What’s fueling the growing interest in direct indexing? S&P DJI’s Robby Ross and Brandon Hass sit down with Erkko Etula from Brooklyn Investment Group to explore how direct indexing solutions can enable investment managers to customize leading indices like the S&P 500 to meet specific objectives.

The posts on this blog are opinions, not advice. Please read our Disclaimers.Direct Indexing: Launch of MyIndex™ with S&P DJI and Brooklyn Investment Group

Carbon Intensity in the Middle East – An Index Perspective

Comparing the S&P Quality FCF Aristocrats Indices with the S&P Dividend Aristocrats

Introducing the S&P Quality FCF Aristocrats Indices

Evaluating Private Markets with Benchmarks

Direct Indexing: Launch of MyIndex™ with S&P DJI and Brooklyn Investment Group

Carbon Intensity in the Middle East – An Index Perspective

In December 2023, the COP28 UN Climate Change Conference was hosted in Dubai, once again putting the spotlight on global climate change action and handing the Middle East hosting responsibilities. Describing the current period as “the beginning of the end” of the fossil fuel era,1 this iteration of COP not only gave us the first global stocktake of progress against the 1.5°C by 2023 global warming target, but more specifically a unique opportunity to assess how the host region, the Middle East, stacks up in terms of both contribution to global warming and reduction of corporate carbon emissions.

Indices are a useful way to measure the performance of a basket of stocks, but they can also provide insight into the environmental credentials of listed companies. In this blog, we explore the carbon characteristics of the region via the S&P Pan Arab Composite and the S&P/Hawkamah ESG Pan Arab Index. The latter index measures the performance of the 50 top-performing stocks in the region, while incorporating environmental, social and governance (ESG) factors. The former index is a broad, float-adjusted, market-capitalization-weighted index with no specific ESG criteria incorporated, and acts as the benchmark for the ESG index.

Using S&P Global Trucost environmental data, we can assess how constituents of these indices have historically contributed to overall emissions and related metrics. This analysis enables us to explore a number of facets of climate transition. For example, which industries are the heaviest CO2 polluters? Which companies are leading the charge from a decarbonization perspective? How does the inclusion of ESG criteria in index design affect its carbon performance when compared to the benchmark?

Exhibit 1 provides us an overview of how the weighted-average carbon intensity (WACI) of the S&P Pan Arab Composite has increased over time.2 One noteworthy observation here is that corporate disclosure has improved with time, with more companies providing more thorough disclosure of their carbon performance. This is combined with improved modeling techniques on non-disclosing corporates.3

With overall emissions rising, which companies are most heavily contributing? Exhibit 2 provides an overview of which stocks have the greatest WACI, meaning that based on their weight in the index, they have the highest proportional CO2 emissions.

The S&P Pan Arab Composite has more stocks, meaning weights within the index are generally smaller than in the S&P/Hawkamah Pan Arab ESG Index. As a result, although ACWA Power Co has a WACI of 839.8, its smaller index weight minimizes its contribution to the overall WACI of the S&P Pan Arab Composite. Conversely, in the S&P/Hawkamah Pan Arab ESG Index, the lower number of stocks mean that they have greater weight in the index, leading to greater concentration. As a result, the overall index-level WACI of the ESG index has historically been higher.

As depicted in Exhibit 3, due to concentration within the S&P/Hawkamah Pan Arab ESG Index, it had a greater carbon intensity than its benchmark in 2021, 2022 and 2023.

Exhibit 4 depicts the overall country-level contribution of carbon intensity of the S&P Pan Arab Composite. As of June 2024, over one-half of the emissions of the index came from Saudi Arabia, while Kuwait was the second-largest contributor, at 14% of overall index emissions. This is aligned with country representation by market capitalization.

To identify sectors that are making progress, it is possible to compare the sector-level intensity and observe which sectors have seen reductions over time. Exhibit 4 shows the Trucost Revenue Sectors that have made the most progress since December 2019.

Coal Power Generation has experienced the largest reduction in intensity over this period, driven by Taqa Morocco’s declining carbon intensity. However, overall emissions at an index level have increased, highlighting the need for corporate action on CO2 emissions.

This carbon analysis reveals that the S&P/Hawkamah ESG Pan Arab Index exhibited a higher WACI than its benchmark over the five-year period studied. While this finding highlights a notable disconnect between ESG scoring and actual carbon performance, it also emphasizes the evolving nature of ESG indices as they adapt to the complexities of sustainability metrics. While the S&P/Hawkamah ESG Pan Arab Index represents a significant step forward in promoting responsible investment practices in the region, encouraging companies to enhance their ESG performance and transparency, for those market participants seeking an improved carbon reduction at an index level, it may be the case that this should be factored into specific index design principles.

Ultimately, the S&P/Hawkamah ESG Pan Arab Index can serve as a valuable tool for assessing the ESG performance of companies within the region, as it integrates considerations for environmental, social and governance issues. As expectations on corporate sustainability proliferate, the index continues to act as a robust measurement of these crucial topics.

1See a summary of COP28 here: https://unfccc.int/cop28/5-key-takeaways

2For more information on metric calculation please see Index Carbon Metrics Explained.

3The full methodology available at Trucost Environmental Data: Methodology.

The posts on this blog are opinions, not advice. Please read our Disclaimers.Comparing the S&P Quality FCF Aristocrats Indices with the S&P Dividend Aristocrats

- Categories Factors

- Tags aristocrats, defensive strategies, Dividend Aristocrats, dividends, free cash flow, institutional investor, quality, Quality FCF Aristocrats, S&P 500 Quality FCF Aristocrats Index, S&P Developed Quality FCF Aristocrats Index, S&P High Yield Dividend Aristocrats Index, S&P HYDA Index, S&P Quality FCF Aristocrats Indices

While the S&P Dividend Aristocrats® Indices have been in existence for almost two decades, only now has the “Aristocrats” moniker been extended to a new series: the S&P Quality FCF Aristocrats® (Free Cash Flow Aristocrats) Indices. Like the S&P Dividend Aristocrats, this new series emphasizes consistency and the selection of high quality companies. While they share many core attributes, these two series offer differentiated exposure and track companies with distinct profiles. In this blog, we will compare these two series and explore how they can serve as complementary building blocks when paired together.

Methodology Comparison

For the purposes of this blog, we will compare the S&P High Yield Dividend Aristocrats Index (S&P HYDA Index) with the S&P 500® Quality FCF Aristocrats Index, as both are based on a U.S. universe. The S&P HYDA Index is a dividend-focused strategy that tracks high-yielding large-, mid- and small-cap companies in the S&P Composite 1500® that have increased their U.S. dollar dividends for a minimum of 20 consecutive years. Comparatively, the S&P 500 Quality FCF Aristocrats Index is a free cash flow-focused strategy that tracks large-cap companies with a minimum of 10 consecutive years of positive free cash flow, along with high FCF margin and FCF return on invested capital (ROIC).

Index Characteristics

While both index series emphasize consistency as a key qualifier, they differ in their exposures and the types of constituents they track. The S&P HYDA Index aims to select high quality dividend payers, tilting to both value and quality. In contrast, the S&P 500 Quality FCF Aristocrats Index focuses on companies with high and consistent free cash flow, resulting in a purer focus on quality, as free cash flow measures true profitability and is less susceptible to manipulation, with a tilt to growth. This distinction reflects the company lifecycle: S&P HYDA Index companies are typically more mature, blue-chip firms, while the S&P 500 Quality FCF Aristocrats Index often comprises earlier-stage companies that tend to reinvest their capital at high rates of return to seize growth opportunities.

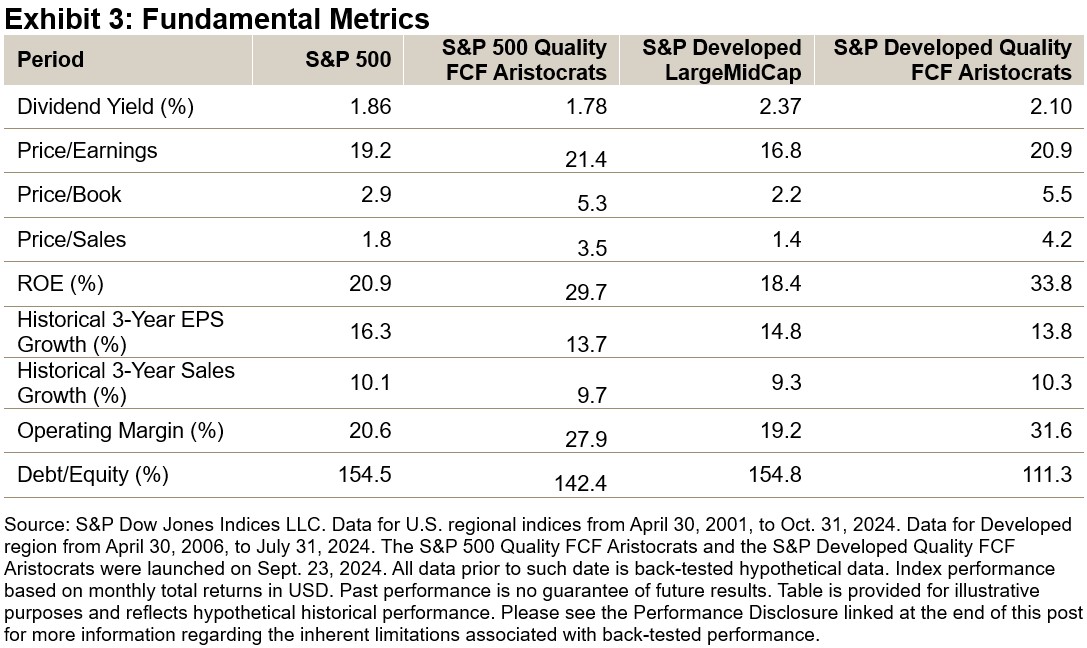

From a fundamental perspective, Exhibit 3 shows that the S&P HYDA Index tends to track companies with lower valuation multiples and higher yields. In contrast, the S&P 500 Quality FCF Aristocrats Index typically exhibits higher profitability, stronger sales and earnings growth, as well as elevated returns on equity.

Performance Comparison

Both indices comfortably outperformed their respective benchmarks over the back-tested period since 2001 (see Exhibit 3), making a side-by-side comparison insightful. Notably, the S&P HYDA Index exhibited a lower upside capture ratio (0.85) but demonstrated strong defensiveness on the downside (0.76). The S&P 500 Quality FCF Aristocrats Index closely tracked the benchmark in up markets and showed moderate defensiveness on the downside, though not as robustly as the S&P HYDA Index.

Sector Comparison

From a sector perspective, these indices could be considered complementary due to their contrasting sector overweights and underweights. The S&P HYDA Index generally favors defensive sectors such as Consumer Staples and Utilities, while the S&P 500 Quality FCF Aristocrats Index has a greater weight in secular growth sectors, including Information Technology and Health Care.

Pairing the S&P HYDA Index with the S&P Quality FCF Aristocrats Index

When choosing between these two indices, market participants should align their selection with their desired outcome. The S&P HYDA Index has historically tended to have equity participation with the potential for higher dividends and strong defensive qualities. The S&P 500 Quality FCF Aristocrats Index has demonstrated market-like upside capture ratios with enhanced quality, reduced downside risk and strong risk-adjusted returns. Alternatively, combining both indices may offer the best of both worlds, historically improving overall risk-adjusted returns and smoothing the impact of regime changes.

This new series of indices, while using the Aristocrats brand, has shown differentiated exposure versus the S&P Dividend Aristocrats. Compared with the S&P HYDA Index, the S&P 500 FCF Aristocrats Index has had low constituent overlap, higher weight in secular growth sectors and a pure focus on quality. We hope this blog has clarified the positioning of these two index series, demonstrating their potential as complementary tools.

The posts on this blog are opinions, not advice. Please read our Disclaimers.Introducing the S&P Quality FCF Aristocrats Indices

The S&P Quality FCF Aristocrats® (Free Cash Flow Aristocrats) Indices measure companies that consistently generate robust FCF over many years. FCF, the cash remaining after a business covers its operational costs and capital investments, is crucial because it provides financial flexibility. Companies with high FCF can invest in growth opportunities, pay dividends and reduce debt, making them more resilient in fluctuating markets.

On Sept. 23, 2024, S&P Dow Jones Indices (S&P DJI) launched two indices in this new series: the S&P 500® Quality FCF Aristocrats Index and S&P Developed Quality FCF Aristocrats Index. In this blog, we will introduce these indices by reviewing their methodology and historical performance.

Methodology Overview

These indices track companies that have a minimum of 10 consecutive years of positive FCF, along with a high FCF margin and FCF return on invested capital (ROIC). FCF margin measures how efficiently revenue is converted into FCF, while FCF ROIC measures how efficiently invested capital is utilized to generate FCF.

By concentrating on firms that excel in long-term FCF generation, this methodology aims to include only the highest-quality companies. Additionally, by prioritizing consistent and efficient FCF generation, this approach distinguishes itself from other FCF-based indices in the market, which tend to be yield-focused and exhibit a strong value tilt.

Performance Insights

When looking at back-tested historical performance, these indices outperformed their regional benchmarks, delivering higher risk-adjusted returns and lower losses during market downturns. They provided a defensive investment strategy that balanced growth potential with stability, visible through their reduced volatility and lower downside capture ratios.

Factor Tilts in S&P Quality FCF Aristocrats Indices

The S&P Quality FCF Aristocrats Indices primarily emphasize quality, including companies that typically exhibit high and consistent FCF generation. Additionally, these indices tilt toward growth since these companies can allocate excess FCF to research & development, advertising and marketing.

As Exhibit 3 shows, this approach has historically resulted in improved return on equity (ROE) and operating margins compared to their benchmark indices, showcasing a balanced strategy that prioritizes both quality and growth.

The regional S&P Quality FCF Aristocrats Indices offer a high quality, defensive approach, demonstrating outperformance versus their benchmarks with higher risk-adjusted returns and lower downside capture in falling markets, while matching the benchmark returns in rising markets over the back-tested period. Stay tuned for an upcoming blog, where we will compare the S&P Quality FCF Aristocrats Indices with the S&P Dividend Aristocrats® Indices.

The posts on this blog are opinions, not advice. Please read our Disclaimers.Evaluating Private Markets with Benchmarks

Collectively, private markets make up one of the fastest-growing market segments, but they have historically been characterized by opacity and inaccessibility. This is changing, thanks in part to evolving private market benchmarks that focus on strategy-specific performance. In our first blog, we summarized the performance of a collection of private market benchmarks.

In this blog, we explore the important role Cambridge Associates benchmarks may play moving forward and highlight how the right data can bolster private market benchmarks.

Benchmarking Private Markets

For 50 years, Cambridge Associates has provided performance evaluation tools and detailed insights for investors navigating the complex landscape of private investments. Today, its platform tracks over 10,000 private investment funds and the firm remains a critical proponent and advisor in the private market landscape. Cambridge Associates benchmarks deliver robust and data-driven insights derived from deep expertise and engagement with private market participants to help investors identify opportunities, manage risks and drive portfolio performance.

S&P Dow Jones Indices supports clients, in collaboration with Cambridge Associates, by providing private market solutions for investors with dynamic, fit-for-purpose benchmarks in an ever-changing market.

Data Sourcing Is Key

Accurate benchmarking for private investments requires a diligent process and access to a “golden source” of performance data. In private markets, that golden source is fund financial statements. Cambridge Associates sources its data directly from private investment fund managers who contribute anonymously across strategies and geographies. Contributing managers are screened to ensure the data is of institutional quality.

The result is a private investment benchmarking universe that is both broad and granular, reflecting the diverse opportunity set in private markets. Benchmarks are organized into four main strategies: Private Equity, Venture Capital, Private Credit and Real Assets, plus aggregated benchmarks that blend Private Equity and Venture Capital.

Sub-strategies include Buyouts, Growth Equity, Subordinated Capital, Distressed Debt, Infrastructure, Real Estate, Secondaries and Fund of Funds, and can be broken down further by geography, size or sector.

Benchmarking in 3D

Because of private markets’ unique performance drivers, Cambridge Associates advocates using multiple metrics to evaluate them. While internal rate of return (IRR) is the predominant measure of performance of private investments, Cambridge Associates encourages investors and managers to evaluate IRRs in conjunction with multiples, performance breakpoints, vintage year returns and public market equivalents for a wider lens of performance evaluation.

For example, an investor evaluating a manager may use quartile breakpoints to rank their investments in terms of IRR and multiples against a sample of the strategy funds from the same vintage year. Or they may wish to use a public market equivalent (PME) analysis, which essentially addresses the question: what would my return look like if I invested capital in a given public market (e.g., the S&P 500) with the exact timing of private market cash flows?

Key Takeaways and the Path Ahead

As the private markets industry evolves, several trends are taking shape:

- Continued expansion of assets under management in private markets underscores the need for sophisticated and comprehensive benchmarking tools.

- Enhanced transparency through more sophisticated benchmarks, data and tools could be crucial for investors seeking to navigate these complex markets.

- Growing demand from individual investors who have increasing access to private market strategies.

The role of Cambridge Associates benchmarks could become increasingly critical, with more investors seeking custom benchmark solutions to support performance measurement, fund manager selection or fund due diligence. As we progress, the insights derived from Cambridge Associates benchmarks will help navigate the dynamic and complex private market environment, assisting investors to be well equipped to handle emerging opportunities.

Learn more in our recent analysis, “2023 Private Markets Review: Cambridge Associates Benchmarks versus Public Indices.”

Learn more about Private Investment Benchmarks

This blog was co-authored by Ricky LaBelle, Nicholas Godec, and Greg Vadala.

The posts on this blog are opinions, not advice. Please read our Disclaimers.