While the S&P Dividend Aristocrats® Indices have been in existence for almost two decades, only now has the “Aristocrats” moniker been extended to a new series: the S&P Quality FCF Aristocrats® (Free Cash Flow Aristocrats) Indices. Like the S&P Dividend Aristocrats, this new series emphasizes consistency and the selection of high quality companies. While they share many core attributes, these two series offer differentiated exposure and track companies with distinct profiles. In this blog, we will compare these two series and explore how they can serve as complementary building blocks when paired together.

Methodology Comparison

For the purposes of this blog, we will compare the S&P High Yield Dividend Aristocrats Index (S&P HYDA Index) with the S&P 500® Quality FCF Aristocrats Index, as both are based on a U.S. universe. The S&P HYDA Index is a dividend-focused strategy that tracks high-yielding large-, mid- and small-cap companies in the S&P Composite 1500® that have increased their U.S. dollar dividends for a minimum of 20 consecutive years. Comparatively, the S&P 500 Quality FCF Aristocrats Index is a free cash flow-focused strategy that tracks large-cap companies with a minimum of 10 consecutive years of positive free cash flow, along with high FCF margin and FCF return on invested capital (ROIC).

Index Characteristics

While both index series emphasize consistency as a key qualifier, they differ in their exposures and the types of constituents they track. The S&P HYDA Index aims to select high quality dividend payers, tilting to both value and quality. In contrast, the S&P 500 Quality FCF Aristocrats Index focuses on companies with high and consistent free cash flow, resulting in a purer focus on quality, as free cash flow measures true profitability and is less susceptible to manipulation, with a tilt to growth. This distinction reflects the company lifecycle: S&P HYDA Index companies are typically more mature, blue-chip firms, while the S&P 500 Quality FCF Aristocrats Index often comprises earlier-stage companies that tend to reinvest their capital at high rates of return to seize growth opportunities.

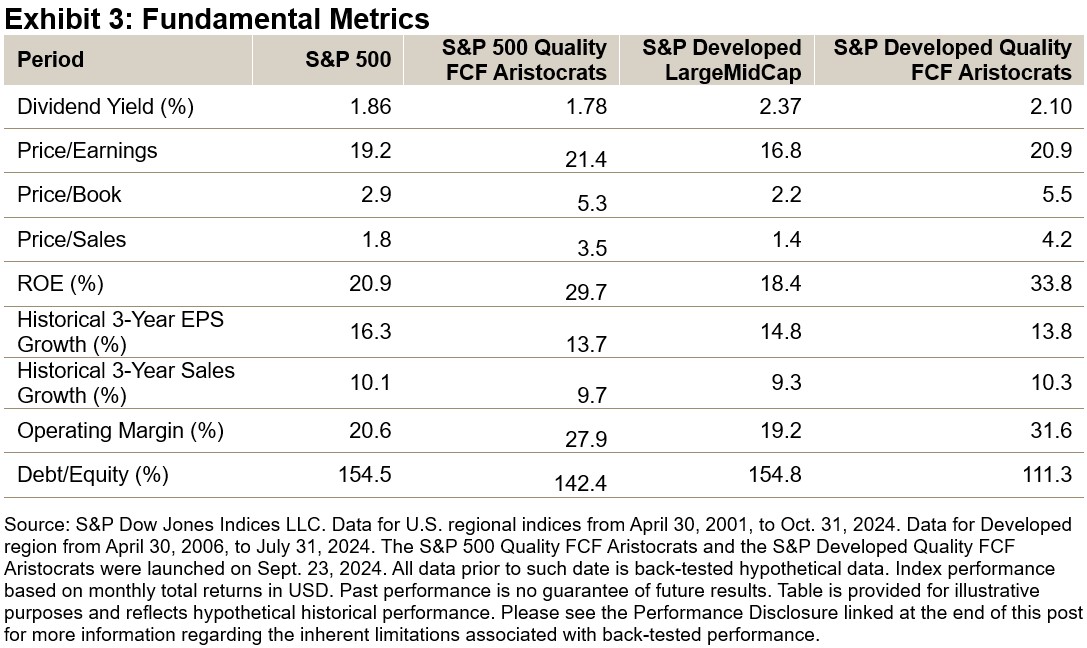

From a fundamental perspective, Exhibit 3 shows that the S&P HYDA Index tends to track companies with lower valuation multiples and higher yields. In contrast, the S&P 500 Quality FCF Aristocrats Index typically exhibits higher profitability, stronger sales and earnings growth, as well as elevated returns on equity.

Performance Comparison

Both indices comfortably outperformed their respective benchmarks over the back-tested period since 2001 (see Exhibit 3), making a side-by-side comparison insightful. Notably, the S&P HYDA Index exhibited a lower upside capture ratio (0.85) but demonstrated strong defensiveness on the downside (0.76). The S&P 500 Quality FCF Aristocrats Index closely tracked the benchmark in up markets and showed moderate defensiveness on the downside, though not as robustly as the S&P HYDA Index.

Sector Comparison

From a sector perspective, these indices could be considered complementary due to their contrasting sector overweights and underweights. The S&P HYDA Index generally favors defensive sectors such as Consumer Staples and Utilities, while the S&P 500 Quality FCF Aristocrats Index has a greater weight in secular growth sectors, including Information Technology and Health Care.

Pairing the S&P HYDA Index with the S&P Quality FCF Aristocrats Index

When choosing between these two indices, market participants should align their selection with their desired outcome. The S&P HYDA Index has historically tended to have equity participation with the potential for higher dividends and strong defensive qualities. The S&P 500 Quality FCF Aristocrats Index has demonstrated market-like upside capture ratios with enhanced quality, reduced downside risk and strong risk-adjusted returns. Alternatively, combining both indices may offer the best of both worlds, historically improving overall risk-adjusted returns and smoothing the impact of regime changes.

This new series of indices, while using the Aristocrats brand, has shown differentiated exposure versus the S&P Dividend Aristocrats. Compared with the S&P HYDA Index, the S&P 500 FCF Aristocrats Index has had low constituent overlap, higher weight in secular growth sectors and a pure focus on quality. We hope this blog has clarified the positioning of these two index series, demonstrating their potential as complementary tools.

The posts on this blog are opinions, not advice. Please read our Disclaimers.