“Sustainable investing must go mainstream. Fortunately, the momentum is growing.” – Mark Carney

Mark Carney’s statement underpins the sentiment of the investment community, where environmental, social, and governance (ESG) considerations have entered the forefront of investors’ priorities.

Whether factor indices have ESG principles integrated or not, understanding a factor’s influence on ESG characteristics, such as the benefits of quality, can be advantageous.

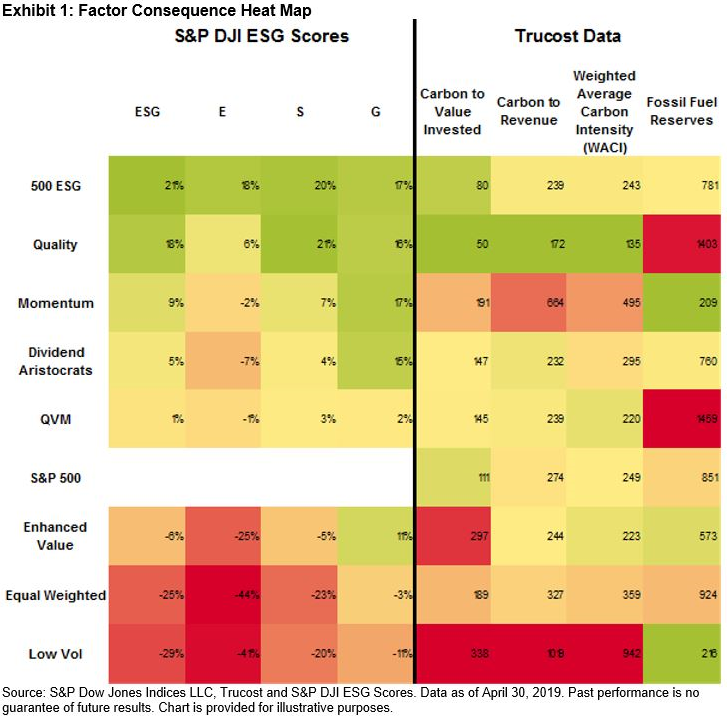

Exhibit 1 presents a heat map visualizing the S&P Factor Indices’ ESG exposures. This can be interpreted as red representing poor performance, yellow as middle, and green as strong, relative to the other indices.

Using S&P DJI ESG Scores, ESG improvements from the parent index were calculated as a percentage of possible ESG improvement if the total index weight were to be placed in the highest ESG-scoring stock (hence, there is no data for the S&P 500® as it is the benchmark for the factor indices analyzed). The S&P DJI ESG Scores are based on underlying data from SAM’s award-winning Corporate Sustainability Assessment combined with an S&P DJI methodology of how underlying data is treated and aggregated.[1]

The “ESG,” “E,” “S,” and “G” columns in Exhibit 1 refer to the improvement in the ESG, environmental, social, and governance levels of the S&P DJI ESG Scores, while the other columns refer to various Trucost carbon footprinting methods.

Exhibit 1 illustrates that factor exposures can have a strong influence on ESG scores.

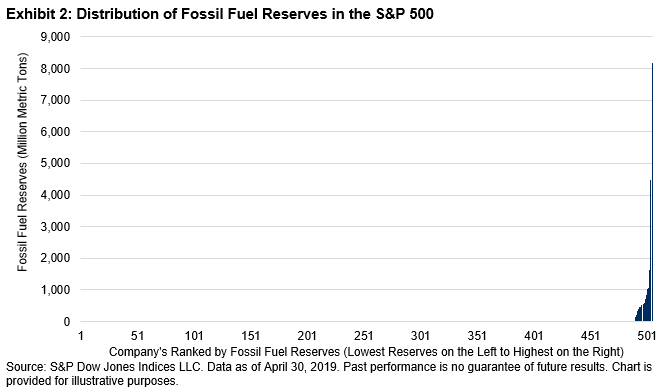

Quality topped all factors, showing strong ESG performance, fossil fuel reserves aside. Fossil fuel reserves, however, are driven largely by one company, Occidental Petroleum—only four companies included in the S&P 500 have any fossil fuel reserves. The nature of this metric, with only 16 S&P 500 constituents having fossil fuel reserves recorded by Trucost (see Exhibit 2), means the figure is skewed by including just one high fossil fuel reserve company. On the S&P DJI ESG Score front, quality performs well, seeing an ESG performance increase almost as high as the S&P 500 ESG Index, albeit with a stock count of less than a third.

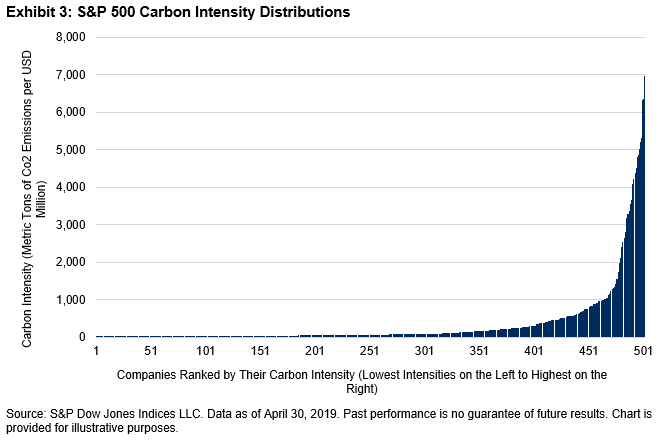

Alternately, the S&P 500 Low Volatility Index shows the poorest ESG characteristics, with a 29% ESG reduction, largely driven by a 41% environmental reduction, while also falling short on social and governance factors. These S&P DJI ESG Scores[2] are backed by poor carbon to value, carbon to revenue, and weighted average carbon intensity figures, which were the worst performers of the factor indices analyzed. The low carbon scores are unsurprising, considering the large number of Utilities companies with low volatility characteristics. Exhibit 3 illustrates the distribution of carbon intensities, heavily skewed as with the fossil fuel reserves.

A responsible investor may consider implementing a carbon reduction strategy for a low volatility index or combining ESG with low volatility to gain stronger ESG exposures while still capturing the low volatility risk premia. In the next blog, we’ll see what drives these scores, as well as how constant the sector allocations within factor indices are over time.

[1] “S&P DJI ESG Scores FAQ,” S&P Dow Jones Indices.

[2] “Index ESG Characteristics Explained,” S&P Dow Jones Indices.

The posts on this blog are opinions, not advice. Please read our Disclaimers.