Amid macroeconomic uncertainty and elevated volatility, the S&P 500® has experienced a notable decline. In the challenging market conditions from Dec. 31, 2024, to April 4, 2025, the S&P 500 Quality Index not only outperformed the S&P 500 but also showcased its defensive characteristics, which have been evident throughout its history. In this blog, we will explore the performance, attribution and key characteristics of the S&P 500 Quality Index.

Performance

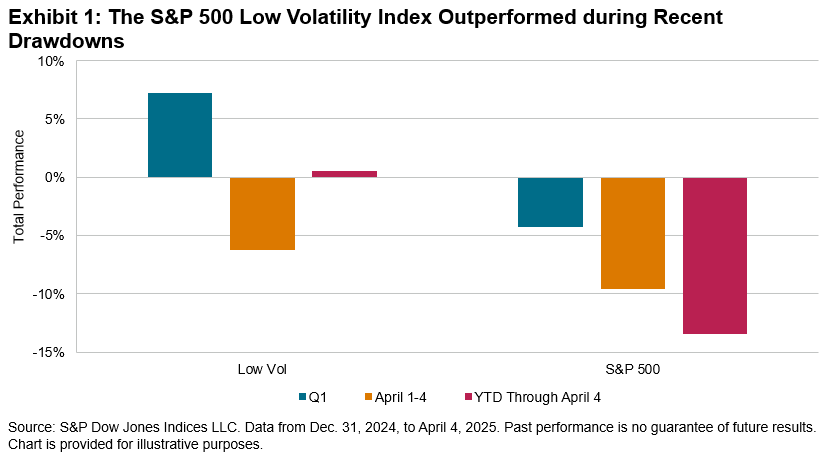

During this turbulent period, the S&P 500 Quality Index outperformed the S&P 500 by 3.58% YTD, while exhibiting lower volatility (see Exhibit 1). Such performance highlights the defensive and resilient characteristics of this index.

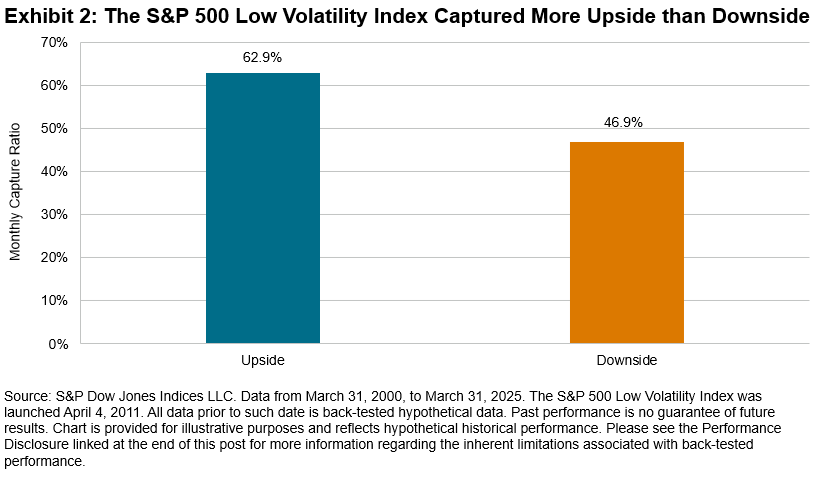

Moreover, this recent outperformance aligns with its historical track record, which indicates that tracking companies with strong fundamentals has been an effective approach for achieving consistent and long-term performance. As shown in Exhibit 2, the S&P 500 Quality Index has outperformed the S&P 500 in terms of total return and risk-adjusted return across almost all periods studied while maintaining consistently lower volatility.

The historical capture ratios show that the S&P 500 Quality Index has typically participated one-for-one in up markets,1 while delivering significant outperformance during down markets. This makes sense, as quality indices tend to track companies with durable business models and sustainable competitive advantages.

Methodology Overview

High quality is typically associated with a company’s strong profitability, high earnings quality and robust financial strength. To effectively reflect these quality characteristics, the S&P Quality Indices utilize three key metrics: return on equity (ROE), balance sheet accruals ratio (BSA) and financial leverage ratio (FLR) (see Exhibit 3).

The selection process for the S&P Quality Indices involves identifying the top 20% of eligible stocks within their respective universes, ranked by overall quality scores. Index constituents are then weighted based on the product of their market capitalization and quality scores, while adhering to specific constraints.3

Performance Attribution

In Exhibit 4, the S&P 500 Quality Index’s YTD performance is broken down into three components: ROE, BSA and FLR attributions.4 ROE contributed the most to the outperformance, followed by BSA.

Performance in Different Macroeconomic Conditions5

Exhibit 5 shows the performance of the S&P 500 Quality Index in different macroeconomic conditions. Historically, the index had comparable performance to the S&P 500 in rising growth regimes while delivering outperformance in slowing growth regimes.

Conclusion

The S&P 500 Quality Index has demonstrated historical resilience and defensive characteristics during times of market volatility and economic uncertainty. By selecting high quality companies with strong profitability, superior earnings quality and robust financial strength, the index not only outperformed the broader S&P 500 but also provided lower volatility in both the short and long term.

1 The market is defined as the monthly performance of the underlying benchmark from Dec. 31, 1994, to March 31, 2025.

2 For more information, see Richardson, Scott Anthony, Sloan, Richard G., Soliman, Mark T. and Tuna, Ayse Irem, “Accrual Reliability, Earnings Persistence and Stock Prices,” Journal of Accounting & Economics, Vol. 39, No. 3, September 2005.

3 For further information about the factor definition, factor score calculation and index design, please see the S&P Quality Indices Methodology.

4 S&P 500 Quality BSA Attribution: Securities in the eligible universe are selected for index inclusion based on their accruals ratio z-score determined during the semiannual rebalancing of the S&P 500 Quality Index. The values for all securities are ranked in ascending order.

S&P 500 Quality Leverage Attribution: Securities in the eligible universe are selected for index inclusion based on their financial leverage ratio z-score determined during the semiannual rebalancing of the S&P 500 Quality Index. The values for all securities are ranked in ascending order.

S&P 500 Quality ROE Attribution: Securities in the eligible universe are selected for index inclusion based on their return-on-equity z-score determined during the semiannual rebalancing of the S&P 500 Quality Index. The values for all securities are ranked in ascending order.

5 Hao, Wenli Bill and Watts, Rupert, “A Historical Perspective on Factor Index Performance across Macroeconomic Cycles,” S&P Dow Jones Indices LLC, Nov. 14, 2024.

The posts on this blog are opinions, not advice. Please read our Disclaimers.