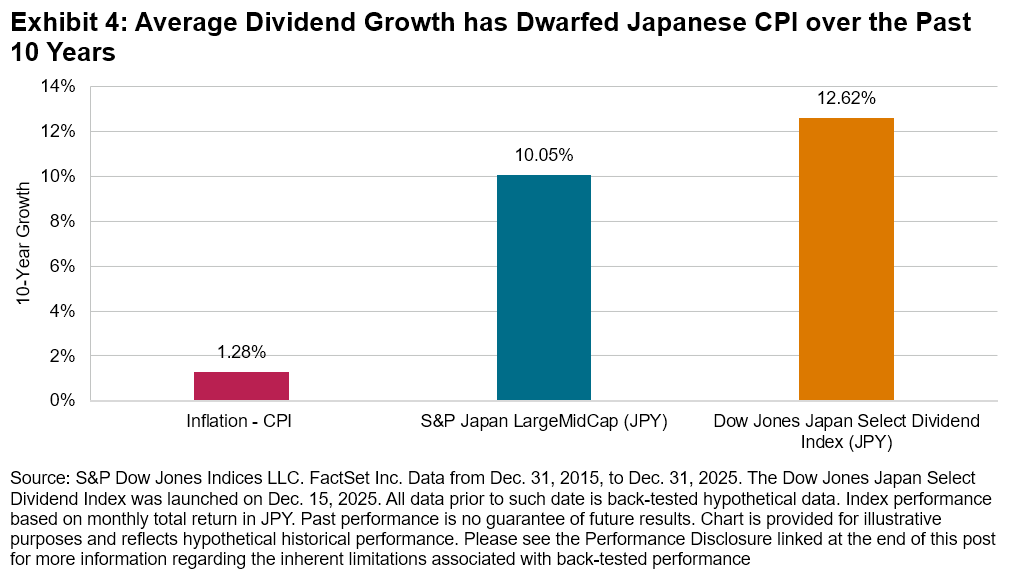

Exhibit 4 reveals that the Dow Jones Japan Select Dividend Index had an average annual dividend growth rate of 12.62% during this period, surpassing the benchmark universe by approximately 260 bps and significantly outpacing Japanese inflation. Irrespective of this growth continuing into the future, it underscores Japan’s market dynamics aligning more closely with developed market standards.

Long-Term Outperformance

Back-tested results show that the Dow Jones Japan Select Dividend Index has outperformed its benchmark universe on both long- and short-term horizons, while also delivering higher risk-adjusted performance. The index has provided a degree of defensiveness, with a downside capture ratio of 92%, while participating in rising markets as reflected by its upside capture ratio.

Sector Weights

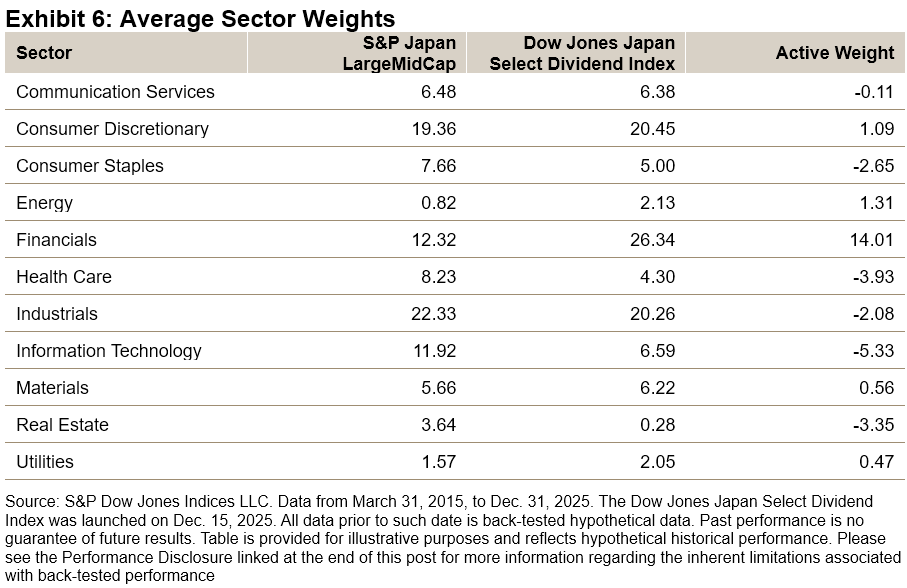

Over the long term, the index’s GICS sector weights have been concentrated in Financials, Industrials and Consumer Discretionary. Financials represent the largest active overweight, at 14.01%. Industrials and Consumer Discretionary also carry meaningful weights in the Japanese benchmark, resulting in relatively low active positions.

The largest active underweights are in Information Technology and Health Care, reflecting the index’s focus on income-oriented sectors rather than growth-oriented industries.

Conclusion

By systematically targeting high-yielding companies with demonstrated dividend stability, the Dow Jones Japan Select Dividend Index reflects Japan’s evolving income landscape. Based on back-tested data, its combination of high dividend yields, strong dividend growth and long-term risk-adjusted performance highlights the growing relevance of dividend strategies within Japanese equities.

1 Japan Exchange Group – Follow-up of Market Restructuring

2 Dow Jones Dividend Indices Methodology

The posts on this blog are opinions, not advice. Please read our Disclaimers.