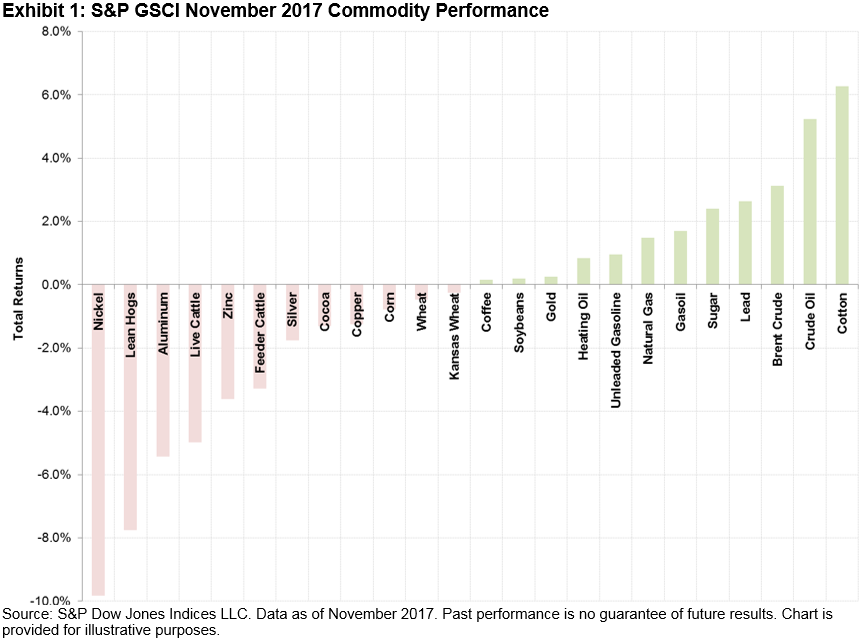

The S&P GSCI was up 1.4% with a YTD return of 1.3% in November. Of the five sectors in the index, energy and agriculture were positive for the month, up 3.4% and 0.5%, precious metals was flat, while industrial metals and livestock finished the month on a negative note, down 3.2% and 5.5%, respectively.

The 24 commodities tracked by the index were divided between positive and negative territory in November. Cotton was the best-performing commodity for the month, while nickel was the worst.

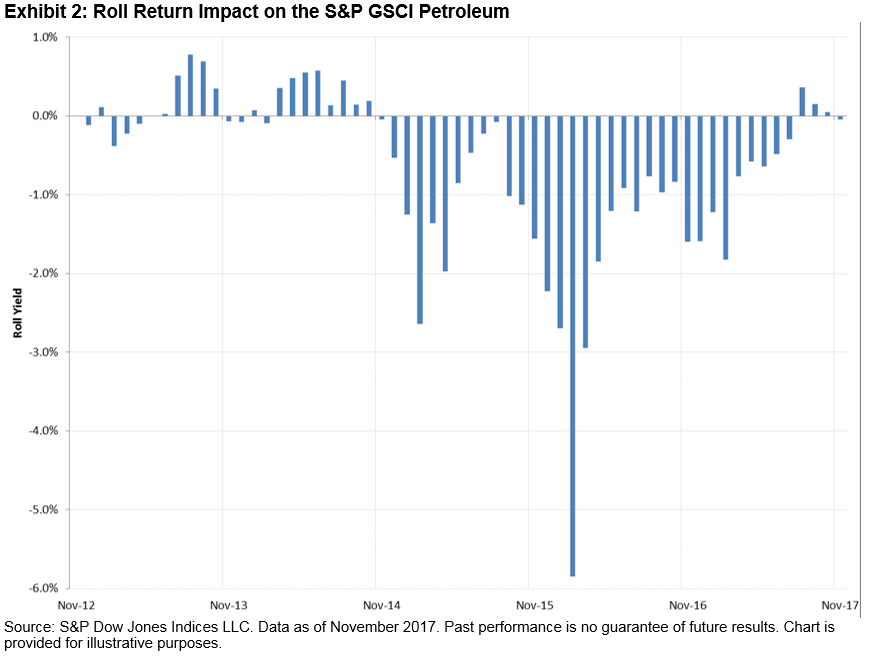

Crude prices benefited from OPEC and non-OPEC members agreeing to extend output cuts into 2018, and WTI specifically benefited from a decrease in inventories by 3.4 million barrels, as reported by the U.S. Energy Information Administration.

In fact, this low level of inventories can be seen in the roll yield of the S&P GSCI Petroleum. Since August, the roll returns, as measured by the excess return of the index minus the spot return, has moved into backwardation (positive roll yield) for petroleum (see Exhibit 2). In November, the roll yield reflected a small level of contango, or negative roll yield, which is the result of nearer contracts being cheaper than later-dated ones, however this contango level of 0.05% still shows a significant improvement from levels seen earlier in the year. The S&P GSCI has been in contango at the end of each month since November 2014.