When the S&P 500 ESG (Environmental, Social, and Governance) Index underwent its annual rebalance after markets closed on April 30, 2019, several notable companies were removed, including Wells Fargo, Oracle, and IBM. However, the largest component to be dropped was Facebook.

A day before its exclusion, Facebook held a weight of 2.5% in the S&P 500 ESG Index. At that time, Facebook was the fourth-largest company in the S&P 500, the parent index for the S&P 500 ESG Index, with a weight of 1.9%.

Why was Facebook removed? To better understand, a primer on the S&P ESG Index Series methodology[1] is helpful.

Some ESG indices, like the Dow Jones Sustainability Indices,[2] are narrow in their construction, selecting only a few leading companies in sustainability, industry by industry. Other ESG indices, such as the S&P 500 ESG Index, keep broad exposure but exclude companies lagging in ESG performance or that are involved in certain business activities, such as the production of tobacco or controversial weapons.

To keep alignment with the S&P 500 and to exclude companies underperforming in ESG, companies are ranked within their S&P 500 GICS® industry groups by their S&P DJI ESG Scores. They are then selected, highest to lowest, with the aim of getting as close as possible to a market capitalization threshold of 75% within each industry group.

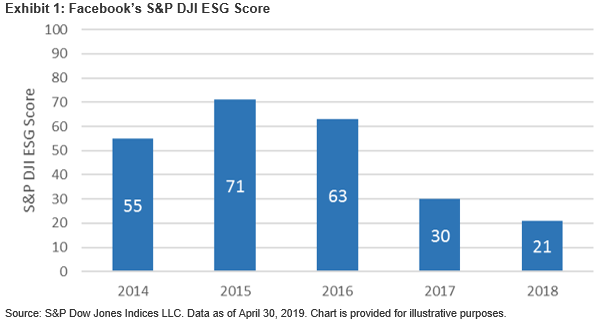

In the case of Facebook, its overall S&P DJI ESG Score was 21, out of a range of 0 to 100, with 100 being best. This low score resulted in Facebook not being selected as part of the approximately 75% of the Media & Entertainment industry group’s market capitalization included in the S&P 500 ESG Index.

Drilling down further, though its environmental score was strong at 82, this sub-score only carried a 21% weight in determining its aggregate ESG score, as environmental issues tend to be less material for tech companies. More impactful were its social and governance sub-scores, which registered at 22 and 6, respectively. These scores carried weights of 27% and 52%, respectively.

The specific issues resulting in these scores had to do with various privacy concerns, including a lack of transparency as to why Facebook collects and shares certain user information. According to SAM, a unit of RobecoSAM, S&P Dow Jones Indices’ collaborator on the S&P 500 ESG Index, its “Media and Stakeholder (MSA) analysis found that Facebook had experienced many privacy issues over the past 24 months, including allowing more than 150 companies access to more users’ personal data than it had disclosed, misuse of personal information (e.g., Cambridge Analytica) and hacking of almost 50 million accounts. These events have created uncertainty about Facebook’s diligence regarding privacy protection, and the effectiveness of the company risk management processes and how the company enforces them. These issues caused the company to lag behind its peers in terms of ESG performance.”

The good news for Facebook and other members of the S&P 500 is that the composition of the S&P 500 ESG Index is reasonably fluid, rebalancing annually. However, the S&P DJI ESG Scores are relative measures.[3] As Facebook’s peers raise the bar in their ESG performance, Facebook will need to do even more to rejoin the ranks of the S&P 500 ESG Index.

[1] Please see the S&P ESG Index Series Methodology.

[2] Please see the Dow Jones Sustainability Indices.

[3] Please see FAQ: S&P DJI ESG Scores.

The posts on this blog are opinions, not advice. Please read our Disclaimers.