S&P Indices Versus Active (SPIVA) scorecards provide mainstay performance comparisons between active managers and benchmarks. Our latest Institutional SPIVA scorecard shows once again how difficult active managers found it to beat benchmarks, net- or gross-of-fees. Here are a couple of highlights.

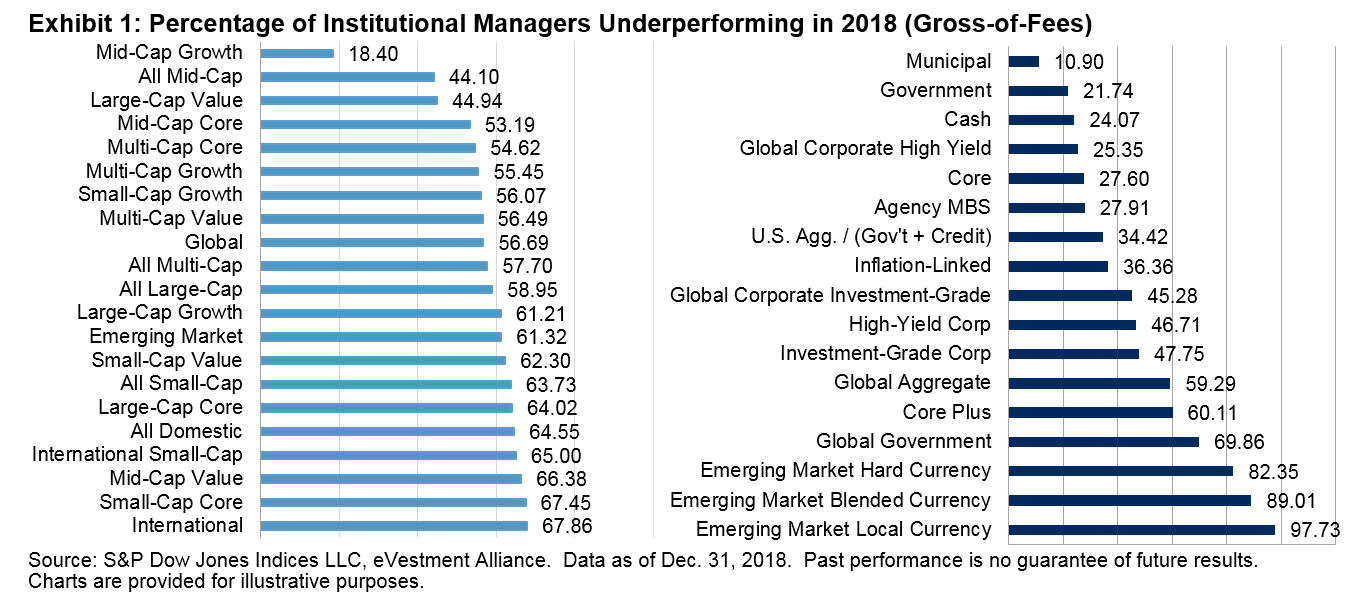

2018 proved challenging for institutional equity managers, although institutional fixed income managers showed some strength.

The fourth quarter of 2018 witnessed a complete turnaround in sentiment, as uncertainty over Fed policy and renewed trade tensions between the U.S. and China contributed to a rise in volatility. Although such conditions are commonly believed to favor active managers, the data suggests otherwise: in most categories, a majority of institutional equity funds underperformed their benchmarks last year, even gross-of-fees.

However, institutional active fixed income managers navigated the turbulence more surefootedly: a majority of managers beat their benchmarks, before fees, in 11 out of the 17 fixed income categories in 2018.

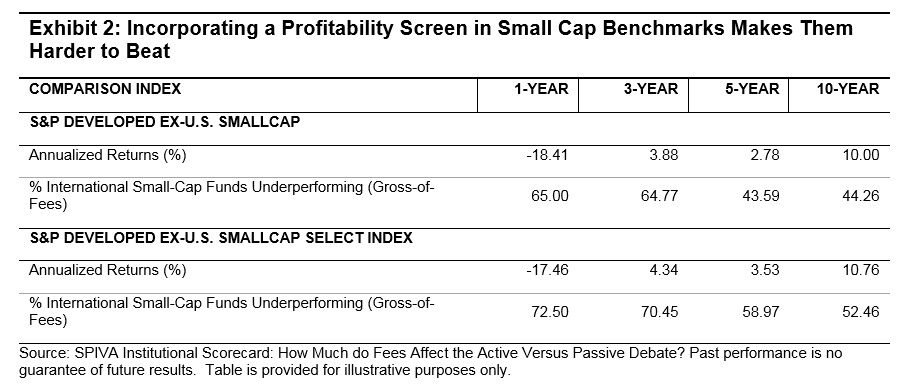

Incorporating a profitability screen in small cap benchmarks would have made them harder to beat.

We have written quite recently about the potential benefits of incorporating a profitability screen in small caps and S&P Dow Jones Indices launched the S&P Global SmallCap Select Index Series earlier this year in order to allow benchmark comparisons. Exhibit 2 shows the impact on the SPIVA statistics when switching our international small cap benchmark to one of these small cap select indices – the S&P Developed Ex-U.S. SmallCap Select Index.

Over every timeframe, more funds beat the S&P Developed Ex-U.S. SmallCap Index (which does not require small cap companies to have a track record of positive earnings) than the corresponding small cap select index (which does). And over the 5- and 10-year periods ending December 2018, such a switch in benchmarks would convert the international small cap category from one in which a majority of institutional active funds outperformed, to a one in which a majority underperformed.

To find out more about the latest results and for more information on the active versus passive debate, visit out SPIVA microsite.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

Exhibit 2 displays the stress scenario analysis for the S&P U.S. High Yield Low Volatility Corporate Bond Index since 2000. During the Q4 2018 and early January 2019 sell-off, when the broad market high yield bond index OAS widened by 199 bps from trough to peak, the S&P U.S. High Yield Low Volatility Corporate Bond Index outperformed the broad-based S&P U.S. High Yield Corporate Bond Index by 1.2%, while the latter suffered a loss of 4.1%. Other periods of market stress are also included that point to the defensive nature of the S&P U.S. High Yield Low Volatility Index.

Exhibit 2 displays the stress scenario analysis for the S&P U.S. High Yield Low Volatility Corporate Bond Index since 2000. During the Q4 2018 and early January 2019 sell-off, when the broad market high yield bond index OAS widened by 199 bps from trough to peak, the S&P U.S. High Yield Low Volatility Corporate Bond Index outperformed the broad-based S&P U.S. High Yield Corporate Bond Index by 1.2%, while the latter suffered a loss of 4.1%. Other periods of market stress are also included that point to the defensive nature of the S&P U.S. High Yield Low Volatility Index.