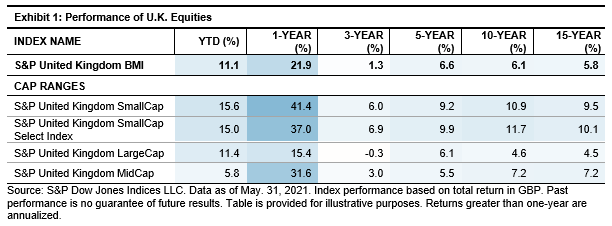

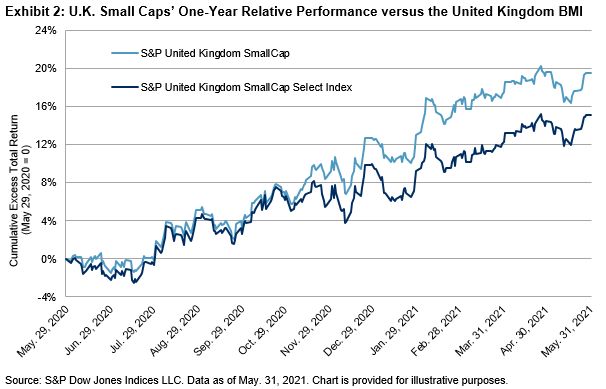

A gap between the 12-month performances of the S&P United Kingdom SmallCap and S&P United Kingdom SmallCap Select Index hints at a “junk rally” in U.K. stocks, but the longer-term data suggests that those looking to participate in an ongoing recovery in the world’s fourth-largest economy might be wise to maintain a selective approach.

As the global recovery from the coronavirus pandemic continues, the U.K. economy has picked up a head of steam, with the Bank of England forecasting over 4% GDP growth in Q2 alone. The pound sterling has surged to a near three-year high versus the U.S. dollar and, although the local equity markets aren’t quite back to pre-pandemic levels, they appear to be on the right track, with the S&P United Kingdom BMI adding 11% so far in 2021. Carrying a natural domestic focus and higher gearing to the economy, small-cap companies are benefiting the most from the optimism and the British “recovery trade,” outperforming the broad market index by five percentage points YTD.

However, within small-cap U.K. equities, there has also been something of a junk rally, with the outperformance of lower-quality stocks creating a more than 5% performance gap over the past year between the S&P United Kingdom SmallCap and the S&P United Kingdom SmallCap Select Index, the latter of which is designed to measure constituents of the S&P United Kingdom SmallCap with a track record of positive earnings. This echoes a recent inverse relationship between profitability and performance on the other side of the pond that we highlighted in May’s S&P 500 Factor Dashboard.

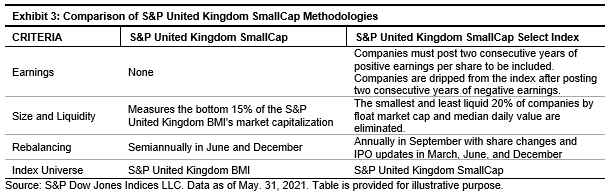

So, is there still a benefit to be gained by screening out the lower-quality names from small caps? As a recap for those who might not have met our “select” range of global small-cap indices, they are formed from their respective small-cap universes (in this case, the smallest 15% of companies by capitalization in the broad-based S&P United Kingdom BMI) by requiring two consecutive years of positive earnings per share at the point of index entry. Companies are also dropped if they post two consecutive years of negative earnings, while, to aid market participants hoping to replicate the index’s return, the smallest 20% and least liquid 20% of companies are excluded.

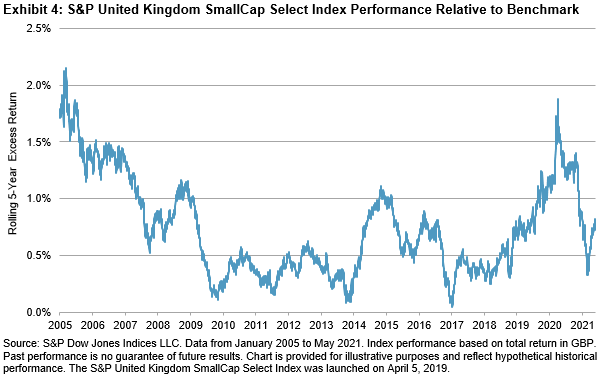

The potential benefits of the “select” methodology are illustrated in Exhibit 4, which plots the difference in five-year annualized returns between the S&P United Kingdom SmallCap and S&P United Kingdom SmallCap Select Index over the past 15 years. The S&P United Kingdom SmallCap Select Index outperformed across every rolling five-year interval including, despite the recent rally in unprofitable companies, the period ending in May 2021. Further, the winds may have changed, with the series appearing to take on an upward trend early in 2021.

The booming prospects for the world’s fourth-largest equity market may be tempting market participants to return to U.K. equities after a long period in the doldrums, and smaller U.K. companies may be well positioned to participate in growth. But it is worth emphasizing that while unprofitable companies may be currently in the lead this year, filtering out less profitable firms has, over the long term, made a big and positive difference in small caps.