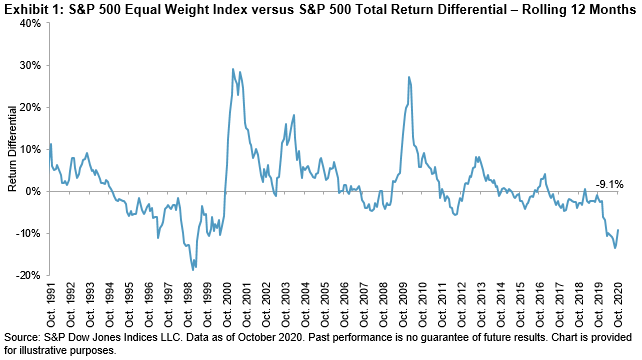

The S&P 500® rose by 10% in the 12 months ending on Oct. 31, 2020, trouncing the S&P 500 Equal Weight Index by 9.1%, as seen in Exhibit 1. While such outperformance is not unprecedented, it does remind us of previous market peaks (especially in December 1999), and raises questions about whether a reversal may be in the cards.

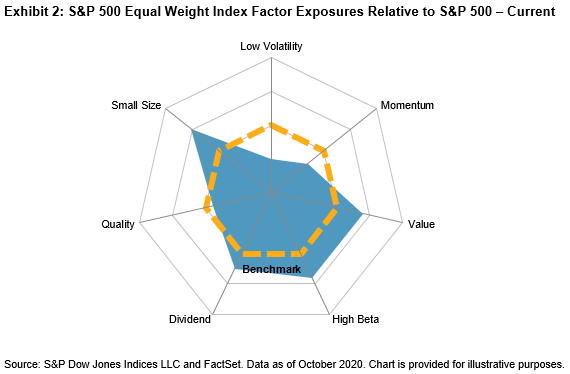

While these periods may feel similar, they have notable differences. It is important to remember that by definition, the capitalization-weighted S&P 500 has no factor tilts. We can, however, look under the market’s figurative hood by analyzing the differences between the S&P 500 and its average constituent, represented by the S&P 500 Equal Weight Index. Exhibit 2, excerpted from our monthly factor dashboard, shows the factor tilts of the S&P 500 Equal Weight Index, relative to the (capitalization-weighted) S&P 500.

Currently, the equal weight version has a strong tilt away from low volatility and momentum, and a slight tilt away from quality. It also has exposures toward small size, dividend yield, high beta, and value. In other words, compared to the average stock in the index, the S&P 500 itself is less volatile, more momentum-oriented, more expensive, and much larger.

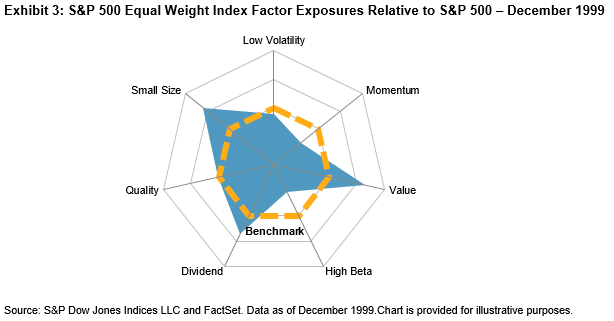

But when we go back further in history, we observe significant differences between today’s factor dynamics compared to those in December 1999. We observe in Exhibit 3 that like today, the equal weight version had a strong tilt away from momentum and toward small size, but that is where the similarities end. Twenty years ago, the S&P 500 Equal Weight Index barely had a tilt away from low volatility, deeper exposures to quality and dividend yield, along with a strong tilt away from high beta. Therefore, compared to the average constituent, the S&P 500 was much more volatile and not as durable from a quality perspective.

The fact that today’s market is less volatile and of higher quality compared to 1999 is not surprising, as the companies within Information Technology, the S&P 500’s largest sector then and now, are both more profitable and less volatile than they were 20 years ago. While we cannot predict whether the market’s upward trajectory is sustainable, history enables us to better understand the motions of the market from a factor lens.

The posts on this blog are opinions, not advice. Please read our Disclaimers.