In response to COVID-19 and its disruptive impact on the credit market, the U.S. Federal Reserve announced the creation of the Primary Market Corporate Credit Facility (PMCCF) and the Secondary Market Corporate Credit Facility (SMCCF) on March 23, 2020, to support the functioning of the credit market. The PMCCF provides a funding backstop for corporate debt to eligible issuers so that they are better able to maintain business operations and capacity during the period of dislocation related to COVID-19. The SMCCF supports market liquidity for corporate debt by purchasing individual corporate bonds of eligible issuers and exchange-traded funds (ETFs) in the secondary market. The combined size of both credit facilities is up to USD 750 billion.

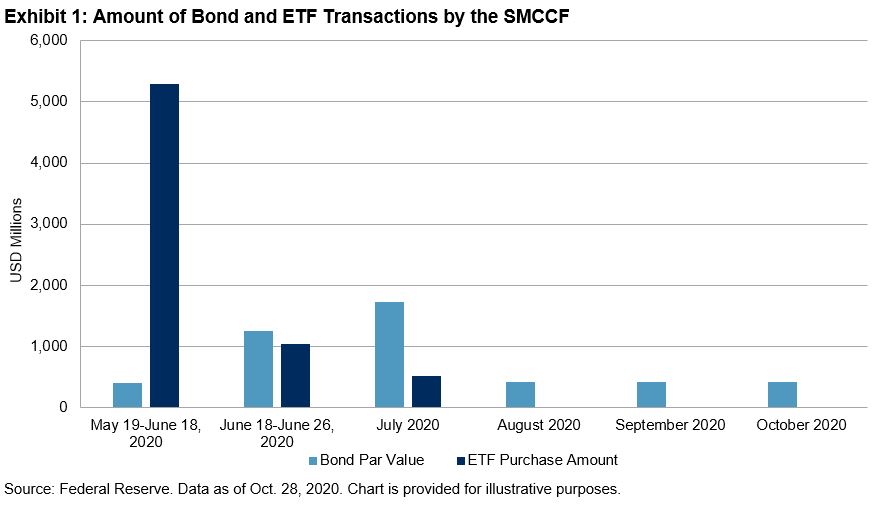

As of the end of September, the SMCCF had purchased only about USD 13 billion of eligible securities out of its capacity of USD 250 billion, while the PMCCF has not yet closed any transactions. Exhibit 1 shows transactions in the SMCCF since it started purchasing corporate bond ETFs in May. The majority of ETF purchases were executed in May and June, while in August, September, and October the Fed stopped adding ETFs to the SMCCF. Individual bond purchases were more stable during this period of time, totaling a par amount of USD 4.5 billion as of Oct. 28, 2020.

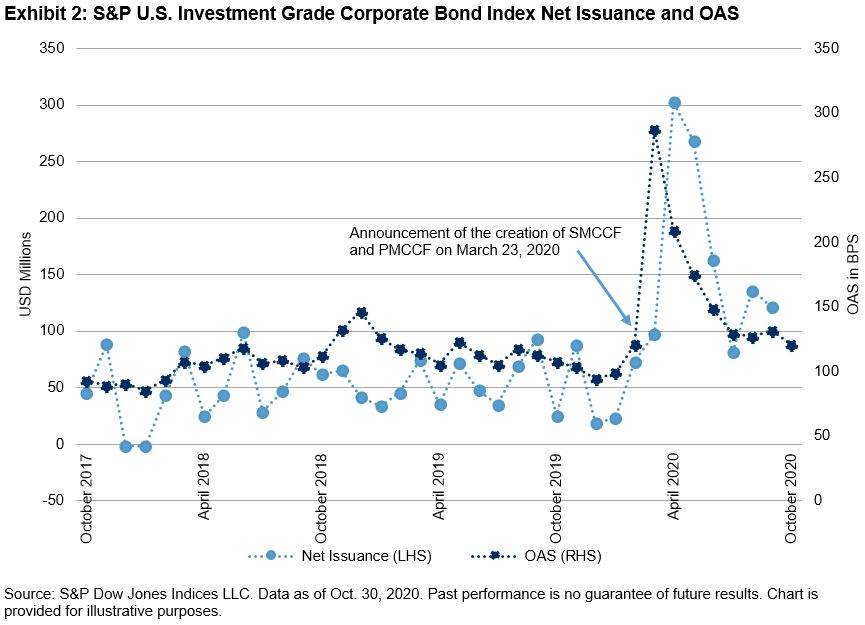

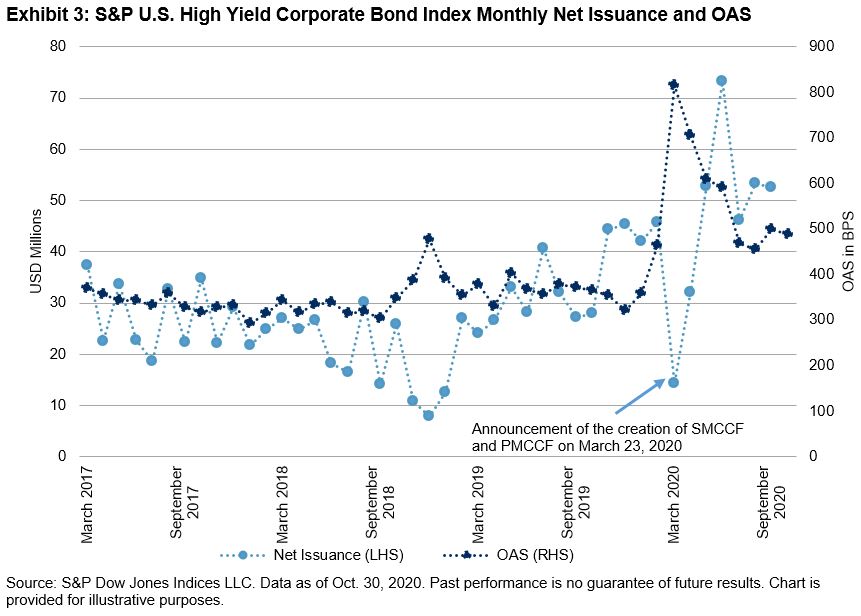

The main objective of the Fed’s credit facilities is to provide a liquidity backstop for corporate bonds and improve credit market functioning. One important measure of orderly market functioning is issuers’ access to the primary market. Exhibits 2 and 3 show net issuance amounts in the S&P U.S. Investment Grade Corporate Bond Index and S&P U.S. High Yield Corporate Bond Index, respectively. For the S&P U.S. Investment-Grade Corporate Bond Index, there was barely any lasting disruption, as net issuance was up 26% in Q1 2020 and more than tripled in Q2 and Q3 2020 combined compared with the same quarters in 2019. For the S&P High Yield Corporate Bond Index, the impact of the Fed’s credit facilities on new bond issuance was more visible. In March, high-yield bond net issuance dropped 40% versus March 2019, when index credit spreads widened to 815 bps; then, issuance recovered and rose 80% and 52% in Q2 and Q3 2020 compared with Q2 and Q3 2019, respectively.

It is interesting to note that high-yield bond issuance rebounded, and investment-grade bonds further strengthened, as soon as the announcement of both credit facilities in March, but before the commencement of actual purchases by the SMCCF, which began only on May 12, 2020, for bond ETFs and on June 16, 2020, for individual bonds. The fact that the Fed has achieved a rapid rebound of market issuance with only USD 13 billion of corporate bond and ETF purchases demonstrated the effectiveness of both corporate credit facilities in providing a funding backstop, though their long-term impact on the health of the credit market remains to be seen.

The posts on this blog are opinions, not advice. Please read our Disclaimers.