In our previous blog, The Growth of Emerging ASEAN, we discussed why market participants are showing increased interest in this region. In this post, let’s take a deeper look at how the emerging ASEAN equity markets—consisting of Indonesia, Malaysia, Philippines, Thailand, and Vietnam—performed historically.

The emerging ASEAN equity markets collectively outperformed the Brazil, Russia, India, China, and South Africa (BRICS) equity markets as a whole on an absolute and risk-adjusted basis over the period from March 31, 2010, to Dec. 31, 2017 (see Exhibit 1).

The emerging ASEAN equity markets are much smaller than the BRICS markets. As of year-end 2017, their aggregate float market cap was approximately one-sixth of the size of the BRICS equity market. In general, smaller markets tend to have lower liquidity and efficiency. The largest companies in small markets tend be the most liquid. The top 100 largest and most liquid companies slightly underperformed the broad emerging ASEAN equity market over the period from March 31, 2010, to Dec. 31, 2017 (see Exhibit 2).

The portfolio of the top 100 largest companies weighted by float market cap was concentrated in stocks domiciled in Indonesia, Malaysia, and Thailand. A country-weight-capped portfolio may reduce the country-specific risk. The capped portfolio of the top 100 largest companies with a country weight capping of 25% and a stock weight capping of 8% outperformed the broad emerging ASEAN equity market over the same period (see Exhibit 3).

S&P Dow Jones Indices recently launched the Dow Jones Emerging ASEAN Titans 100 Index. It consists of companies from the emerging ASEAN equity markets based on composite rank by float market cap, revenue, and net income. The index constituents are weighted by float-adjusted market cap and subject to a country weight cap of 25% and a stock weight cap of 8% to reduce the country and stock concentration risk. It outperformed the top 100 capped portfolio purely selected by market cap over the period from March 31, 2010, to Dec. 31, 2017 (see Exhibit 4).

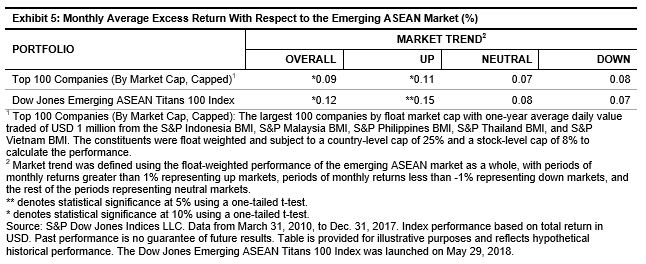

Historically, market participants in the emerging ASEAN equity markets tended to favor the companies with high revenue and income over other companies. The Dow Jones Emerging ASEAN Titans 100 Index outperformed the top 100 capped portfolio from the broad emerging ASEAN equity market trends in all the market cycles. The most significant outperformance was during the up market (see Exhibit 5).

Historically, the emerging ASEAN equity market outperformed the BRICS equity market. Revenue, income, or other fundamentals, along with weight limits to prevent excessive concentration in a particular country or stock, are also important when evaluating the markets for diversification purposes, in addition to market cap and liquidity.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

Source: S&P Dow Jones Indices

Source: S&P Dow Jones Indices