As 2025 draws to a close, U.S. large caps boast impressive gains: after a rocky start that saw a 19% drawdown, the S&P 500® is up 18% including dividends, as of Dec. 12, significantly above its annualized total return of 10.8% since inception in 1957. The U.S. bellwether also recorded 37 all-time highs this year.

The largest of blue chips continued to drive The 500®, although the index’s performance this year has been less top heavy than in 2024: year-to-date, the top 20 stocks by market capitalization contributed 61% of returns, less than last year’s 68%. Nevertheless, this year’s statistics are still on the high side in a historical context.

As a consequence of their robust returns in recent years, the weight of the 20 largest stocks in The 500 has increased from 37% to 48% since 2020. That said, mega caps earned the increase in their weights: their combined contribution to S&P 500 forward earnings rose from 32% to 42% over the past five years. Thus, the ratio of the top 20 stocks’ index weight to their projected share of S&P 500 net income was unchanged from 2020 to Q3 2025.

Turning to markets outside of U.S. large caps, gold’s performance immediately stands out both in absolute terms and relative to its own historical returns. The yellow metal soared 62% this year compared to a compound annual return of 7% over the previous 30 years, placing this year’s performance more than three standard deviations above the historical average. The S&P Developed Ex-U.S. BMI also had an exceptionally strong year: its 33% performance, including dividends, is over one standard deviation above its 30-year average of 6%. U.S. small caps, on the other hand, have had a slightly below-average year, up just 9% YTD.

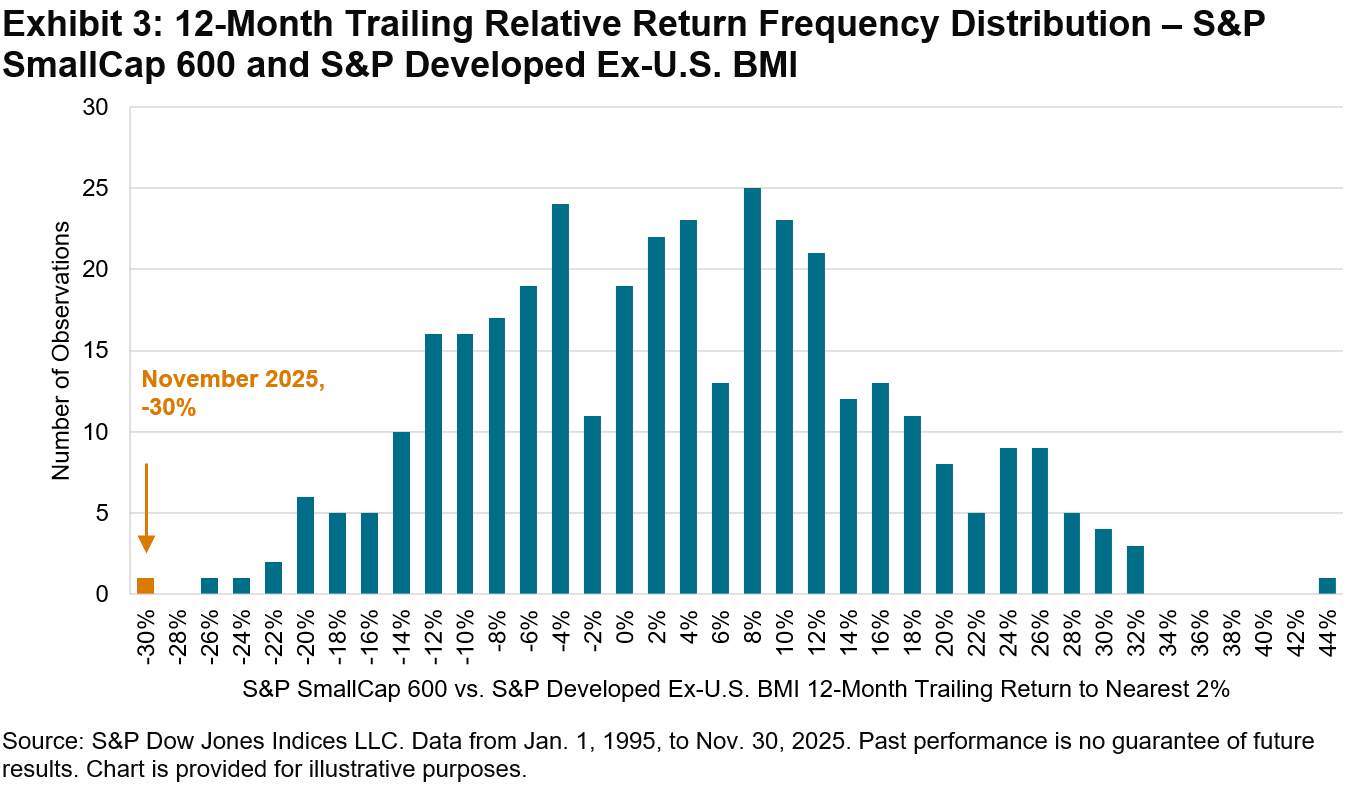

The combination of strong developed ex-U.S. performance and below par U.S. small-cap performance culminated in a significant differential between these two segments over the past 12 months. By the end of November, the S&P SmallCap 600® trailed the S&P Developed ex-U.S. BMI by 30%, the most of any 12-month period since January 1995.

Despite this year’s strong run for developed non-U.S. equities, their valuation has remained more compelling relative to the U.S.: the S&P World Ex-U.S. Index is currently trading at a forward price/earnings (P/E) ratio of 16.7, a discount of 9 points compared to U.S. equities. Many European equity markets are even cheaper, with Italy, Spain and the U.K. all trading below a P/E multiple of 15 as of the end of Q3 2025.

Notwithstanding this year’s impressive returns, some market watchers may feel as I do—although the scoreboard is telling a different story, the year felt volatile and even like a downturn. Such sentiment makes sense in one respect: as the S&P 500 continued to rise, there was never any real let-up in tension during the year; trade-related worries gave way to concerns about the labor market, which then shifted to questions about the payoff of AI-related corporate investments. Exhibit 2 illustrates the lowest end-of-day VIX® reading for each calendar year dating back to 2000. In 11 of the past 13 years, VIX dipped below its long-term mode of 14 at least once, but this year, we never saw that kind of breather.

As 2026 approaches and the Q4 2025 corporate earnings season draws closer, it remains to be seen whether developed ex-U.S. equities will continue to benefit from their lower valuation relative to U.S. markets or whether the coming year will mark a reversal of relative performance in global equity markets. In any case, attempting to forecast market outcomes for 2026 may prove futile, as the best guess of future returns is not dictated by the most recent past.

The posts on this blog are opinions, not advice. Please read our Disclaimers.