When does low volatility tend to outperform and why? S&P DJI’s Craig Lazzara and Invesco’s Nick Kalivas take a closer look at low vol performance in periods of rising rates and inflation, and explore what happens to risk/return when low vol is combined with other factors.

https://youtu.be/UJWi3P7-e5I

The posts on this blog are opinions, not advice. Please read our Disclaimers.

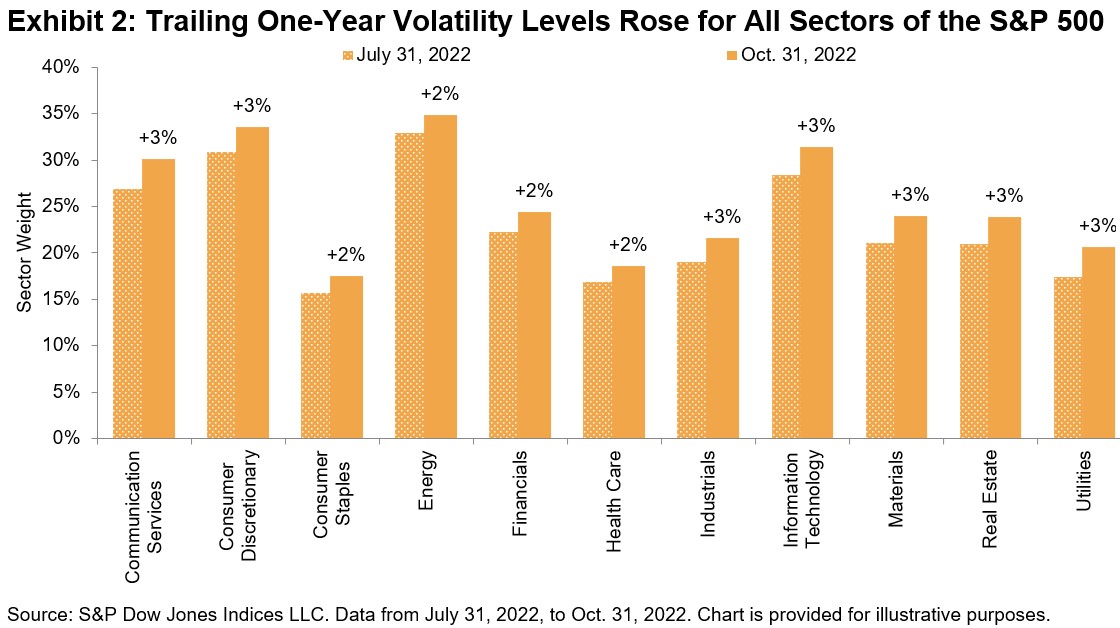

Since August, volatility has risen for all S&P 500 sectors, with Consumer Discretionary and Energy maintaining their status as the most volatile sectors.

Since August, volatility has risen for all S&P 500 sectors, with Consumer Discretionary and Energy maintaining their status as the most volatile sectors.

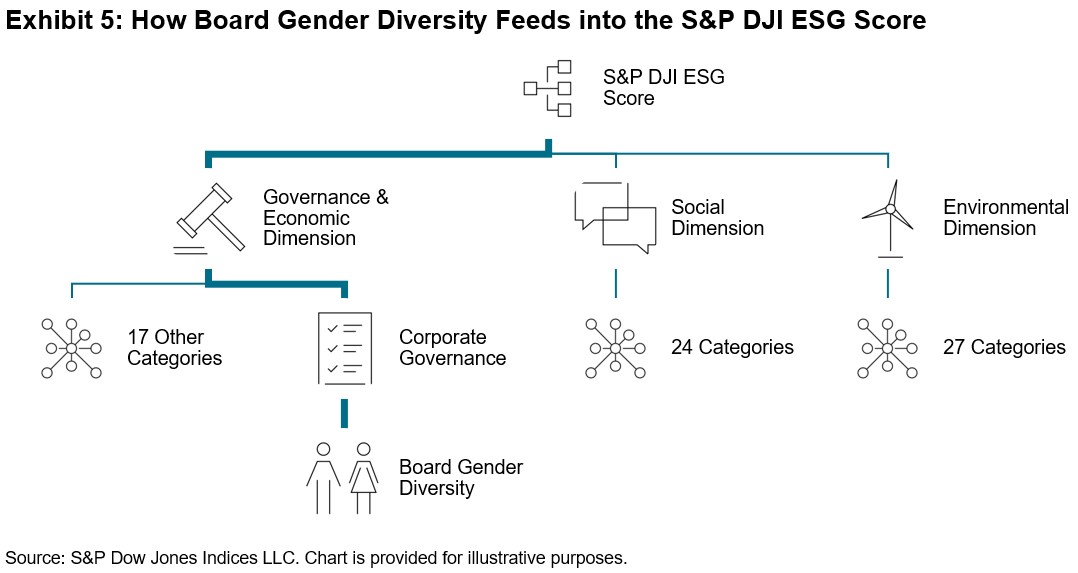

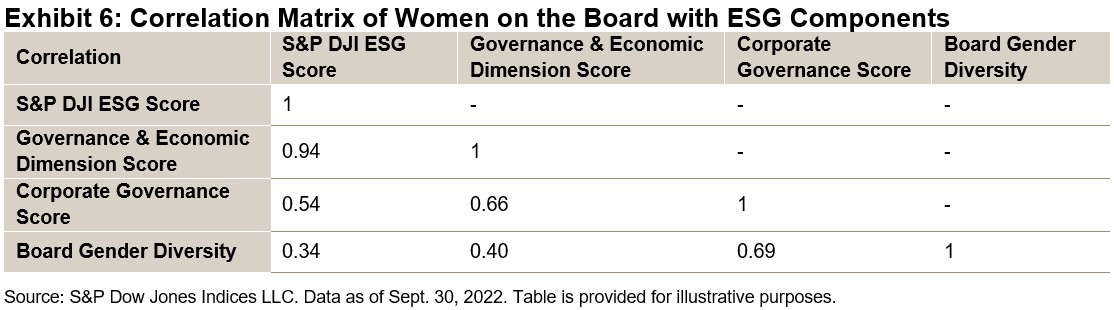

Exhibit 6 demonstrates the influence that women on boards of directors can have on each dimension of a firm’s S&P DJI ESG Score. Even at the overall ESG score level, board gender diversity still plays a part in a company’s overall sustainability rating.

Exhibit 6 demonstrates the influence that women on boards of directors can have on each dimension of a firm’s S&P DJI ESG Score. Even at the overall ESG score level, board gender diversity still plays a part in a company’s overall sustainability rating.