Notwithstanding the recent correction associated with renewed trade tensions between the U.S. and China, a strong start to the year for global equity and commodities markets suggests a strong macroeconomic backdrop and a high risk appetite among investors. However, when drilling down into the performance of individual commodities sectors, it is clear that the situation is much more nuanced.

The global commodities market has been dominated by the strength of the petroleum complex so far this year; the intensity of oil supply disruptions has largely overwhelmed middling oil demand and the seemingly perpetual expansion of U.S. oil production, pushing Brent oil prices back up toward USD 75/barrel, albeit briefly. Oil supply constraints have varied from voluntary OPEC production cuts, to rising tensions among various actors in the Middle East, to U.S. sanctions on Venezuela and Iran. While additional supply disruptions are always a risk in the oil market, it is becoming more difficult to see where new disruptions may occur, and fading economic growth prospects in emerging markets as well as the trade conflict between the U.S and China could put increasing pressure on oil consumption growth and energy prices.

Meanwhile, the recent retracement in industrial metals prices reflects the rekindling of the trade war between the U.S. and China. Metals such as aluminium, nickel, and copper are used extensively in the production of goods targeted by U.S. tariffs, such as electronics. More broadly, higher tariffs also add to the existing headwinds facing the Chinese economy, although it is important to remember that Chinese authorities have the capacity to initiate significant economic stimulus should they deem the impact of the trade war too onerous for specific industries or too detrimental to the prospects for broad economic growth.

While investor and central bank interest in gold remains well above that of previous years, the performance of the gold market has been meek, which is rather at odds with the more cautious view of the world economy presented by recent weakness in the oil and metals markets. That said, there are growing signals coming from various central banks that monetary policy may become more accommodative in the second half of the year in response to flattering prospects for global economic growth, which is likely to support gold prices.

The agriculture sector has been a drain on the performance of the overall commodities market during the first five months of 2019. Agriculture markets are not generally dependent on the macroeconomic environment, but a number of agricultural commodities, such as soybeans, have also been drawn into the U.S.-China trade fracas. The spread of African swine fever, which will cut demand for pig feed, and bumper harvests in North and South America have also contributed to soybean prices falling to a post-financial crisis low.

The latter part of the global economic cycle is typically characterized by the outperformance of industrial commodities, namely energy and industrial metals. While commodities are not anticipatory assets, they can provide a useful insight into current macroeconomic conditions on top of any commodities-specific supply and demand dynamic. It is imperative that investors take stock of the myriad of indicators presented by commodities markets, especially given growing economic and geopolitical turbulence.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

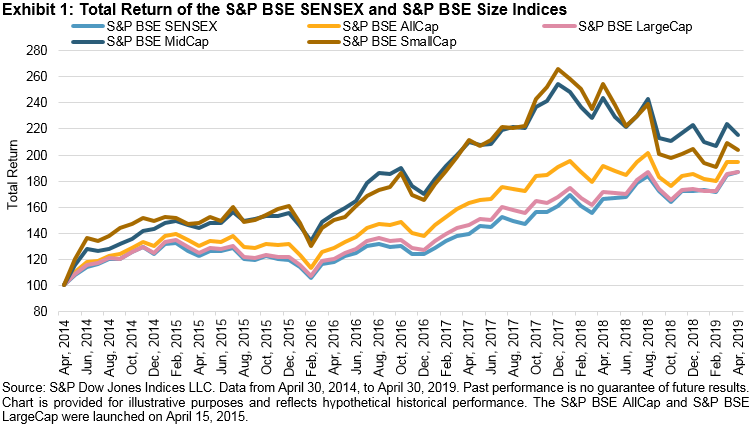

Exhibit 2 provides the five-year absolute returns of the S&P BSE AllCap Series. Among the sub-sector indices in the S&P BSE AllCap, the

Exhibit 2 provides the five-year absolute returns of the S&P BSE AllCap Series. Among the sub-sector indices in the S&P BSE AllCap, the

Source: “

Source: “