South African equity markets have once again performed poorly, especially in comparison with global equity markets. One reason for this drab performance was that its GDP contracted 1.2% in the first quarter, although the price of gold—one of the country’s key exports—increased and the South African rand recovered somewhat with respect to other currencies.

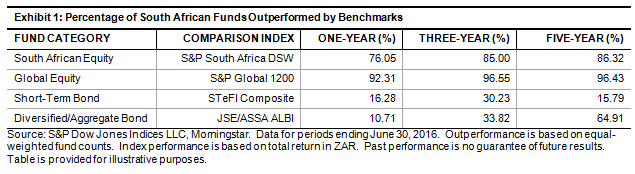

Poor economic news, both domestic and international, led to bouts of heightened volatility in the first half of the year, but active equity managers did not seem to be able to take advantage of this. Across all time horizons studied, both domestic and international active equity funds underperformed their respective benchmarks (see Exhibit 1).

The results regarding fixed income were less clear. Over the five-year horizon, active managers beat their respective benchmark in the short-term bond category but not in the diversified/aggregate bond category.

To access the full report, please click here.