The S&P 500® is up 21.42% year-to-date and is within striking distance of its all-time high. Although this may suggest the presence of a strong “risk-on” environment, there are signs that the bull market’s stride is changing. Defensive assets have fared relatively well amid concerns over economic growth and trade tensions, while the inversion of several sovereign yield curves points to the unease being felt by many market participants.

Against this backdrop, many market participants may have considered switching asset allocations to adopt a more defensive approach – moving from equities to bonds, for example. However, such a strategy is not without its challenges: given the difficulty in timing the market correctly, one runs the risk of missing out on equity market gains or not having the desired downside protection when it is most desired. An alternative approach may be to use equity sectors.

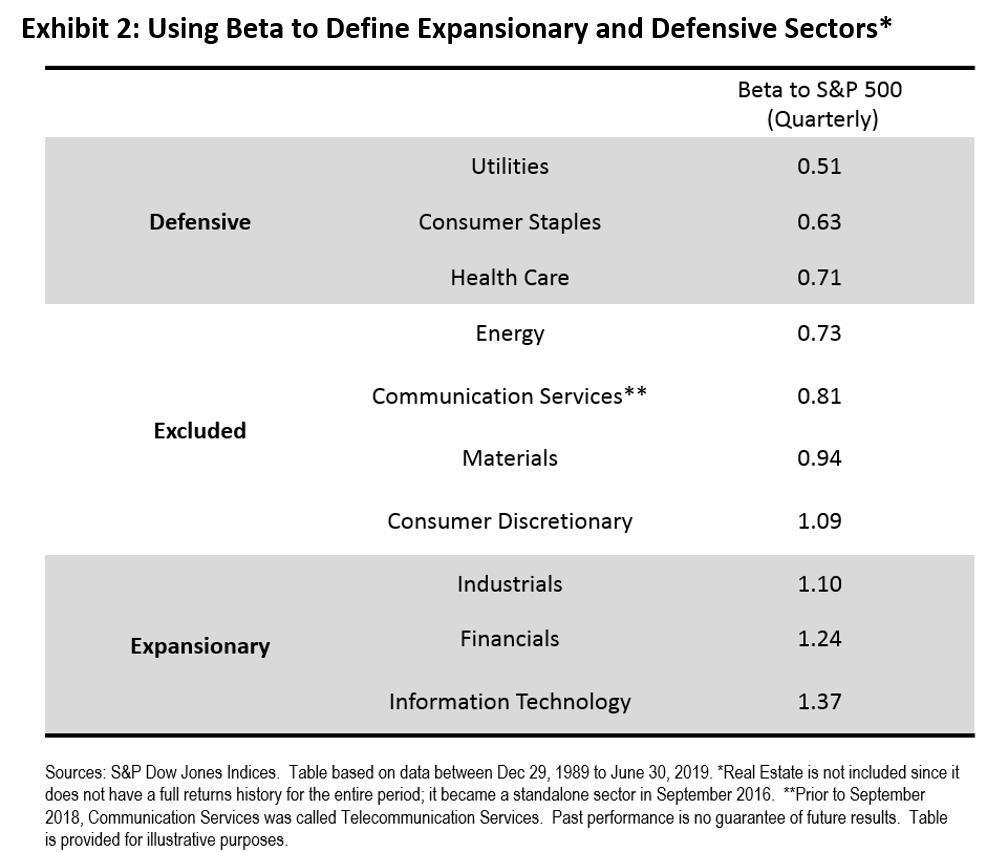

When implementing forecasts, it is imperative to know two pieces of information. First, what is going to happen? And once in possession of that information, what is to be done? Bypassing the challenges involved with predicting the future, we assume that market participants have perfect foresight over U.S. GDP growth. In order to help answer the second question, Exhibit 2 offers a simple categorization of S&P 500 sectors according to their betas to the S&P 500, based on quarterly total returns between Dec. 1989 and Jun. 2019. These categorizations are used in the hypothetical sector rotation strategy.

Next up, we compare the performance of 3 hypothetical portfolios, each of which rebalances at the end of each quarter and maintains approximate 60/40 equity/bond allocations. The “Benchmark 60/40” portfolio maintains a 60% allocation to the S&P 500 and a 40% allocation to the S&P U.S. Treasury Bond Index. The “Asset Rotation” strategy prescribes a 70/30 (or 50/50) ratio between the S&P 500/S&P U.S. Treasury Bond Index when U.S. GDP growth over the next quarter is above (or below) its median value for the period between Dec. 1989 and June 2019. The “Sector Rotation” portfolio maintains 40% allocations in each of the S&P 500 and the S&P U.S. Treasury Bond Index, and allocates 20% to an equally-weighted portfolio of expansionary (defensive) sectors when U.S. GDP growth in the next quarter is above (below) its median value for the entire period.

Exhibit 3 shows that both the hypothetical “Asset Rotation” and “Sector Rotation” portfolios offered similar risk/return characteristics, with higher annualized returns than the hypothetical “Benchmark 60/40” strategy.

Although this example involves substantial look-ahead bias – one would have needed perfect foresight over U.S. GDP growth to implement the hypothetical rotation strategies described above – the results illustrate a broader point: sector rotation strategies can be just as powerful as asset allocation in allowing market participants to express views.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

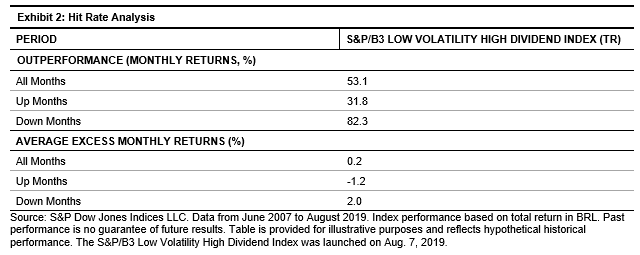

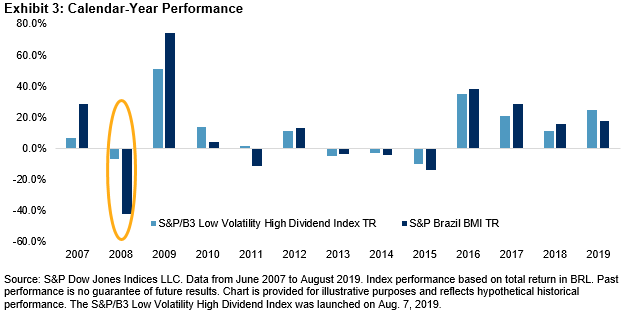

The S&P/B3 Low Volatility High Dividend Index provided downside protection in periods of market turbulence. During all the months in which the benchmark was down between June 2007 and August 2019, the S&P/B3 Low Volatility High Dividend Index outperformed 82.3% of the time and generated a monthly average excess return of 2% over the benchmark.

The S&P/B3 Low Volatility High Dividend Index provided downside protection in periods of market turbulence. During all the months in which the benchmark was down between June 2007 and August 2019, the S&P/B3 Low Volatility High Dividend Index outperformed 82.3% of the time and generated a monthly average excess return of 2% over the benchmark.

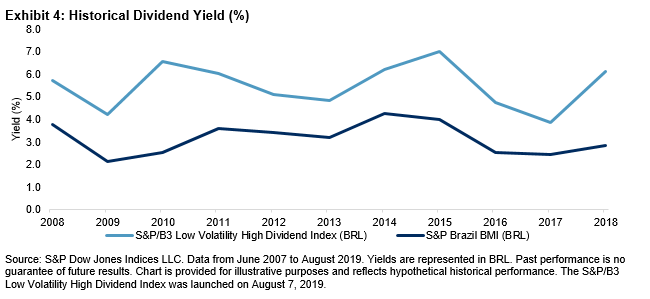

The S&P/B3 Low Volatility High Dividend Index was also able to generate higher yield than the S&P Brazil BMI. Over the studied period, the S&P/B3 Low Volatility High Dividend Index had an average historical yield of 5.5%, compared with 3.1% for the benchmark.

The S&P/B3 Low Volatility High Dividend Index was also able to generate higher yield than the S&P Brazil BMI. Over the studied period, the S&P/B3 Low Volatility High Dividend Index had an average historical yield of 5.5%, compared with 3.1% for the benchmark.

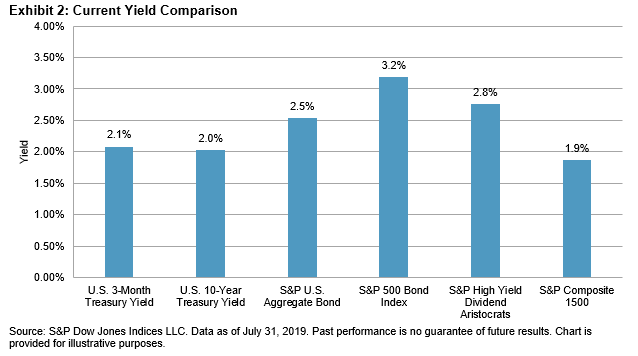

For comparison purposes, Exhibit 2 lists recent yields of selected securities and indices. As of July 31, 2019, the S&P High Yield Dividend Aristocrats had a dividend yield of 2.8%, which was higher than the yields of the other securities and indices shown, with the exception of the

For comparison purposes, Exhibit 2 lists recent yields of selected securities and indices. As of July 31, 2019, the S&P High Yield Dividend Aristocrats had a dividend yield of 2.8%, which was higher than the yields of the other securities and indices shown, with the exception of the