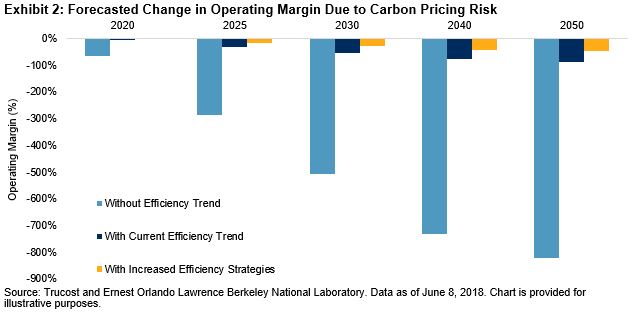

Companies that act now to invest in low carbon technologies have the chance to maintain their license to grow and avoid carbon pricing costs that would significantly reduce profits. For example, in 2020, the technology sector’s investments in energy efficiency for their U.S. data centers could avoid over USD 6.9 billion in carbon costs and show a 59% reduction in operating margins.

Growing global carbon prices can affect companies through regulatory costs imposed on energy and fuel price increases, or through suppliers passing on these costs to the company. Trucost developed its Corporate Carbon Pricing Tool to help companies understand how this carbon pricing risk exposure can affect their competitiveness in a climate-challenged future.

Carbon pricing risk can affect all business sectors. One sector in particular has been successful in reducing its carbon pricing risk in the future. In just the past five years, data centers have turned what was an exponential increase in energy demand into practically a flat line.

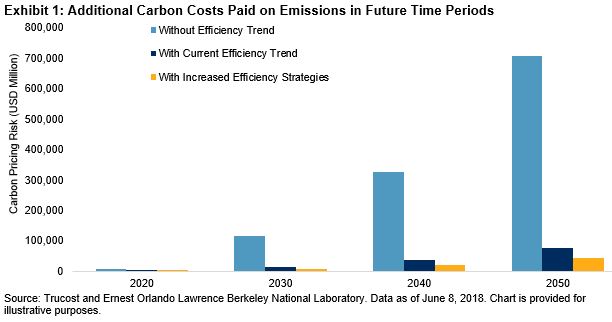

For U.S. data centers alone, there was a 90% increase in electricity use from 2000-2005, as the data center industry saw booming growth.[1] From 2005-2010, this energy use increased only by about 24%. Since 2010, electricity consumption has only increased by about 4%. An overall efficiency trend has helped keep data center energy use steady, despite the technology sector’s continued expansion.

This efficiency trend has helped to drastically reduced the energy usage of data centers, which otherwise would have needed an additional 600 billion kWh by 2020 to meet demand.1 Although many efficiency gains have been made, there remains opportunity to be aggressive in pursuing additional strategies that could decrease electricity consumption by another 33 billion kWh by 2020.

Trucost ran an analysis of three scenarios as depicted in a report1 on U.S. data center usage to help illustrate how data centers have reduced their carbon pricing risk as well as energy intensity. The first scenario depicts the carbon pricing risk for U.S. data centers without any efficiency trend, the second with the current efficiency trend, and the third with adoption of additional efficiency strategies.

The analysis shows how data centers have reduced their carbon pricing risk. A number of factors have helped support this efficiency trend.

- Leading companies have set an example and pushed the industry to innovate quickly in order to save energy costs as well as drive performance. Large internet companies like Google, Facebook, and Amazon have made sizable investments in energy efficiency and renewable energy installations.[2]

- With as much as 48% of operational costs[3] originally dedicated to data center energy needs, there exists a strong business case to invest in energy efficiency.

- Data centers continue to experience strong growth,[4] resulting in new builds that are outfitted with updated servers, infrastructure, and networks with increasing energy efficiency.

- Technological developments, such as server virtualization,[5] movement to cloud services, and more efficient servers has contributed to an overall increase in efficiency.

- There is an industry movement toward a “hyperscale shift” to large data centers configured for maximum productivity that often need fewer servers to provide the same service as smaller data centers.

As more investors request that companies take responsibility for future climate risks,[6] the case of data centers gives us an example of how it is possible to successfully reduce climate risk exposure while still pursuing continuous market growth.

[1] https://eta.lbl.gov/sites/all/files/publications/lbnl-1005775_v2.pdf

[2] http://fortune.com/2016/06/27/data-center-energy-report/

[3] https://www.energystar.gov/ia/partners/prod_development/downloads/EPA_Report_Exec_Summary_Final.pdf

[4] https://cloudscene.com/news/2017/12/2018-data-center-predictions/

[5] https://www.techopedia.com/definition/688/server-virtualization

The posts on this blog are opinions, not advice. Please read our Disclaimers.