When we talk about investments in the U. S., the first thing that comes to mind is the S&P 500®, since it is used to analyze and track large-cap stocks in the U.S. market. Following this iconic index, in July 2015 S&P DJI introduced the S&P 500 Bond Index, which is designed to be a corporate-bond counterpart to the S&P 500. Market value-weighted, the index seeks to measure the performance of U.S. corporate debt issued by constituents of the S&P 500. One of the uses of the S&P 500 Bond Index is to compare the equity and bond markets—some of these comparisons may include performance and sectors. Taking into account sectors, ratings, and maturities, the index has more than 150 subindices, and is calculated in several currencies. Can the index also be used to compare with indices outside of the U.S.? Let’s compare the performance and returns between the S&P 500 Bond Index and the S&P 500 Bond Index (MXN [returns expressed in Mexican pesos]), with four different Mexican indices, two sovereign bond indices and two corporate bond indices.

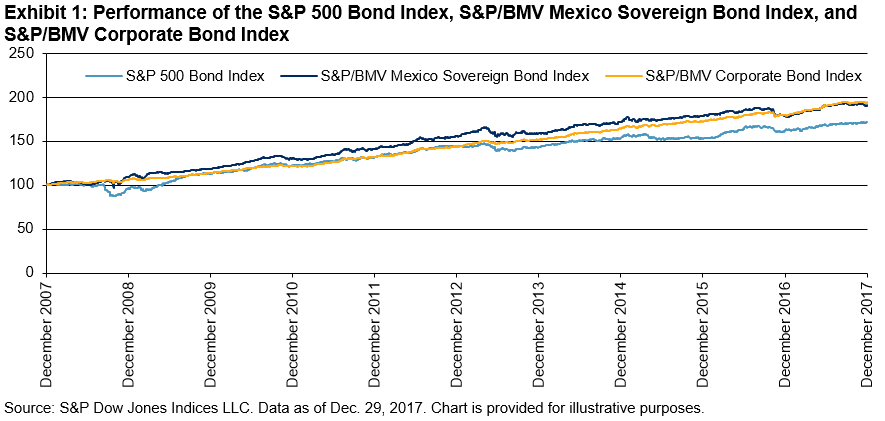

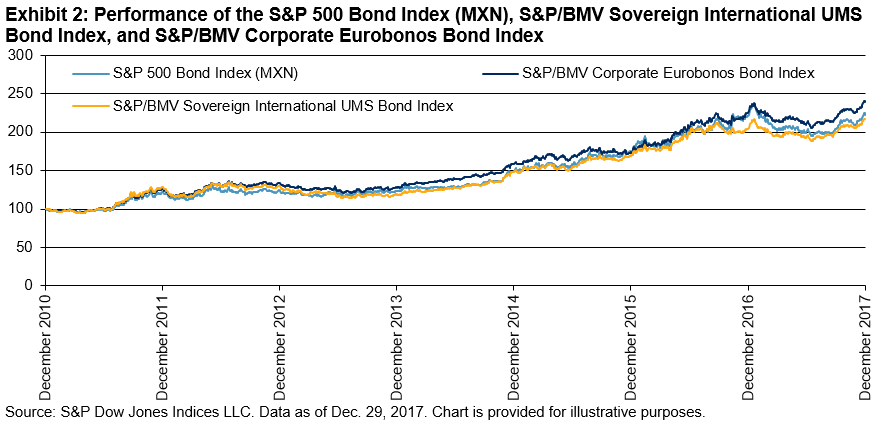

Exhibit 1 shows the performance over the past 10 years of the S&P 500 Bond Index, S&P/BMV Mexico Sovereign Bond Index (which tracks nominal fixed-rate bonds and bills), and the S&P/BMV Corporate Bond Index (which is designed to measure the performance of Mexican corporate-issued bonds). Then, in Exhibit 2, we can see the performance differences between the S&P 500 Bond Index (MXN), S&P/BMV Sovereign International UMS Bond Index, and the S&P/BMV Corporate Eurobonos Bond Index, both of which include the returns of the currency, since they track the eurobond market (bonds issued outside of Mexico in U.S. dollars), expressed in Mexican pesos.

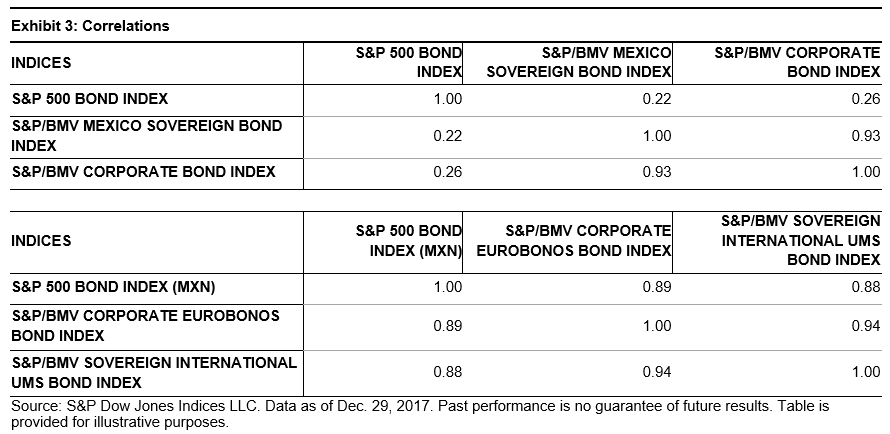

With a yield-to-maturity average spread of more than 335 bps for the past three years, it is interesting how the first group behaved similarly (without taking into account the credit crisis in 2007-2008). The second group’s behavior was expected due to the currency; the correlations are shown in Exhibit 3.

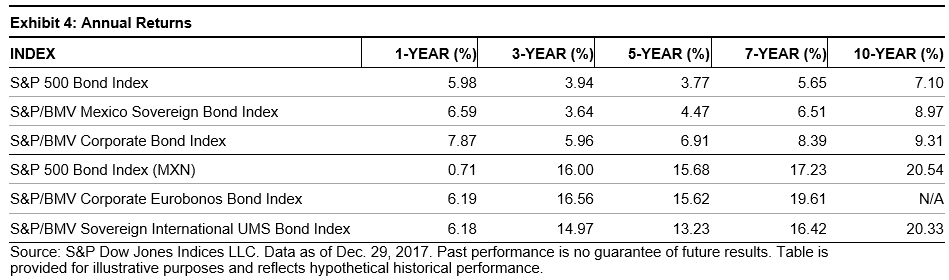

Exhibit 4 shows the annual returns in different time frames, where we can see in more detail how similarly the corporate bond markets have behaved for issuers from the U.S. and Mexico—as measured by the S&P 500 Bond Index (MXN) and S&P/BMV Corporate Eurobonos Bond Index, respectively—with three-year returns of 16.00% and 16.56%, respectively, and five-year returns of 15.68% and 15.62%, respectively.

In times of volatility and when searching for yield, Mexico may provide a good portfolio diversification with the extra yield for those seeking it given the correlation between Mexico and U.S. corporate bonds, as well as with their 2017 performance.

The posts on this blog are opinions, not advice. Please read our Disclaimers.