Try as one might, it is hard not to notice the woes of equities this year. Through May 19, 2022, the S&P 500® has declined 18%, losing 9% in the last three months alone. This pain was felt across most sectors of the index, with only Consumer Staples, Energy, and Utilities in positive territory for the year. Exhibit 1 shows that volatility increased in every sector except Energy in the last three months.

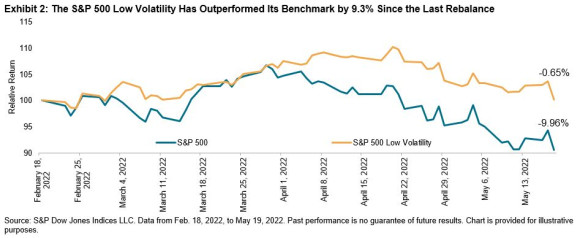

Despite the general increase in volatility, there were clearly pockets of stability in the market, as the S&P 500 Low Volatility Index is actually flat since its last rebalance on Feb 18, 2022, down 0.7%. Exhibit 2 contrasts the performance of low volatility index with that of the S&P 500, which declined 10.0% in the same period. The low volatility index is designed to mute the gyrations of the market in both directions (which it has historically done with reasonable reliability). It should go down less when the market is down, but also go up less when the market is up. And it has certainly done what it is designed to do in the current market rout.

Effective after the market close May 20, 2022, the S&P 500 Low Volatility Index will have almost half its weight in just two sectors, Utilities (26%) and Consumer Staples (22%). As shown in Exhibit 3, the latest rebalance saw a significant increase in Utilities, Financials and Real Estate, and reductions in exposure to the Consumer Discretionary, Health Care and Technology sectors. Despite its strong performance, Energy still has no presence in the index—not a surprise since it remains the most volatile sector of the S&P 500.