Summary

- With Q3’s earnings season substantially complete, 2019 earnings for S&P 500 companies are expected to decline on a year-over-year basis.

- After several strong quarters last year, the first three quarters this year have seen marked earnings deceleration.

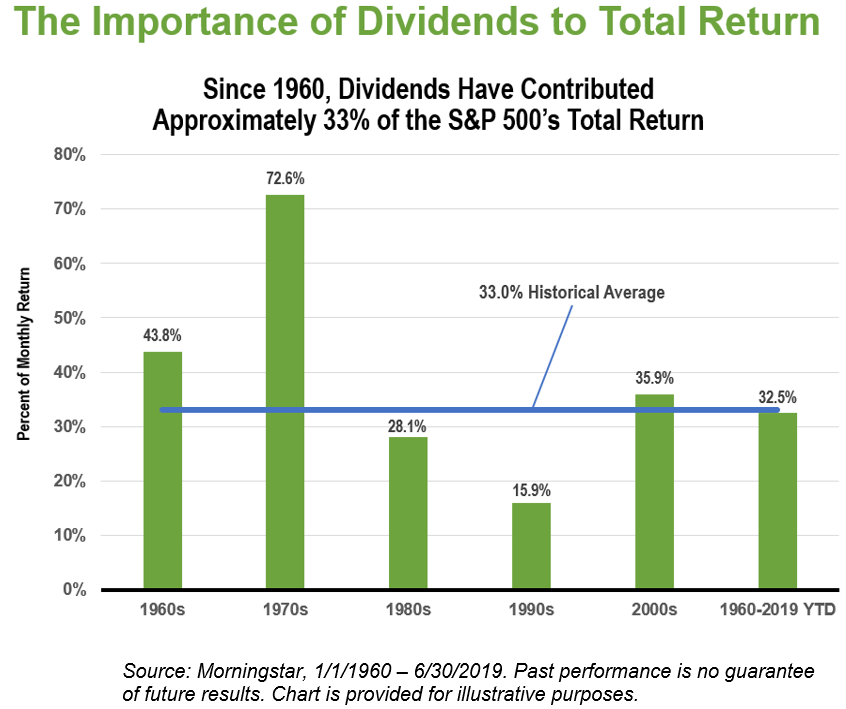

- Providing 1/3 of historical S&P 500 total returns, dividends could become important when the market may be near full valuation and corporate earnings are decelerating

- Indexes such as the S&P 500 Dividend Aristocrats track companies with long-term track records of continuous dividend growth. As such, funds that follow them may be worth a closer look.

Third Quarter Earnings on Pace to Decline Again

Through November 15, 92% of the S&P 500 constituents have announced earnings, and investors have been paying close attention. Most companies that have reported thus far have exceeded estimates, which had in many instances been guided lower. On the surface this is, of course, positive news. But when looking for year-over-year growth, a different story begins to emerge. While 2018 saw three quarters with 20% advances, year-over-year earnings growth in the first two quarters of 2019 decelerated markedly and ended flat to slightly down. As of November 15, the estimated earnings decline for Q3 2019 as compared with the same period in 2018 currently stands at just over 2%. If that turns out to be the case, when all is said and done, it would mark the third consecutive quarterly decline. Soon enough, investors will begin to ask the question of where the earnings are going to come from to support current valuations.

Decelerating Earnings Could Make Dividends More Important

In a market susceptible to fits and starts, investors remain understandably attracted to dividend strategies. Beyond the obvious appeal of a potential income stream during a time of low fixed-income yields, dividends have historically provided a sizeable slice of total-returns pie. In fact, dividends have accounted for roughly one-third of S&P 500 Total Return Index performance going back to 1960.

Interestingly, the contribution of dividends to returns has varied considerably over time. Dividends accounted for more than 72% of returns during the 1970s but less than 16% during the 1990s. So, considering their historical average around 33%, how important will dividends be going forward? A credible argument can be made that dividends are likely to represent an above-average proportion of, and be a significant contributor to, near-term returns.

The rationale behind this argument becomes apparent if we look at the relationship between dividend yield, earnings growth rate, and potential valuation changes from current levels. If: 1) one considers the market to be currently at or very near full valuation; and 2) the recent trend of flat to slightly-down earnings growth continues; then 3) it follows that dividends may indeed represent a greater-than-average portion of total returns going forward.

Dividend Growth Could Hold Even Greater Appeal

Given the potential above-average contribution to returns going forward and general investor appetite for dividends, quality companies that continuously grow their dividends could become even more appealing if earnings continue to decelerate. In particular, investors might want to look into the S&P 500 Dividend Aristocrats—high-quality companies that have not just paid dividends but grown them for at least 25 consecutive years. In fact, the Aristocrats delivered positive, if moderate, earnings growth during the first two quarters of 2019. Over time, companies that have grown their dividends like this generally have had stable earnings and solid fundamentals.

There are several indexes tracking long-term dividend growth companies—the S&P 500® Dividend Aristocrats® Index, the S&P MidCap 400® Dividend Aristocrats® Index, the S&P® Technology Dividend Aristocrats® Index and others—and there are ETFs that follow many of them. So, in a market with decelerating earnings, high-quality dividend growth investments could be worth a closer look.

The posts on this blog are opinions, not advice. Please read our Disclaimers.