In October 2021, the S&P Global Clean Energy Index implemented most of the items addressed in the August 2021 consultation, which improved transparency, reduced the index’s carbon footprint and better aligned the index methodology with market trends.1 The latest rebalance (effective April 25, 2022), was a continuation of that consultation, with a focus on diversification by adding companies listed in emerging markets.2

The Inclusion of Emerging Market Companies Has Created a ‘Cleaner’ Clean Energy Index

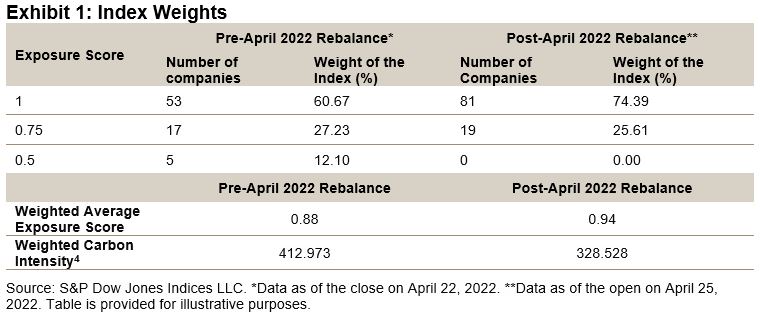

The expansion to include companies listed in emerging markets allows the index to track a larger selection universe. The index is now composed of 100 constituents (formerly 75), thus achieving the target count as outlined in the index methodology. Further, the index purity, as defined by the weighted average exposure score,3 has also improved (see Exhibit 1). The current target stock count is achieved by selecting companies that have either exposure scores of 1 or 0.75, with the majority of companies achieving a score of 1. Previously, the index also included companies with an exposure score of 0.5.

Exhibit 1 shows that close to 75% of the index weight is now composed of companies that have been assigned a maximum clean energy exposure score, a notable improvement compared to the previous composition. Additionally, we observe an improvement in the carbon intensity score.

Emerging Markets Companies Added at “Half” Weight

S&P Dow Jones Indices announced in February 2022 that companies listed in emerging markets will be incorporated in a two-phased approach coinciding with the reconstitutions in April and October 2022. Therefore, all emerging market-listed companies that were added at this April rebalance were added at one-half of their target weights, with the remaining half to be added at the October 2022 rebalance. Of the 33 companies added to the index, 29 were listings from emerging markets, making up 9% of the index weight. The weights of these companies are expected to double at the next rebalance in October 2022. Considering all changes for the April 2022 rebalance, the one-way turnover incurred was 24.5%.

China and Brazil Increased Their Presence in the S&P Global Clean Energy Index

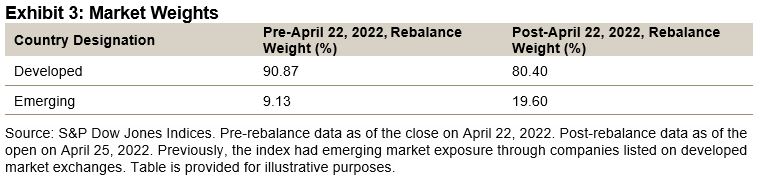

The countries with the most additions were China (16) and Brazil (6), which increased their respective country weights to 11.7% and 3.9% within the index. Conversely, companies from Denmark and the U.K. were most affected in the opposite direction, with decreases of 3.35% and 4.14%, respectively (see Exhibit 2). Overall, emerging market companies have increased their overall weight in the index by 10%, representing close to 20% of the S&P Global Clean Energy Index. At full inclusion, after the October 2022 rebalance, we anticipate that this figure will rise above 25% (see Exhibit 3).

Emerging Markets Inclusion Has Improved the S&P Global Clean Energy Index

Our analysis in this blog highlights that the expansion has aligned the index even more with its intent to focus on companies that are related to clean energy. Additionally, the broader index delivers greater geographical diversification. The International Energy Agency5 has seen a 50% increase in clean energy spending since October, and it has noted that it expects this to increase. As the clean energy transition takes shape in emerging economies,6 we expect these developments to be fairly reflected within the S&P Global Clean Energy Index.

1 Rajendra, Ari. “S&P Global Clean Energy Index: A Path toward Greater Transparency.” S&P Dow Jones Indices. Oct. 20, 2021.

2 The S&P Global Clean Energy Index previously included emerging market companies that were listed on developed exchanges.

3 All companies in the S&P Global Clean Energy Index universe are assigned exposure scores that denote their involvement in clean energy-related businesses. An exposure score of 1 is assigned to companies with maximum clean energy exposure, 0.75 to companies with significant clean energy exposure, 0.5 to companies with moderate clean energy exposure, and 0 to companies with no exposure.

4 The carbon-to-revenue (carbon intensity) footprint standard score is calculated for each stock in the preliminary universe. The score is calculated by subtracting the mean carbon-to-revenue footprint of all preliminary universe stocks with an exposure score of 1 as of the rebalancing reference date from each stock’s carbon-to-revenue footprint, and then dividing the difference by the standard deviation (also determined based on preliminary universe stocks with an exposure score of 1). The top and bottom 5% are excluded from the mean and standard deviation calculations. Companies with a score greater than 3 will not be eligible for inclusion.

5 International Energy Agency. “Clean Energy Spending Has Surged 50%.” April 12, 2022.

6 International Energy Agency. “Clean Energy Transitions in Emerging Economies.”

The posts on this blog are opinions, not advice. Please read our Disclaimers.