The landmark Paris Agreement to accelerate the transition to a low-carbon economy marked a sea change in the global fight against climate change. A swelling tide of carbon-limiting regulations has since emerged, shifting the narrative from a largely ethical debate to a material set of risks and opportunities for the financial markets, today. As the debate continues regarding the link with human activity, the policy response to limit greenhouse gas (GHG) emissions is an undeniable channel through which the underlying transition risk—that is, the risk that comes from a shift in the global modes of production from carbon-intensive to energy-efficient activities—will materialize. These shifts are potentially material for asset values and capital allocation decisions from an investor’s perspective, while many companies will have to adapt to remain profitable.

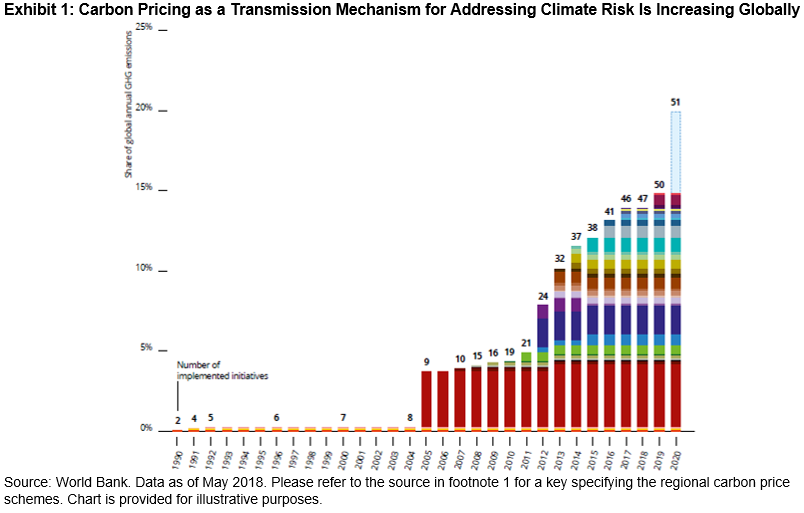

Companies are used to dealing with fluctuations in the price of materials in their production process—and investors watch these closely. When it comes to investment fundamentals, carbon-limiting regulations, such as taxes and emissions trading schemes, are no different. Exhibit 1 shows that 51 countries, regions, and cities will have adopted carbon-pricing schemes by 2020, capturing 20% of global GHG emissions.[1] Thanks to the Paris Agreement, the number of these measures is on the rise, and the pace of change in 2018 alone has been astonishing. In the EU, the carbon price increased from 8 to 18 euros per ton between January and August 2018 and this could increase to 25 euros per ton by the end of 2018.[2] To put this into context, carbon prices would need to increase to USD 120 per ton by 2030 to meet the goals of the Paris Agreement.[3] By design, these measures are transforming the underlying economics to favor more carbon-efficient technologies across all sectors. But just as with commodity price fluctuations, an investor might ask—are companies in certain sectors and regions more prone to (carbon) price risk than others?

Measuring Carbon Earnings at Risk

Carbon pricing will most likely not have uniform effects across portfolios, with both winners and losers emerging. First, carbon pricing across different regions and sectors varies substantially. Second, even companies within the same sector can have varying levels of carbon intensity—they engage in different operations, make use of different technologies, and have different practices that influence their carbon efficiency. Third, varying supply chain elasticities influence the cost pass-through from carbon pricing. As a result, companies and portfolios with different regional and sector exposures can have significant differences in carbon price risk exposure. Thus, any meaningful approach to monetize carbon price risk may need to account for granularity in the range of sectors, geographies, and decarbonization pathway scenarios.

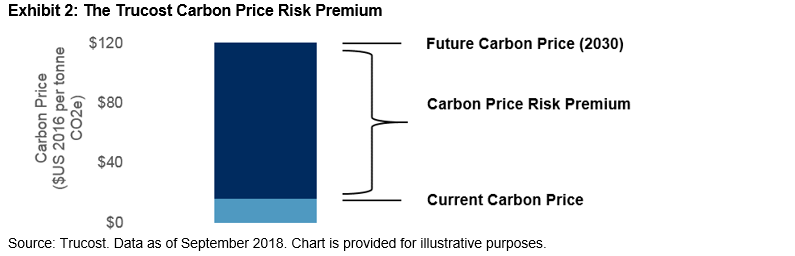

Trucost’s approach is based on a carbon price risk premium, defined as the gap between current and expected future carbon prices in a given time period. This premium depends on three parameters: (i) the initial carbon price, determined by sector and geography; (ii) the expected decarbonization pathway (multiple scenarios are available to choose from); and (iii) the cost pass-through to companies from suppliers. The result is a highly granular dataset of company carbon price premiums based on close to 10,000 sector, year, and country combinations, reflecting the additional financial cost per ton of emissions from expected future carbon pricing regulations. We can use these premia to calculate a company’s exposure to future carbon costs and compare these to earnings metrics to determine the potential earnings at risk. Aggregated at the portfolio level and apportioned on an ownership basis or weighted based on investment exposure, we can produce financial metrics such as change in EBIT(DA) due to carbon price risk and potential impact on valuation multiples.

Investors can integrate these metrics into their decision-making process by incorporating them into a range of valuation approaches and scenario analyses. By influencing risk premiums to evaluate fixed income instruments or loans or plugging these metrics into forward-looking cash flow projections, for example, these metrics can support advanced investment research that accounts for forward-looking climate risk.

From Footprints to Forward-Looking Metrics

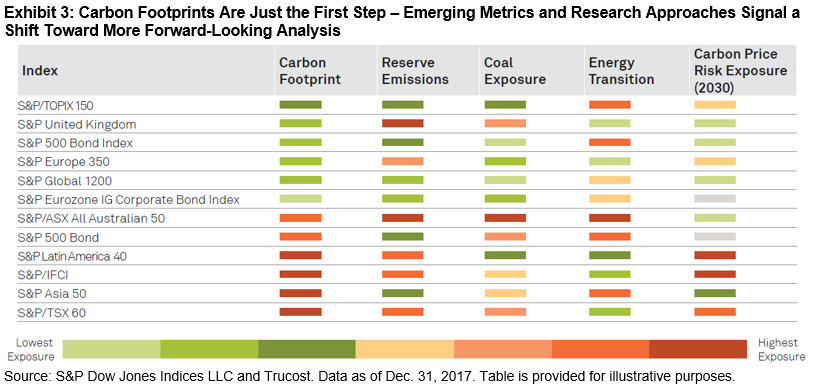

To date, much of the focus in mainstream ESG investing has been to manage the portfolio’s carbon footprint. While carbon footprinting often provides an essential first step toward understanding the climate risk exposure within a portfolio, it may not inform the forward-looking financial risk profile of investments from measures like a carbon price.

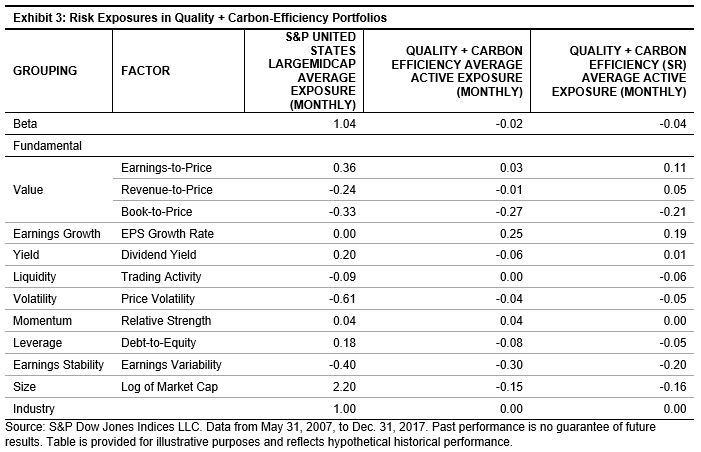

Exhibit 3 applies a range of Trucost carbon exposure metrics to S&P DJI global benchmarks, including carbon earnings-at-risk, and highlights how focusing solely on the carbon footprint might miss the bigger picture in terms of forward-looking risks and opportunities. Thus, to understand the impact of climate change on their investments, investors must recognize there is no silver bullet. Just as it would be prudent to consider a range of financial metrics to determine the overall financial health of a company, so too would it be wise to examine a range of climate-related risks to determine the environmental health of an investment. Moreover, investors do not necessarily have to choose between environmental and financial metrics, as next generation approaches like this may enable us to translate environmental risks into financial metrics. Thus, we can arm investors with the tools they need to assess the profitability of their investments in an ever-shifting global landscape, as we embark on our unprecedented journey toward a low-carbon economy.

[1] Source: World Bank and State and Trends of Carbon Pricing 2018.

[2] See https://markets.businessinsider.com/commodities/co2-emissionsrechte

[3] (OECD, IEA, 2017; CDP, CPLC, 2017).

The posts on this blog are opinions, not advice. Please read our Disclaimers.