Since its index inception on March 31, 2005, the Dow Jones International Dividend 100 Index has delivered significant outperformance, on a total return basis, over the broader market, as represented by the Dow Jones Global ex-U.S. Index.

The Dow Jones International Dividend 100 Index generated an annualized return of 8.82%, compared with 6.05% from the global ex-U.S. index (see Exhibit 1). Taking volatility into consideration, the risk-adjusted returns from the Dow Jones International Dividend 100 Index exceeded the benchmark across the long- and short-term history. During the 15-year horizon, the Dow Jones International Dividend 100 Index provided a risk-adjusted return of 0.55, which is 104% higher than the benchmark.

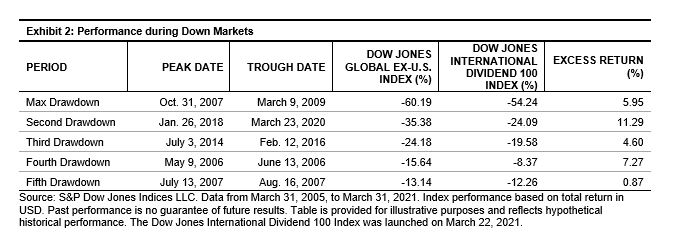

The Dow Jones International Dividend 100 Index has displayed defensive characteristics in volatile markets. Shown in Exhibit 2, the index beat the broader market during the five most-severe drawdown periods, creating an average excess return of 6%. We calculated capture ratios to see how the index performed during the upside and downside markets. Overall, the index captured 78% of the downtrend markets, meaning it suffered less loss than the broader market, as it would decline 7.8% when the benchmark is losing 10%. The index participated in most of the uptrend markets, with an upside capture ratio of 91%.

In addition to the solid outperformance seen in various market conditions, the Dow Jones International Dividend 100 Index provided sustainable dividend income in global markets. The dividend yield has stayed above 3% and averaged 4.33% (see Exhibit 3) over the past 15 years.