The theme of International Women’s Day 2022 is #breakthebias, pushing for organizations to be equitable and inclusive places of work for all. This aligns with our belief at S&P Global that an inclusive economy is one where women can fully participate in the global economy. The positive correlation between gender diversity in the workplace and corporate performance is undeniable—female representation has shown to enhance performance metrics while improving economic productivity and reducing volatility.1 Yet women remain largely underrepresented in the workforce, often due to social discrimination, lack of incentives or antiquated corporate provisions. This can result in negative financial consequences for internal and external stakeholders. Equally, strong gender and diversity integration creates an investment opportunity. The S&P Developed 100 Gender and Diversity Index seeks to track 100 developed market companies that are committed to creating a diverse and inclusive workplace free from bias and discrimination.

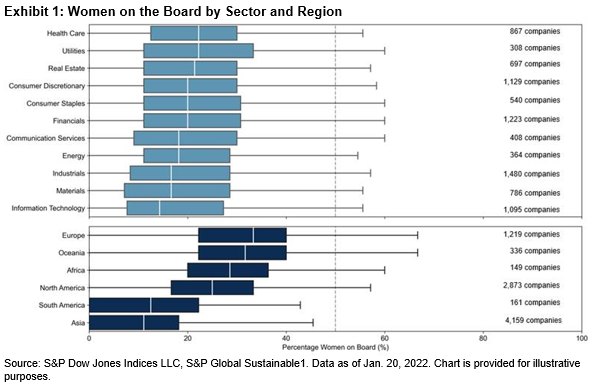

Female Representation Differs across Sectors

The Black Lives Matter and #metoo movements of 2020 have driven global attention toward inclusion and diversity in the workforce. Consequently, more corporations are disclosing these metrics. With increased disclosure, investors gain better insight into the divergence of female representation across sectors and regions, with popular metrics such as women on the board still showing that women remain grossly underrepresented across business.

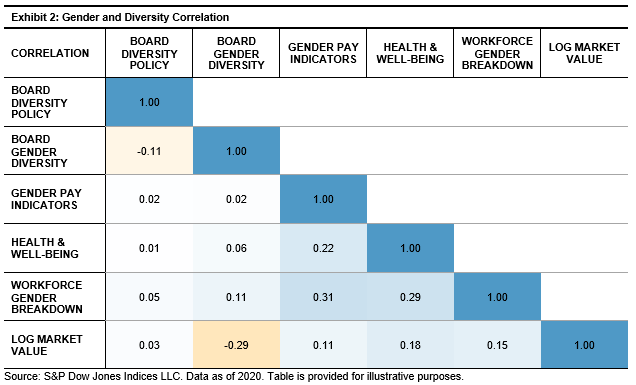

Diversity Metrics Have Low Correlation, so Granular Data Is Essential

Promoting equality in the workplace is about more than having a policy in place. It is about creating a culture where difference is valued and bias is halted. To achieve long-term shareholder value, investors need to determine a company’s true performance across numerous indicators. This is because gender and diversity metrics have low correlation, so you need to gain insight by looking beyond the policy. Having a policy in place does not mean you have created a culture where women are integrated and accepted throughout the corporate ladder.

To understand corporate culture toward inclusion and diversity, you need to aggregate multiple sources of granular data. Leveraging the S&P Global Corporate Sustainability Assessment, the S&P DJI ESG Scores can measure company commitment to gender equality using several frameworks such as board diversity, board gender diversity, workforce gender breakdown, gender pay indicators and health and well-being. This holistic insight into a company’s values and their actions can help us calculate company performance on gender equality and create a transparent and simple scoring approach to use as the basis of our index methodology.

Conclusion

International Women’s Day is not just about women’s equality, it is about creating a society where diversity is accepted and building a sustainable future where no one is left behind. The S&P Developed 100 Gender and Diversity Index strives to track those companies that embody these values and are committed to diversity at all levels. As we look to #breakthebias in 2022, I am reminded of a quote from Gloria Steinem.

“The story of women’s struggle for equality belongs to no single feminist nor to any one organization but to the collective efforts of all who care about human rights.”

1 Cristian L. Deszõ and David Gaddis Ross, “‘Girl Power: Female participation in top management and firm performance,” working paper, December 2007.

Avivah Wittenberg-Cox and Alison Maitland, “Why Women Mean Business: Understanding the Emergence of Our Next Economic Revolution,” Chichester, England: John Wiley & Sons, 2008.

The posts on this blog are opinions, not advice. Please read our Disclaimers.