The growth of index-based passive investing can be attributed to its transparency, efficiency and low cost, along with active management shortcomings. More recently, buoyed by the growth of direct indexing, there has also been increased demand for indices that select a subset of constituents from underlying benchmarks and are designed to meet specified objectives.

S&P DJI recently launched the S&P Focused Indices, which are designed with direct indexing use cases in mind.

S&P Focused Indices Methodology Overview

The S&P Focused Index Series currently comprises three indices: S&P 500® Focused 50 Index, S&P 500 Focused 100 Index and S&P 500 Catholic Values Focused 100 Index. The first two are based on the S&P 500, and the third index is based on the S&P 500 Catholic Values Index. The target company counts are 50, 100 and 100, respectively, and the indices are reconstituted annually.

Each S&P Focused Index is designed to have similar Global Industry Classification Standard (GICS®) industry group weights as its underlying index, which has also resulted in similar sector weights historically.

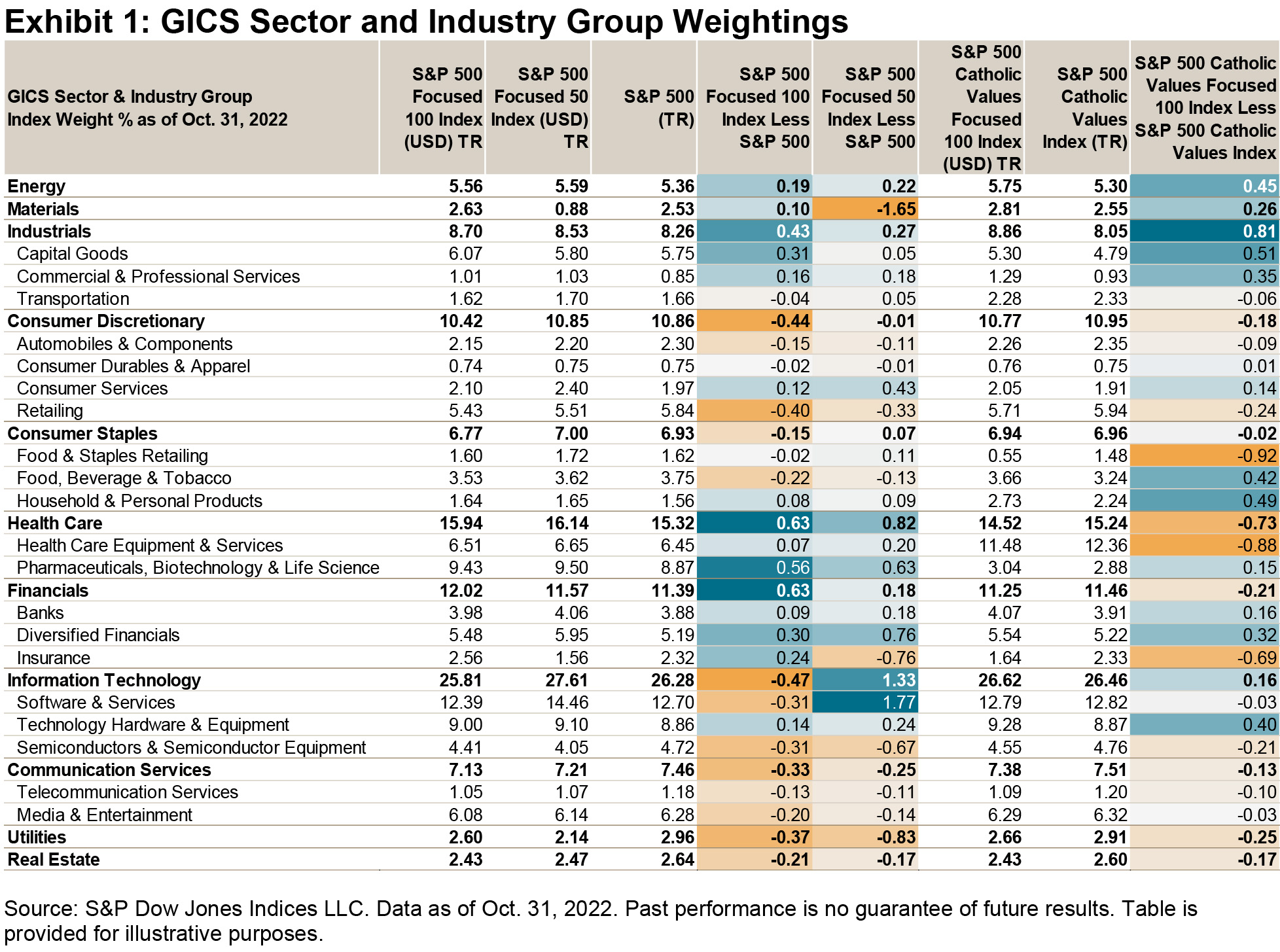

Exhibit 1 compares the GICS sector and industry group weights of each S&P Focused Index against its benchmark, as of Oct. 31, 2022. The results were similar to their benchmarks; differences were typically less than 1%.

Back-Tested Performance History

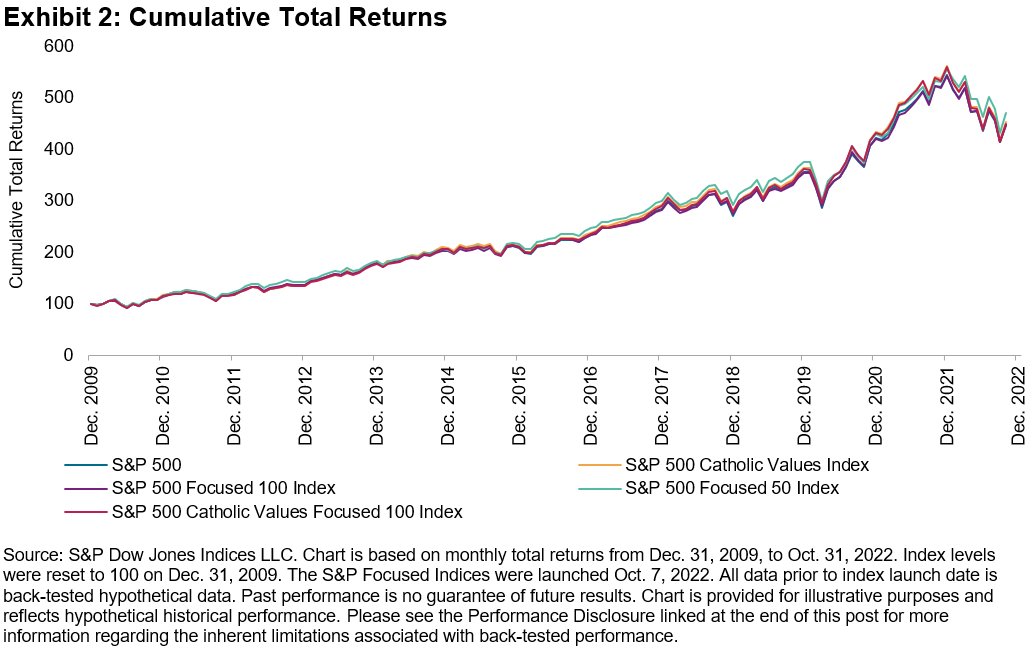

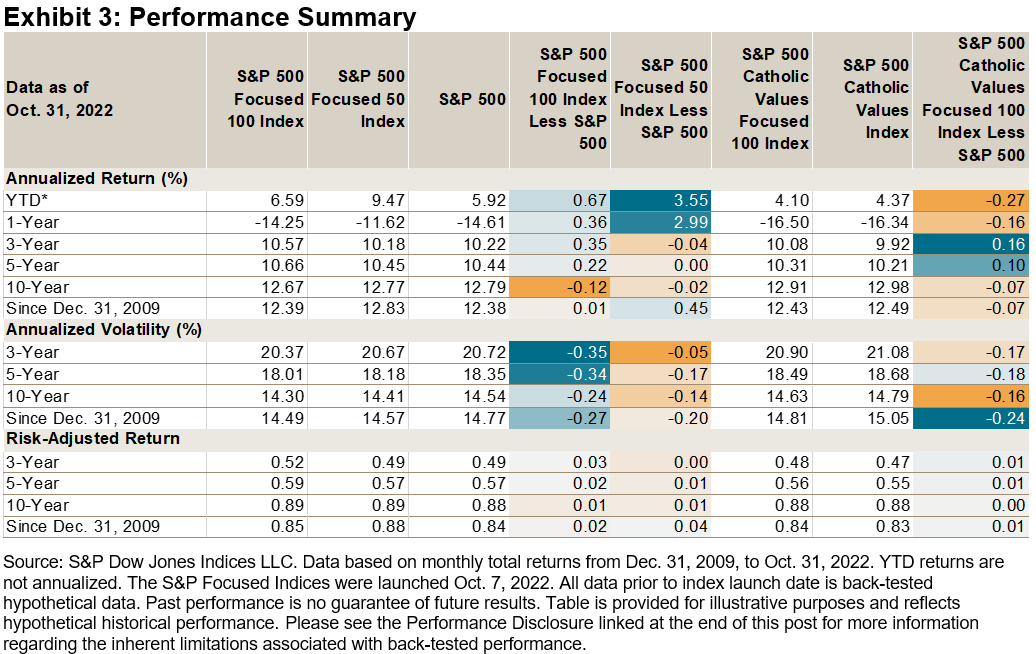

Perhaps unsurprisingly, the similarity in sector and industry group weights between the S&P Focused Indices and their respective underlying indices contributed to similar long-term performance, historically. For example, only 0.03% separated the annualized returns of the S&P 500 Focused 50 Index and S&P 500 since December 2009.

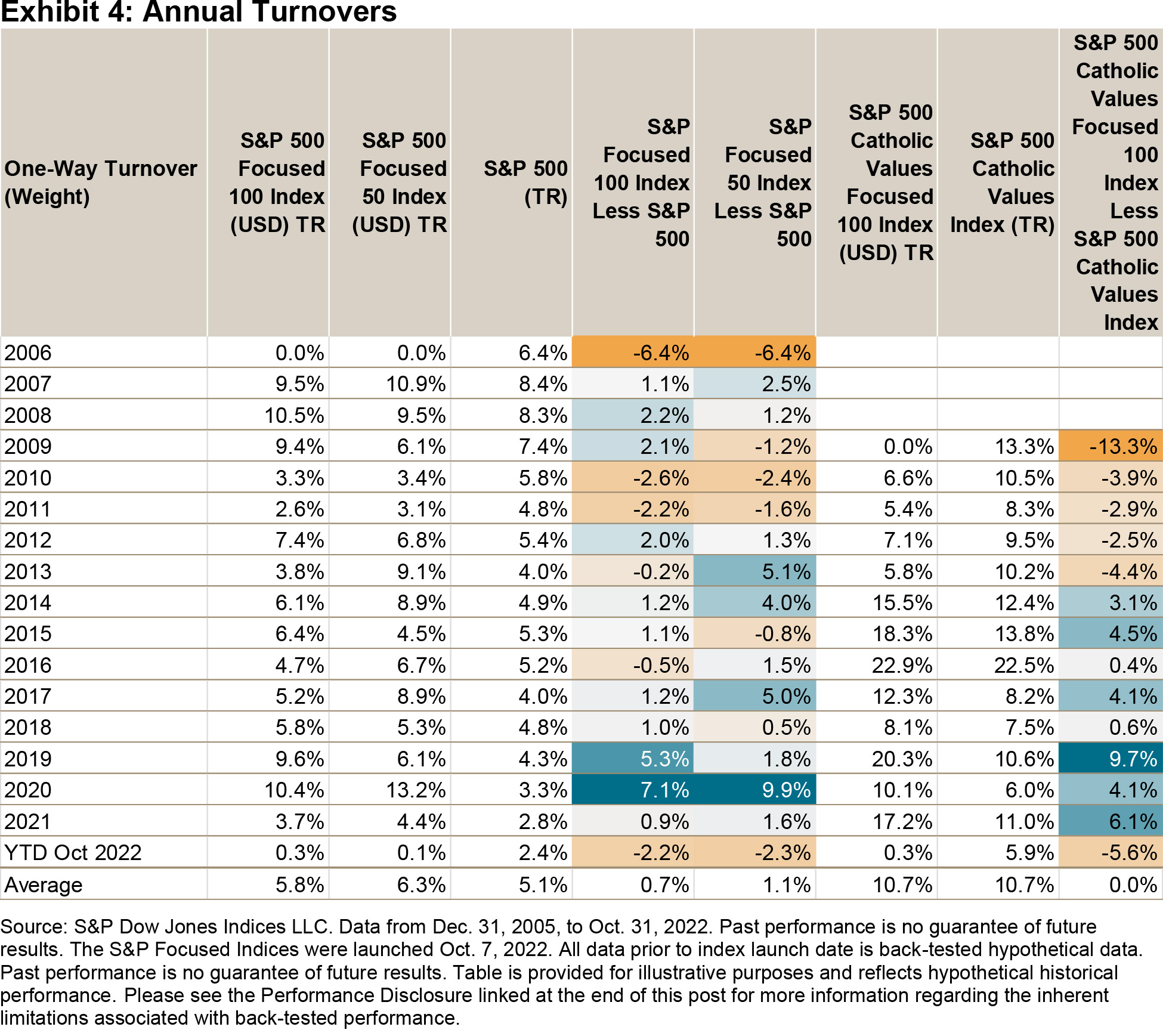

However, greater deviations were observed over shorter horizons. For instance, the S&P 500 Focused 50 Index outperformed the S&P 500 by 2.36% YTD and by 2.99% over the past 12 months. Exhibit 4 shows that the S&P Focused Indices’ construction provided similar turnover figures as their benchmarks, historically.

Exhibit 4 shows that the S&P Focused Indices’ construction provided similar turnover figures as their benchmarks, historically.

As a result, the S&P Focused Indices’ construction may be relevant for direct indexing managers looking to achieve similar sector and industry group weights as their respective underlying indices, but with fewer names.

The posts on this blog are opinions, not advice. Please read our Disclaimers.