The contentious debate of active versus passive is perpetual. Over the past 15 years, SPIVA® Scorecard results have reflected on the trends of active fund management vis a vis benchmarks, wherein statistics tilt the balance in favor of indexing. This recurring feature of benchmark outperformance is contributing to the adoption and growth of the passive investment space.

India is participating in the global passive growth with assets crossing the USD 25 billion mark. Since 1999, S&P Dow Jones Indices has been contributing to Indian markets by sharing its global index expertise to offer passive solutions and educate investors on the benefits of passive investing. The SPIVA India scorecard made its debut in 2013, and the results bear similarities to global trends. One category that stands out in its potential for passive allocation is the large-cap space, which the benchmark S&P BSE 100 has consistently outperformed (see Exhibit 1).

Asset allocation models are critical to achieving a portfolio’s investment objective. Beyond asset class diversification, a combination of strategies can prove beneficial. This is where the core and satellite strategy assists in effective portfolio construction. A strong core provides stability and can contribute to risk mitigation and, ultimately, reaching the financial objective of the portfolio.

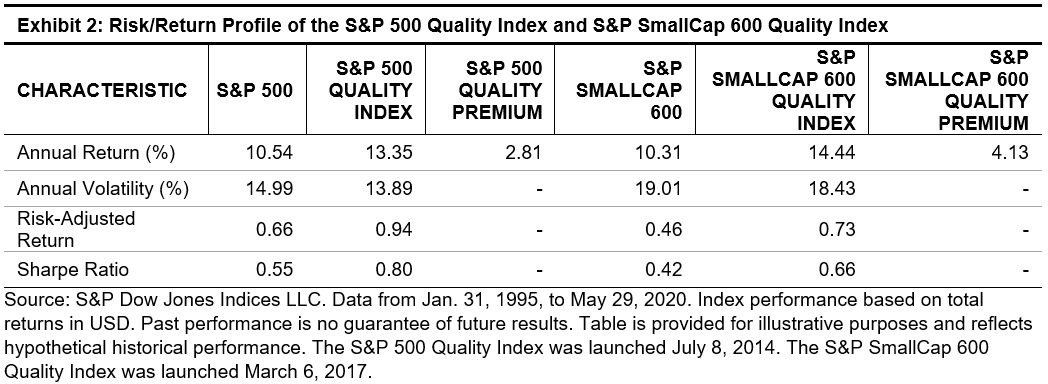

Indexing offers the benefits of diversification, lower costs, transparency, lack of fund manager bias, flexibility, and a variety of investment categories from which to choose. These options vary from standard market beta to factor-, theme-, or strategy-based indices. Region and asset class can further widen the gamut of options. Exhibit 2 is demonstrative of the variance in performance of a standard Indian equity market benchmark versus a fixed income index, a factor-based index such as low volatility, a sectoral index, and a global index such as the S&P 500® over different time periods. Portfolio and investment goals can be directional in their core allocation strategy using various indexing alternatives. An active strategy as a satellite can selectively explore the inefficiencies in the market and scope undervalued market opportunities toward the achievement of the overall portfolio objective.

The core and satellite strategy can be used to derive the best of both worlds by using a diverse selection of indices as the core that provides the benefits of indexing, complemented by an active strategy as the satellite, thereby using a combination of a strategic and tactical allocation approaches to portfolio construction.

The posts on this blog are opinions, not advice. Please read our Disclaimers.