Climate-focused institutional investors face the challenge of reducing carbon exposure while maintaining broad market representation and the ability to closely track the performance of the underlying market. The S&P 500® CTB Base+ Index offers a practical solution that can be used to measure the performance of constituents from the underlying index that meet specific climate and sustainability criteria.

CTB versus PAB: Understanding the Frameworks

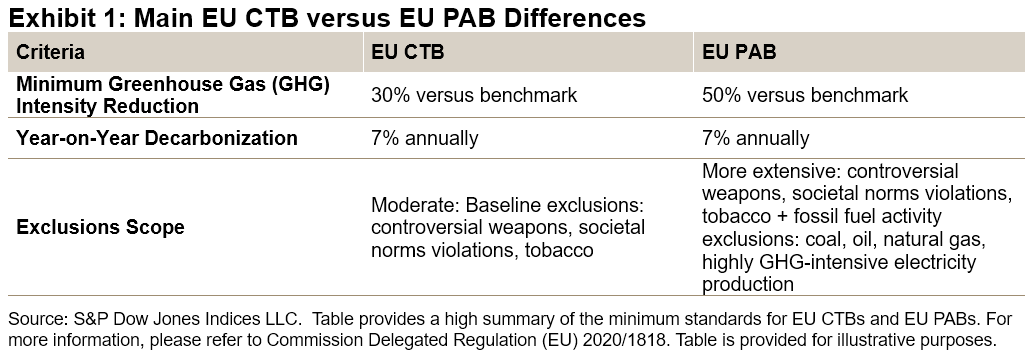

The EU offers two climate benchmarks: the EU Climate Transition Benchmarks (EU CTB) and the EU Paris-Aligned Benchmarks (EU PAB). Both benchmarks support the shift to a low-carbon economy, but they differ in their initial decarbonization levels and exclusion criteria.

S&P Dow Jones Indices (S&P DJI) offers index solutions that align with both the EU CTB and EU PAB frameworks,1 allowing institutions to select the approach that best fits their purpose, risk tolerance and climate objectives.

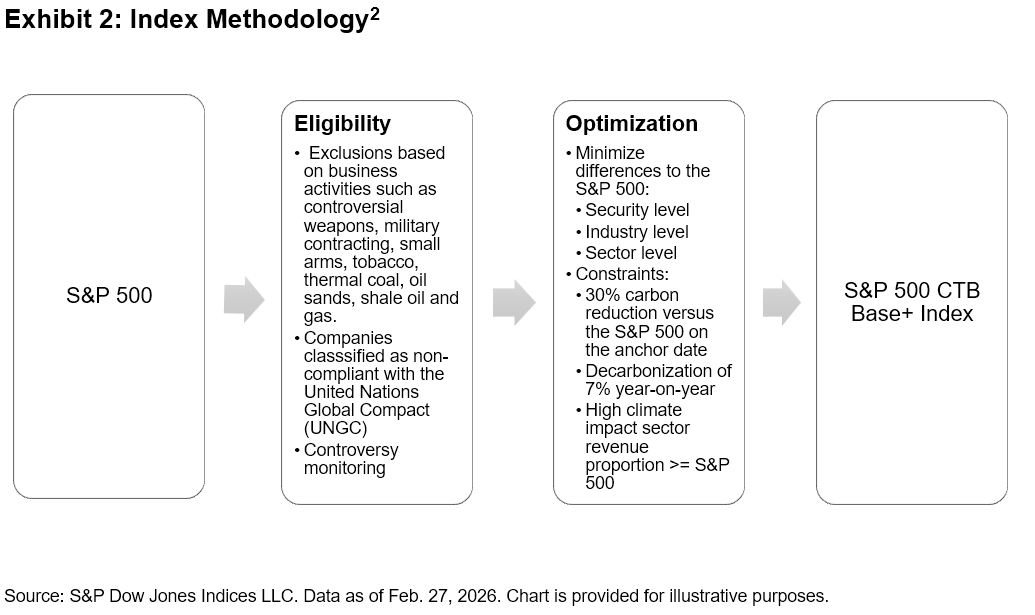

Building on the EU CTB minimum standards, the S&P 500 CTB Base+ Index adds exclusions for shale oil and gas extraction, stricter thresholds for military weapons, group-level military contracting exclusions and additional constraints on Scope 1 and 2 Weighted-Average Carbon Intensity (WACI) targets and decarbonization trajectory. Using our proprietary glass-box optimization approach, the index selects and weights constituents from the S&P 500 that meet low-carbon transition criteria while minimizing deviations from the underlying index.

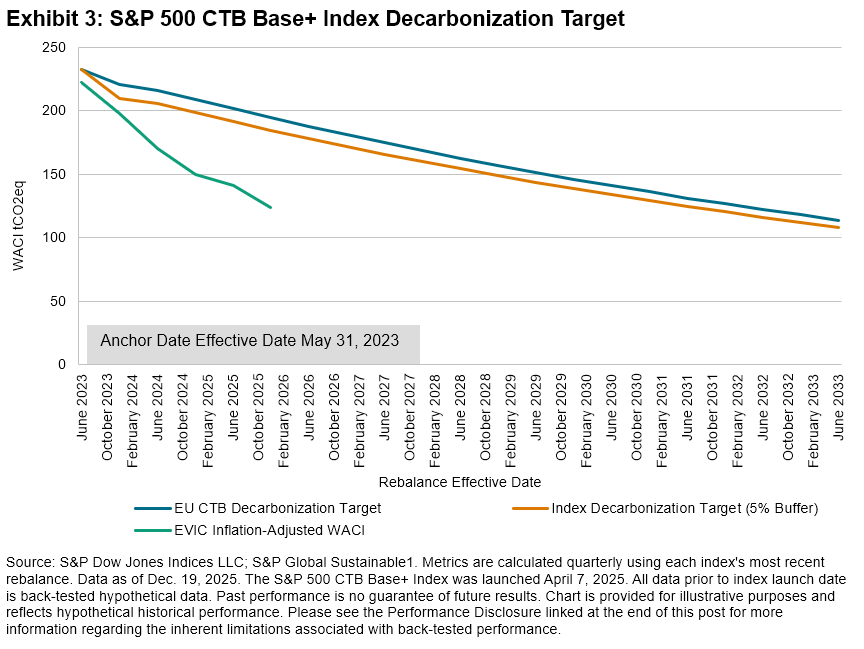

Exhibit 3 shows the decarbonization path of the S&P 500 CTB Base+ Index, which is represented by the index-level enterprise value including cash (EVIC) inflation-adjusted WACI considering Scope 1, 2 and 3 emissions (green line),3 the minimum standards for Scope 1, 2 and 3 emissions (blue line) and a 5% buffer (gold line), anchored to May 31, 2023. The impact of additional restrictions on controllable emissions (Scope 1 and 2) may become more evident.4

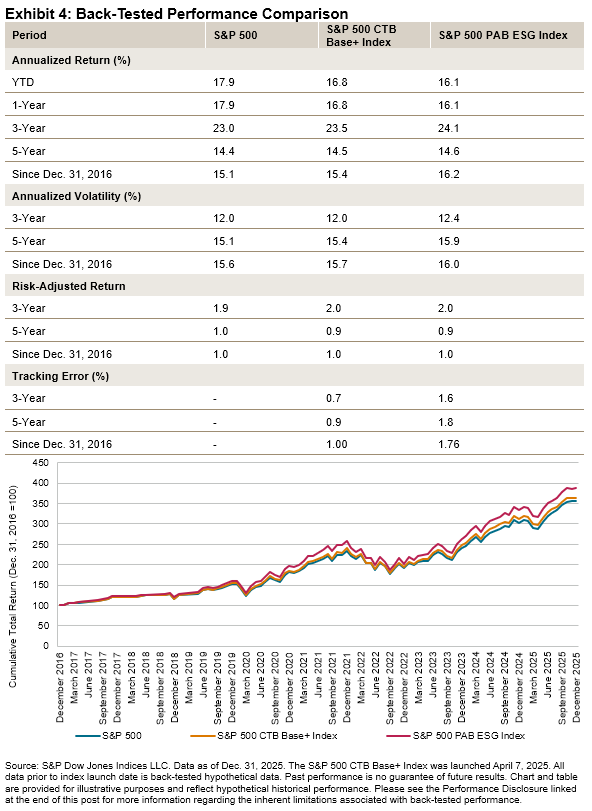

To visualize the potential benefits of the S&P 500 CTB Base+ Index, Exhibit 4 compares it with the S&P 500 PAB ESG Index, which exceeds the EU PAB minimum standards. The S&P 500 CTB Base+ Index has shown historical performance similar to the S&P 500, with slightly lower volatility and tracking error than the S&P 500 PAB ESG Index due to a broader set of constituents.

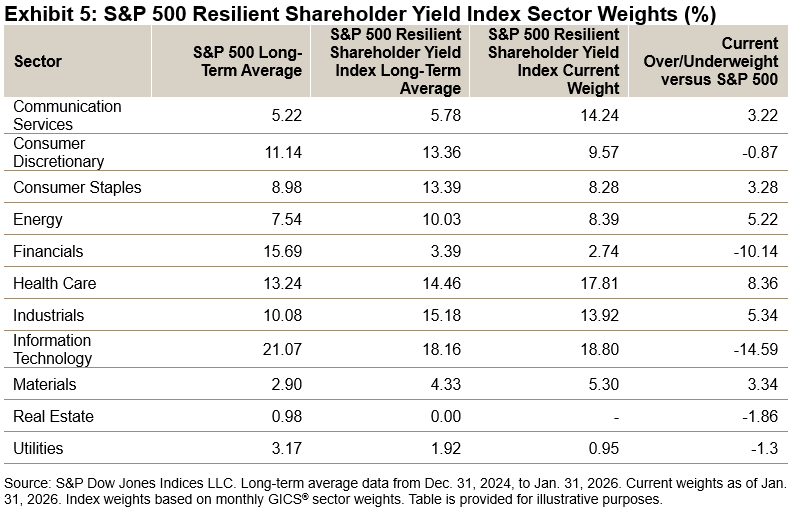

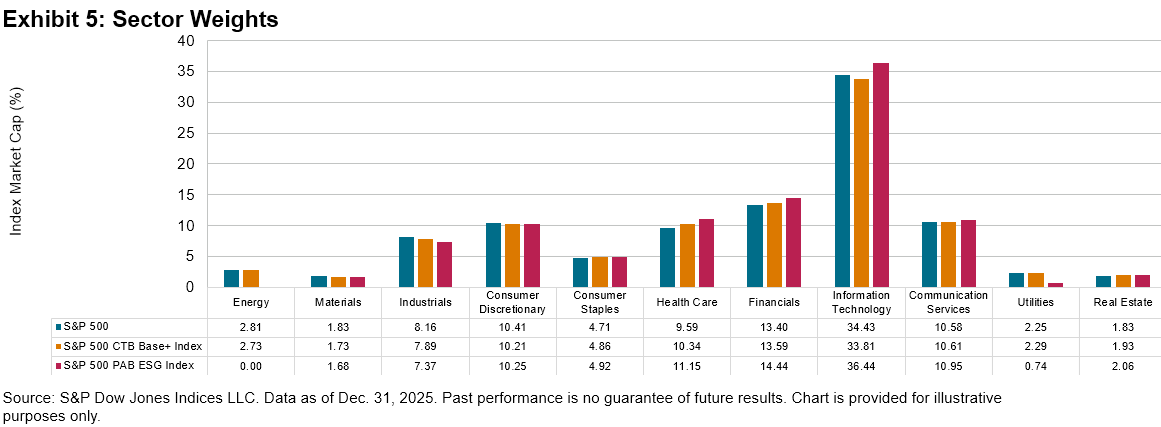

To achieve effective decarbonization requires directing capital toward companies that are actively reducing emissions, not just to those companies that are already low-carbon emitting. The minimum standards for EU CTBs offer a less exclusionary approach that helps maintain exposure to hard-to-abate sectors that are transitioning. Considering our example, the S&P 500 CTB Base+ Index mitigates sector biases, in contrast to stricter alternatives like the S&P 500 PAB ESG Index, which often underweight or exclude sectors such as Energy and Utilities (see Exhibit 5).

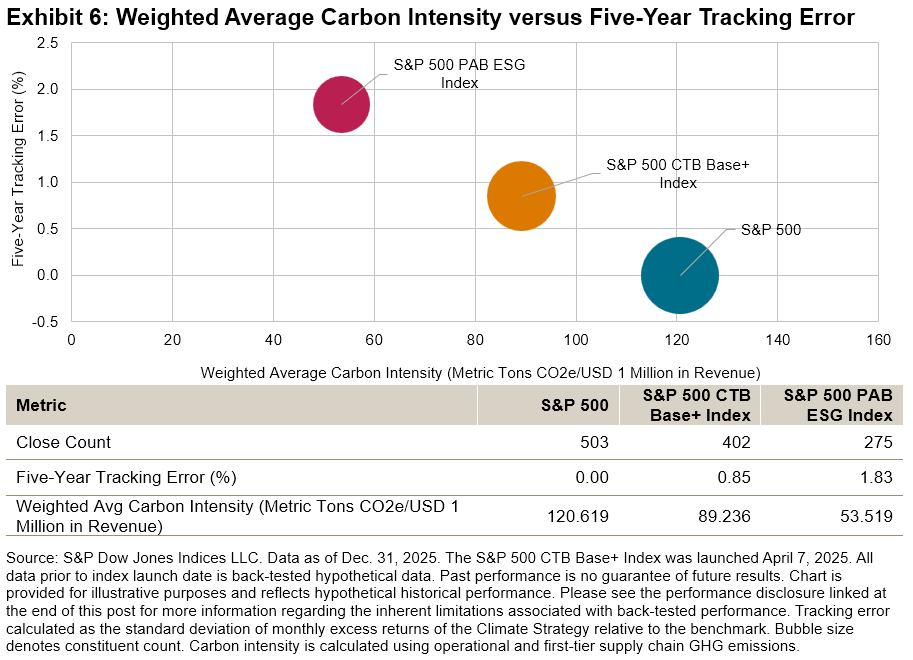

As an index adopts less-stringent exclusions and decarbonization goals, such as those contained in the S&P 500 CTB Base+ Index compared to the S&P 500 PAB ESG Index, a greater number of constituents become eligible, resulting in a reduced tracking error.

In summary, the S&P 500 CTB Base+ Index can potentially offer a pragmatic tool for climate-focused investors to align with the EU CTB minimum standards while potentially maintaining lower tracking error and offering a broader diversification when compared to EU PABs.

1 EU Climate Benchmarks based on the S&P 500 universe include indices such as S&P 500 PAB ESG Index, S&P 500 PAB ESG+ Index, S&P 500 PAB Sustainability Screened Index, S&P 500 CTB Index, S&P 500 CTB Base Pathway-Aligned ESG Index, S&P 500 CTB Base ESG Index and S&P 500 CTB Base+ Index.

2 For the full list of exclusions see the index methodology.

3 EVIC Inflation-Adjusted WACI. For more information on how the WACI is adjusted for EVIC inflation, see “Inflation Adjustment” in Section 3, Part 4 of the “EU Required ESG Disclosures Appendix” in the S&P Equity Paris-Aligned & Climate Transition Index Family Benchmark Statement. FAQ: EU Low Carbon Benchmark Regulation; S&P DJI Equity Sustainability metrics reference guide.

4 The forward-looking decarbonization trajectories for indices are calculated using the same sources of data as the weighted-average carbon intensity metrics calculated and disclosed elsewhere in the S&P DJI EU Low Carbon Benchmark Disclosure Report: The S&P Global Sustainable1 Environmental and Scope 3 datasets, and FactSet EVIC data.

The posts on this blog are opinions, not advice. Please read our Disclaimers.