Most S&P and Dow Jones Islamic indices have outperformed conventional benchmarks through the first half of 2018 driven by underweight to financials.

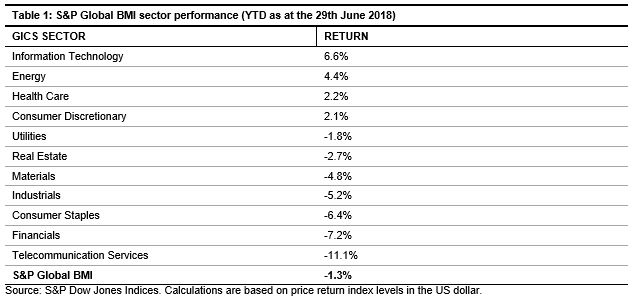

Most S&P and Dow Jones Shariah compliant benchmarks outperformed their conventional counterparts through the first half of 2018 as financials – which are largely absent from Islamic indices – lagged the market by a wide margin. The strong performance of information

technology and healthcare stocks – which tend to be overrepresented in Islamic indices – also contributed to the outperformance of Islamic benchmarks.

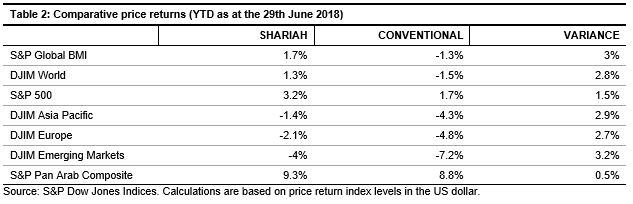

The Dow Jones Islamic Market (DJIM) World and S&P Global BMI Shariah indices rose 1.3% and 1.7% respectively year-to-date (YTD) through the 29th June, outperforming the conventional S&P Global BMI index by about 300bps. A similar trend was seen in all major regions as Shariah compliant benchmarks measuring the US, Europe, Asia Pacific, MENA and emerging markets each outperformed conventional equity benchmarks by meaningful margins.

Emerging markets post steepest losses while the US holds on to gains

In a volatile quarter, emerging market equities experienced steep declines as the US dollar strength, rising interest rates and trade tensions weighed on investor sentiment. The DJIM Emerging Markets Index lost 4% through the middle of the year – representing the weakest performance among major regions. US equities fared relatively well as strong economic data and corporate profits outweighed concerns over protectionist trade policies. The S&P 500 Shariah gained 3.2% through the 29th June representing the lone major global region in positive territory. Meanwhile, DJIM Europe and DJIM Asia-Pacific declined 2.1% and 1.4% respectively through the middle of the year.

Strength in Saudi Arabia boosts MENA’s equity market performance

MENA equities continued to outperform global markets as the S&P Pan Arab Composite Shariah gained 2.3% in the second quarter (Q2) and 9.3% YTD, driven by rising oil prices and unique strength in Saudi Arabia where equity market reforms and expectations of foreign investor inflows have buoyed markets. The S&P Saudi Arabia rose 6.8% in Q2 pushing the index’s YTD gain to nearly 18%.

This article was first published in Islamic Finance news Volume 15 Issue 28 dated the 11th July 2018.

The posts on this blog are opinions, not advice. Please read our Disclaimers.