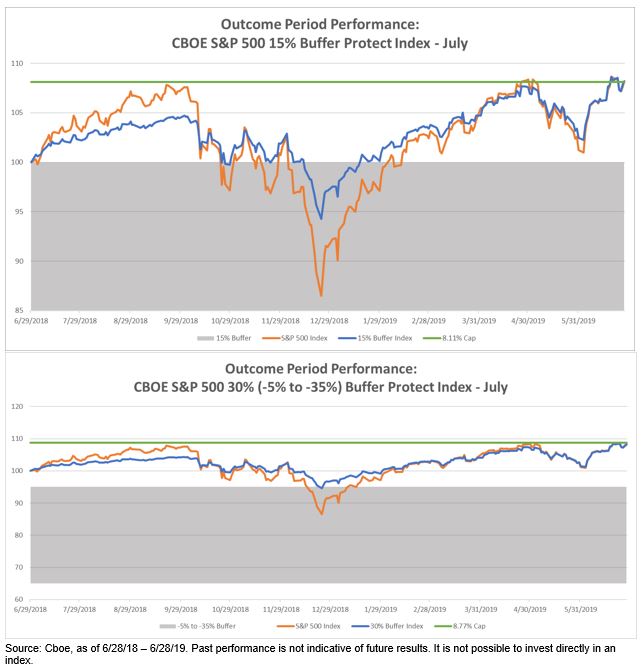

On June 28, 2019 the July Series of the Cboe S&P 500 Buffer Protect Indexes completed their first one-year outcome period (6/28/18 – 6/28/19). The Cboe S&P 500 Buffer Protect Indexes are designed to afford investors defined exposures to the S&P 500 Price Index, where the downside buffer levels, upside growth potential, and outcome period are all pre-determined. The approach taken by the Buffer Protect Indexes is analogous to certain equity-linked strategies used in structured products and indexed annuities—industries with more than $1 trillion in assets in the U.S. alone.

In short, the Buffer Protect Indexes performed as they were designed, exhibiting the same positive return as the S&P 500 Price Index over the outcome period, with approximately half the beta and a significantly lower maximum drawdown. The table and chart below depict the historical performance of two Cboe S&P 500 Buffer Protect Indexes:

- Cboe S&P 500 15% Buffer Protect Index – July Series: Designed to provide access to the price return of the S&P 500, to a cap, with a built-in buffer of 15%, over an outcome period of one year.

- Cboe S&P 500 30% (-5% to -35%) Buffer Protect Index – July Series: Designed to provide access to the price return of the S&P 500, to a cap, with a built-in buffer of 30% (beginning at -5%), over an outcome period of one year.

Did the Indexes Deliver a Defined Outcome?

Yes. The Indexes seek to match positive returns of the S&P 500 Index, to a cap, in up markets and in down markets, buffer investors against losses of 15% or 30% (-5% to -35%) over the outcome period. The S&P 500 was positive at the end of the outcome period, and the Buffer Protect Indexes matched the price returns of the S&P 500. Additionally, as a result of the downside buffers and upside caps, the Indexes experienced significantly less volatility and drawdowns than the S&P 500 along the way (while matching the return of the S&P 500 at the conclusion of the outcome period).

Implications

The investment community has been widely tracking the Cboe S&P 500 Buffer Protect Indexes, and the completion of their inaugural one-year outcome period was an important milestone in the adoption of “defined outcome” based investment strategies. This could add to financial advisors’ toolkit as they manage varied risk tolerance levels and investment objectives.

The posts on this blog are opinions, not advice. Please read our Disclaimers.