The ETF industry has hit a major milestone, reaching USD $10 trillion in assets under management in the U.S. Commentary on the rise of index-based or passive investing may be widespread, but it is harder to find estimates of how truly “passive” their holders are. Secondary market volumes offer a fascinating, important and complementary perspective.

Our new paper “The Liquidity Landscape: Trading Linked to S&P DJI Indices,” shows that volumes associated with listed products tracking S&P DJI’s indices dramatically exceed the corresponding USD 6.6 trillion level of listed index-linked assets,1 with volumes almost doubling from four years ago to exceed USD 246 trillion in 2023.2 Index-based products are increasingly among the most traded securities, with ETFs representing 42% of the most-traded U.S.-listed equity securities by U.S. dollar volumes as of 2023.

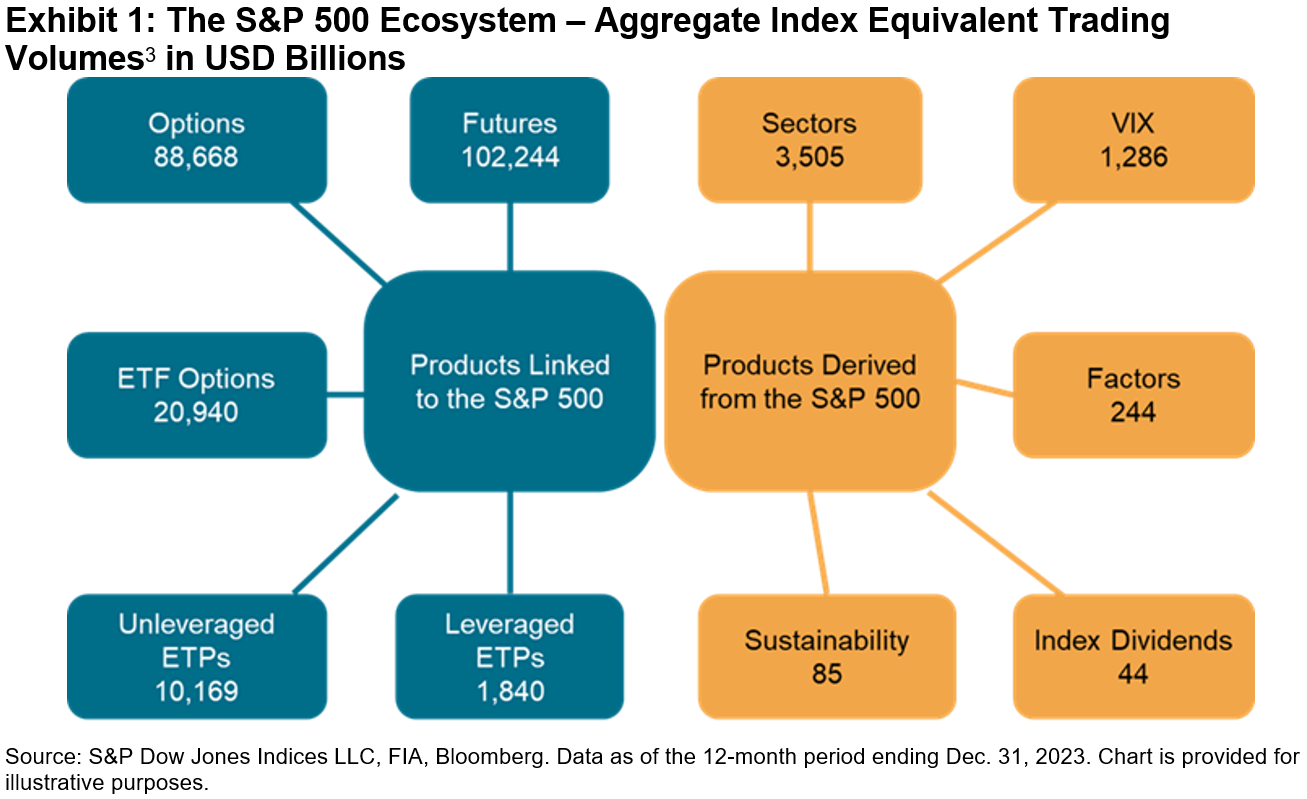

The S&P 500® was the primary contributor to the volumes cited above and was associated with the largest number of distinct products. Volumes associated with the S&P 500 totaled approximately USD 224 trillion, the bulk of which was contributed by options and futures, as we observe from the left side of Exhibit 1. The right side of the exhibit shows volumes in indices derived from the S&P 500 such as our suite of sector or factor indices.

The S&P 500 ecosystem stands out because of its liquidity globally. The network of products tied to the S&P 500 or indices derived from it can form an interconnected web of pricing and trading activity through arbitrage mechanics or risk transference. For example, market makers in S&P 500-linked ETFs, which are listed in markets ranging from New Zealand to Brazil, might use futures to hedge their inventory positions. Or a holder of S&P 500 sector ETFs can weight them accordingly to replicate exposure to the benchmark. This same holder could use options to manage their downside risk or generate income from call overwriting. The resulting benefits in transparency and pricing efficiency stemming from these connections demonstrate the potential network effects of liquidity.

To better understand the behavior of such users of index-linked products, we can divide assets by volumes to arrive at an estimate of the average holding period among market participants.4 For example, for a fund with assets of USD 100 million, an aggregate annual trading volume of USD 200 million would imply an average holding period of six months. Exhibit 2 shows the distribution of assets across the S&P DJI universe by their respective trading frequencies: products with an average holding period of more than one year, one month to one year, one week to one month, and those with an average holding period of less than one week.

Exhibit 2 illustrates several notable observations. First, approximately 60% of assets were associated with products with an average holding period of less than one month, confirming the presence of some relatively active users. Second, options and futures along with leveraged ETPs tended to have shorter average holding periods, indicating heavier usage of these product types among shorter-frequency investors. Finally, while ETPs tended to have longer holding periods, only roughly 20% of ETP assets were associated with products with an average holding period of more than one year. The holders of index funds should not always be equated with “passive” investors.

The S&P DJI ecosystem has benefited from the network effects of liquidity offered by market participants operating on a wide range of trading frequencies, resulting in a creative cacophony of perspectives. This may provide long-term investors with greater confidence in the prices they experience, while more active traders may benefit from increased liquidity. Find out more about how our robust trading ecosystems are promoting price transparency, market efficiency and confidence all around the world in “The Liquidity Landscape: Trading Linked to S&P DJI Indices.”

1 See S&P Dow Jones Indices Annual Survey of Assets, Dec. 31, 2023.

2 See “A Window on Index Liquidity: Volumes Linked to S&P DJI Indices,” S&P Dow Jones Indices, Aug. 29, 2019.

3 Index equivalent trading volume (IET) reflects the economic exposure to the index that is being transacted at the time a trade occurs; it is determined by the instrument’s short-term responsiveness to movements in the underlying index. See Appendix of “The Liquidity Landscape: Trading Linked to S&P DJI Indices”, S&P Dow Jones Indices, Sept. 16, 2024.

4 We caution that any security can have a mix of investors who trade with different frequencies.

The posts on this blog are opinions, not advice. Please read our Disclaimers.