It is that time of year yet again: the seasons are changing, spring is in the air and the S&P 500® ESG Index has undergone its fourth annual rebalance. Just as it has in years past, the changes of the 2022 rebalance reflect the delicate balancing act of providing for broad-based market exposure but with meaningful and measurable sustainability-focused enhancements.

Without further ado, let’s spring into some of those changes.

The Results

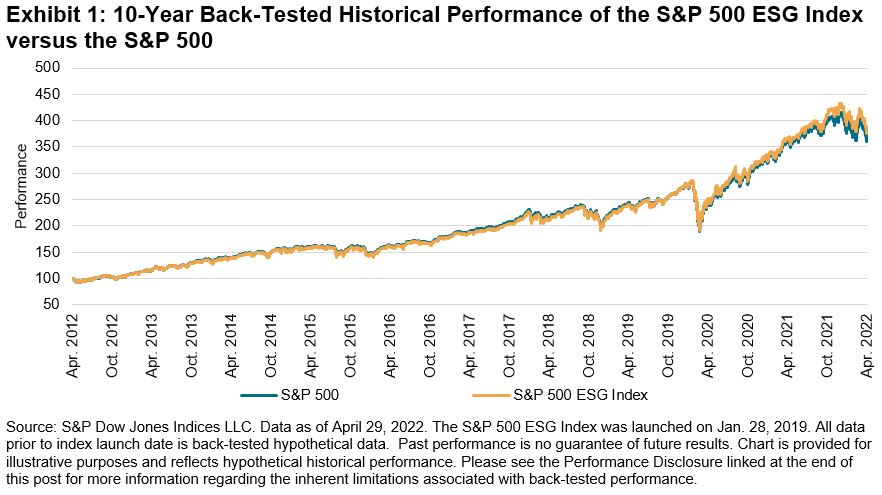

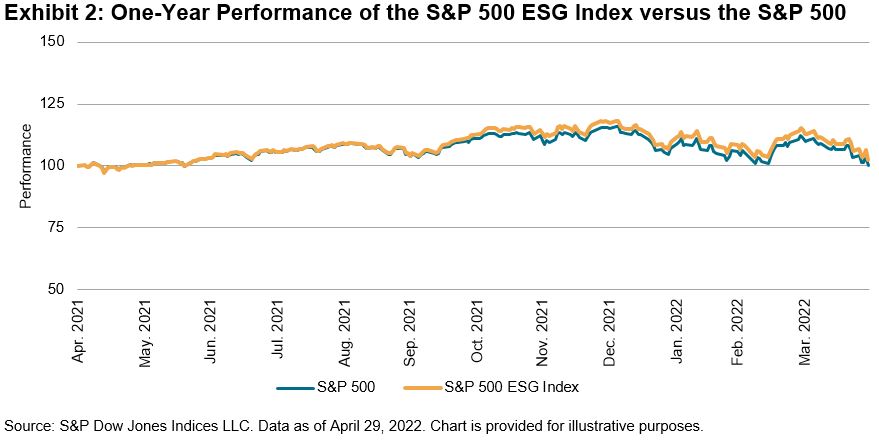

It is important that the methodology of the S&P 500 ESG Index reflect the evolving sentiments of a sustainability-minded investor. These views were voiced in the results of a recent market consultation that led to a revised and expanded list of exclusions based on a company’s involvement in certain business activities such as small arms, military contracting and oil sands. The consultation also addressed several other relevant updates, including more frequent eligibility check for business involvement and UNGC exclusions.1 Even with these enhancements, the S&P 500 ESG Index design still retains its main objective, which is to maintain similar overall industry group weights to the S&P 500 while enhancing the overall sustainability profile of the index. The index has indeed been able to accomplish this delicate balancing act, exhibiting a similar historical risk/return profile to that of the S&P 500 as well as an improvement in S&P DJI ESG Score2 (see Exhibit 1)—even achieving a bit of welcomed outperformance over the past one year (see Exhibit 2).

Who’s In and Who’s Out

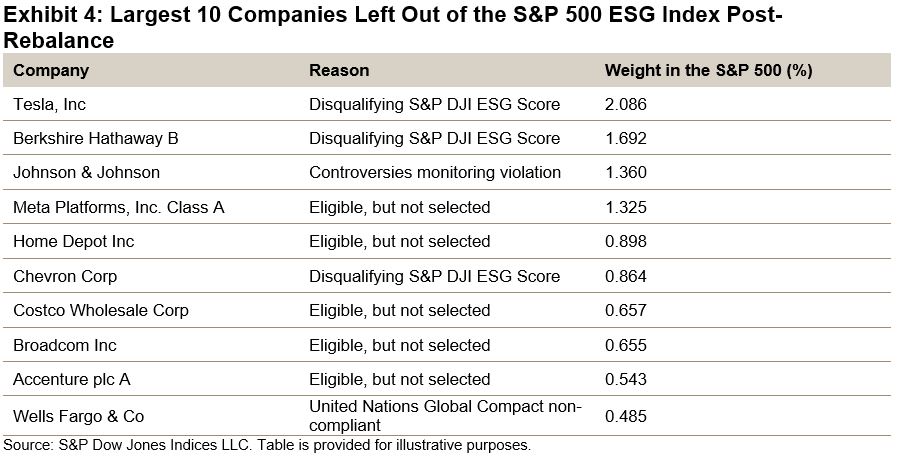

Of the 308 constituents that were selected for inclusion in the S&P 500 ESG Index, names like Apple, Microsoft, Amazon and Alphabet once again made the cut (see Exhibit 3).

However, one familiar name may stick out as being absent from that list: Tesla. Tesla was ineligible for index inclusion due to its low S&P DJI ESG Score,3 which fell in the bottom 25% of its global GICS® industry group peers. It joins Berkshire Hathaway, Johnson & Johnson and Meta, which have once again met the index methodology’s chopping block (see Exhibit 4).

But, how can a company whose self-declared mission is to “accelerate the world’s transition to sustainable energy” not make the cut in an ESG index? There are many reasons.

Talking Tesla

First and foremost, the GICS industry group in which Tesla is assessed (Automobiles & Components) experienced an overall increase in its average S&P DJI ESG Score. So, while Tesla’s S&P DJI ESG Score has remained fairly stable year-over-year, it was pushed further down the ranks relative to its global industry group peers.4 A few of the factors contributing to its 2021 S&P DJI ESG Score were a decline in criteria level scores related to Tesla’s (lack of) low carbon strategy5 and codes of business conduct.6 In addition, a Media and Stakeholder Analysis,7 a process that seeks to identify a company’s current and potential future exposure to risks stemming from its involvement in a controversial incident, identified two separate events centered around claims of racial discrimination and poor working conditions at Tesla’s Fremont factory, as well as its handling of the NHTSA investigation after multiple deaths and injuries were linked to its autopilot vehicles. Both of these events had a negative impact on the company’s S&P DJI ESG Score at the criteria level, and subsequently its overall score. While Tesla may be playing its part in taking fuel-powered cars off the road, it has fallen behind its peers when examined through a wider ESG lens.

Onward and Upward

So, while Tesla and others may not have been included in the index this year, the beauty of the annual rebalance is that they will once again have an opportunity to be reviewed for inclusion in years to come. For now, the (re)balancing act of the S&P 500 ESG Index has once again been achieved.

More information about the S&P 500 ESG Index methodology can be found here.

For more information about hypothetical back-tested data, please see the Performance Disclosure. For information about the creation of Back-Tested Data with respect to the S&P 500 ESG Index, please also see the Back-Tested Data Assumptions FAQ.

1 Maria Sanchez. “What Is New in S&P ESG Indices?” S&P Dow Jones Indices. April 27, 2022.

2 The index achieved an S&P DJI ESG Score improvement of 8.79% (at the index level), representing 28% of the overall ESG improvement potential, given the sustainability characteristics of the starting universe.

3 The S&P DJI ESG Scores are the result of further scoring methodology refinements to the S&P Global ESG Scores that result from S&P Global’s annual Corporate Sustainability Assessment, a bottom-up research process that aggregates underlying company ESG data to score levels.

4 Tesla’s S&P Global ESG Score improved 13 points from 2020 to 2021, whereas the S&P DJI ESG Score declined 2 points over the same time period. While several components of the scoring process are the same, such as the underlying research methodology, data collection and quality assurance, there are meaningful differences in the scoring process between S&P Global ESG Scores and S&P DJI ESG Scores. For more information on these differences, please visit FAQ: S&P DJI ESG Scores

5 Low Carbon strategy criteria focus on companies’ strategies to reduce the carbon intensity of its car portfolio (efficient technologies), but also assess its current portfolio exposure to regulatory risks.

6 Codes of business conduct criteria encompass a company’s implementation, transparent reporting on breaches and the occurrence of corruption and bribery cases and anti-competitive practices.

7 The Media & Stakeholder Analysis is an ongoing screening of company controversies that may have financial or reputational impacts on companies assessed in the Corporate Sustainability Assessment.

The posts on this blog are opinions, not advice. Please read our Disclaimers.