Launched in the late 1990s, the Select Sector® indices measure the performance of S&P 500® sectors; each S&P 500 company is assigned to one of the 11 Select Sector indices, based on the Global Industry Classification Standard (GICS®) framework. The indices serve as the basis for an ecosystem of financial products, which in turn allow market participants to express views.

S&P Dow Jones Indices (S&P DJI) recently announced changes to the Select Sector index methodology, which will go into effect prior to the open on Sept. 23, 2024. Here’s an overview of the upcoming changes to the quarterly rebalance process.

The Select Sector indices are capped market capitalization weighted.

A key feature of the Select Sector indices is that they employ a capping mechanism to ensure diversification among the companies within each index. The capping thresholds are intended to reflect certain diversification requirements imposed on regulated investment companies under the U.S. Internal Revenue Code and the Investment Company Act of 1940.1

At each quarterly rebalance, companies are initially weighted by float market capitalization (FMC). Modifications are made to these FMC weights if a) any company has a weight greater than 24%, or b) the sum of the companies with weights greater than 4.8% exceeds 50% of the total index weight. These rebalance thresholds are unchanged by the upcoming methodology changes that take effect on Sept. 23, 2024.

The quarterly capping process is changing.

If companies with FMC weights greater than 4.8%—“larger companies”—account for more than 50% of the index weight, the current capping mechanism reduces the weight of the smallest company in the group to 4.5%. The process is repeated iteratively, if necessary, until there are no breaches to the thresholds. Full details of the capping mechanism as of the publication date (the “Legacy Capping Mechanism”) can be found in the S&P U.S. Indices Methodology.

The new approach (the “New Capping Mechanism”) would handle such a breach differently: the aggregate weight of the larger companies will be reduced to 45% and the larger companies’ individual weights will be determined by their relative proportions, after checking for any breaches in the single company cap. The minimum index weight of each of the larger companies will be 4.5%. The recent announcement provides the full details.

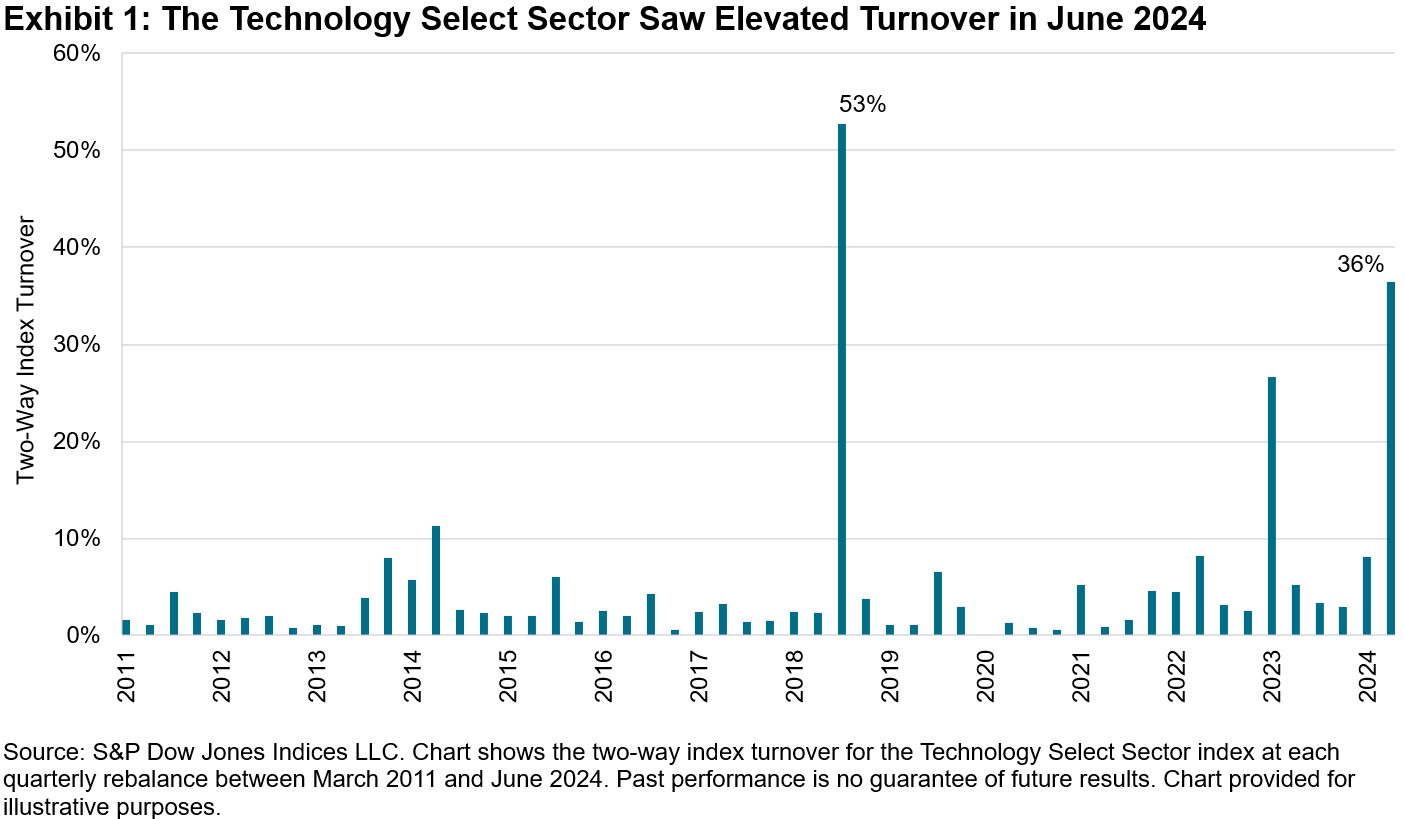

Market dynamics have impacted Select Sector index composition in 2024.

The rationale for the change to the capping mechanism is that the impact of market dynamics could result in the Legacy Capping Mechanism causing “flip flops” in index weights. This was particularly evident in the Technology Select Sector index in 2024. For example, Microsoft, Apple and Nvidia each had FMC weights greater than 4.8% and their collective FMC weight exceeded 50% at the March 2024 reference date. As the smallest of the three companies at the time, Nvidia’s weight was reduced to 4.5%.2

A similar situation occurred in June 2024, except Nvidia had become the second largest of the group, reflecting investors’ expectations of the impact of AI on the company’s growth prospects. Accounting for changes between the rebalance reference date and rebalance effective date, Apple—as the smallest of the group—had its index weight reduced by 17% at the June rebalance, while Nvidia’s weight increased by 15% to around 21%. These changes meant that the index’s quarterly rebalance turnover in June was the highest since September 2018, when various companies moved to Communications Services as part of a GICS structure update.

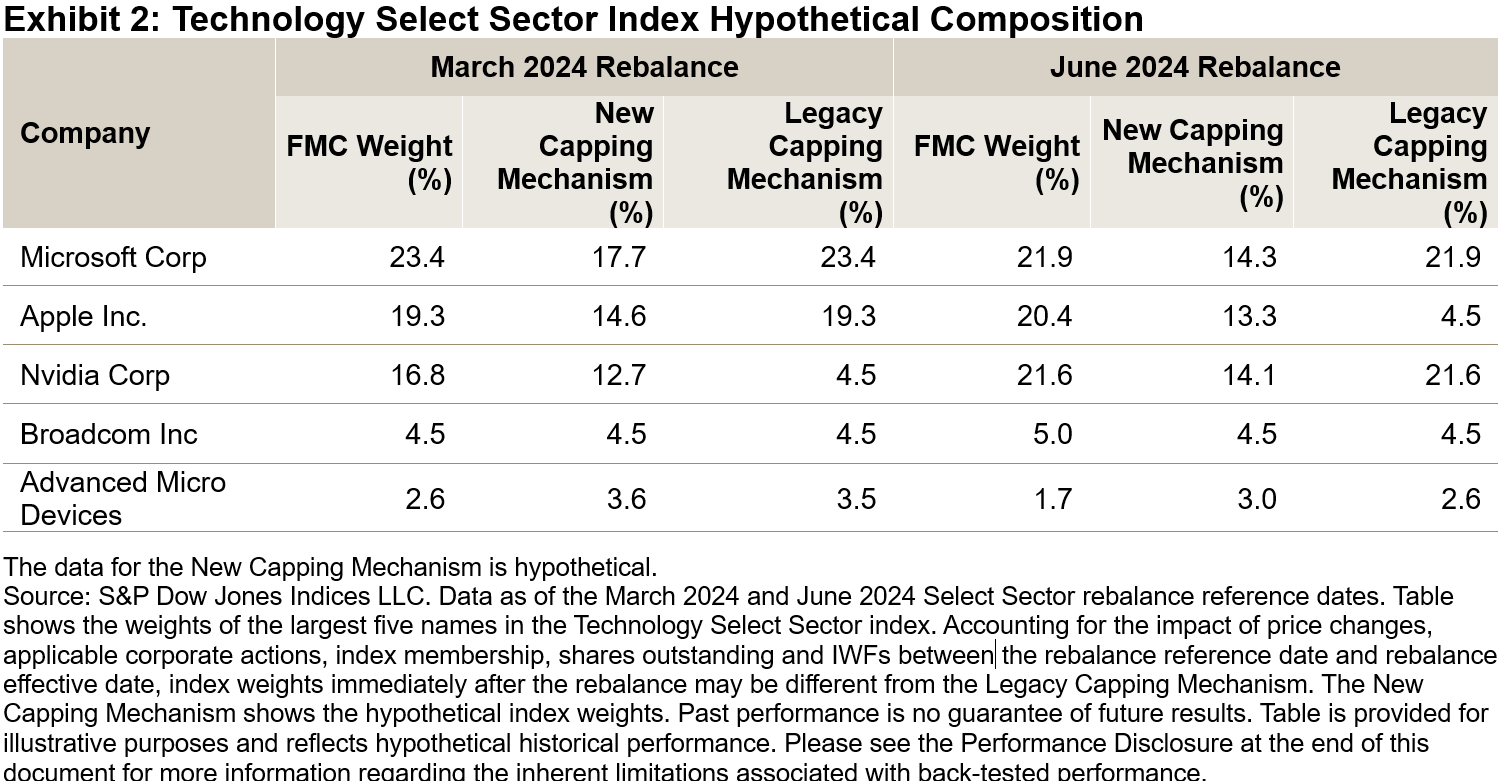

The New Capping Mechanism better retains FMC proportions.

The New Capping Mechanism is designed to better retain FMC proportions among index constituents, while still being mindful of diversification thresholds. For example, Exhibit 2—taken from the impact analysis that was included in the public consultation—shows the hypothetical weights of several companies in the Technology Select Sector index under the New Capping Mechanism versus the Legacy Capping Mechanism as of the March and June 2024 rebalance reference dates. The application of the new approach would have reduced the potential for “flip flops” in index composition.

Although we will have to wait to see the exact composition of the Select Sector indices after the September rebalance, upcoming changes reflected in the New Capping Mechanism provide an example of how index methodologies can evolve in light of market dynamics.

1 For more information on the capping thresholds, please refer to the Regulatory Capping Requirements section of S&P Dow Jones Indices’ Equity Indices Policies & Practices Methodology.

2 Accounting for the impact of price changes, applicable corporate actions, index membership, shares outstanding and IWFs between the rebalance reference date and rebalance effective date, Nvidia’s index weight prior to the open on March 18, 2024, was 4.55%.

The posts on this blog are opinions, not advice. Please read our Disclaimers.