In early March 2020, S&P Dow Jones Indices released the SPIVA Australia Year-End 2019 Scorecard. With the market gyrations in late February and March due to the COVID-19 pandemic spreading across the globe, we decided to provide a “mid-term” SPIVA update to include data up to March 31, 2020, and to share the timely results through the webinar, Harnessing Active Vs. Passive Findings During Times of Market Turbulence. So, what did we find?

Q1 2020 Market Performance

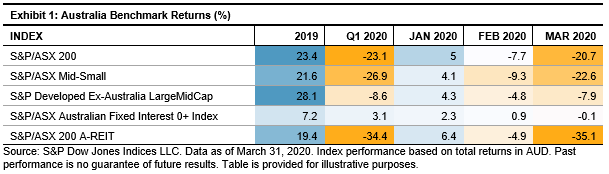

With the exception of Australian bonds, all asset classes suffered drawdowns, with the S&P/ASX 200 seeing a drawdown of 23%. The S&P/ASX 200 A-REIT experienced a drawdown of 34.4%.

Q1 2020 Fund Performance

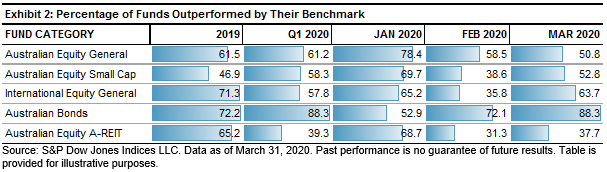

As Exhibit 2 shows, for the three-month period ending March 31, 2020, 61.2% of funds in the Australian Equity General category were outperformed by the S&P/ASX 200. This was more or less in line with the results as of Dec. 31, 2019. What becomes more interesting is when we look at the results on a month-by-month basis, we saw a steady improvement in the performance of funds in that category across the three-month period, with the number of funds outperformed by the benchmark decreasing from 78.4% to 50.8%. To put this another way, in January 2020, 21.6% of funds outperformed the benchmark, in February 2020, this increased to 41.5%, and in March 2020, it increased to 49.2%. The volatile market appears to have provided active fund managers opportunities to outperform the benchmark, although the benchmark still outperformed greater than 50% of funds.

Other fund categories were also not able to beat the benchmark in Q1 2020, with the exception of A-REITs. For the three-month period, 39.3% of A-REIT funds were outperformed by the benchmark.

While opportunities for outperformance by active fund managers may have increased in Q1 2020, most continued to underperform their relevant benchmarks. The challenge remains. How can investors, or financial advisors, select outperforming funds in advance? 2020 hindsight continues to prevail in 2020.

How Does SPIVA Assist Financial Advisors?

David Haintz of Global Adviser Alpha joined our mid-term SPIVA results webinar and provided a wealth of advice for financial advisors. David’s advice can be heard starting at minute 23:45. A couple of key takeaways from his advice include the following.

- Rather than using the terms active and passive for investing, David suggests using the terms forecasting (active investing) and non-forecasting (passive investing). He is an advocate for non-forecasting, as when put to the test, the forecasters have not been able to demonstrate an ability to pick stocks, market timings, or active managers so that they consistently outperform relevant benchmarks. SPIVA has been a key tool in supporting a non-forecasting approach.

- When adopting a non-forecasting approach to investing, David suggests advisors take a three-step approach.

- Understand: Gather data and understand whether options available to clients add value or subtract value. SPIVA is a great resource to aid in your understanding;

- Believe: Look at the available alternatives and start to believe in what will be the best possible option for your clients; and

- Articulate: Once an advisor understands and believes in a non-forecasting approach, the articulation of that proposition is easy, as there is so much evidence for non-forecasting that your passion for this approach will naturally flow as you talk to your clients.

- Finally, when adopting a non-forecasting approach, be aware that this does not inoculate clients from negative markets. Keep your conversations with clients focused on their goals and aspirations, rather than on returns over 1, 3, or 12 months.

The posts on this blog are opinions, not advice. Please read our Disclaimers.